Estratégia Quantitativa da Linha de Distração Enrolada Diariamente

Visão Geral

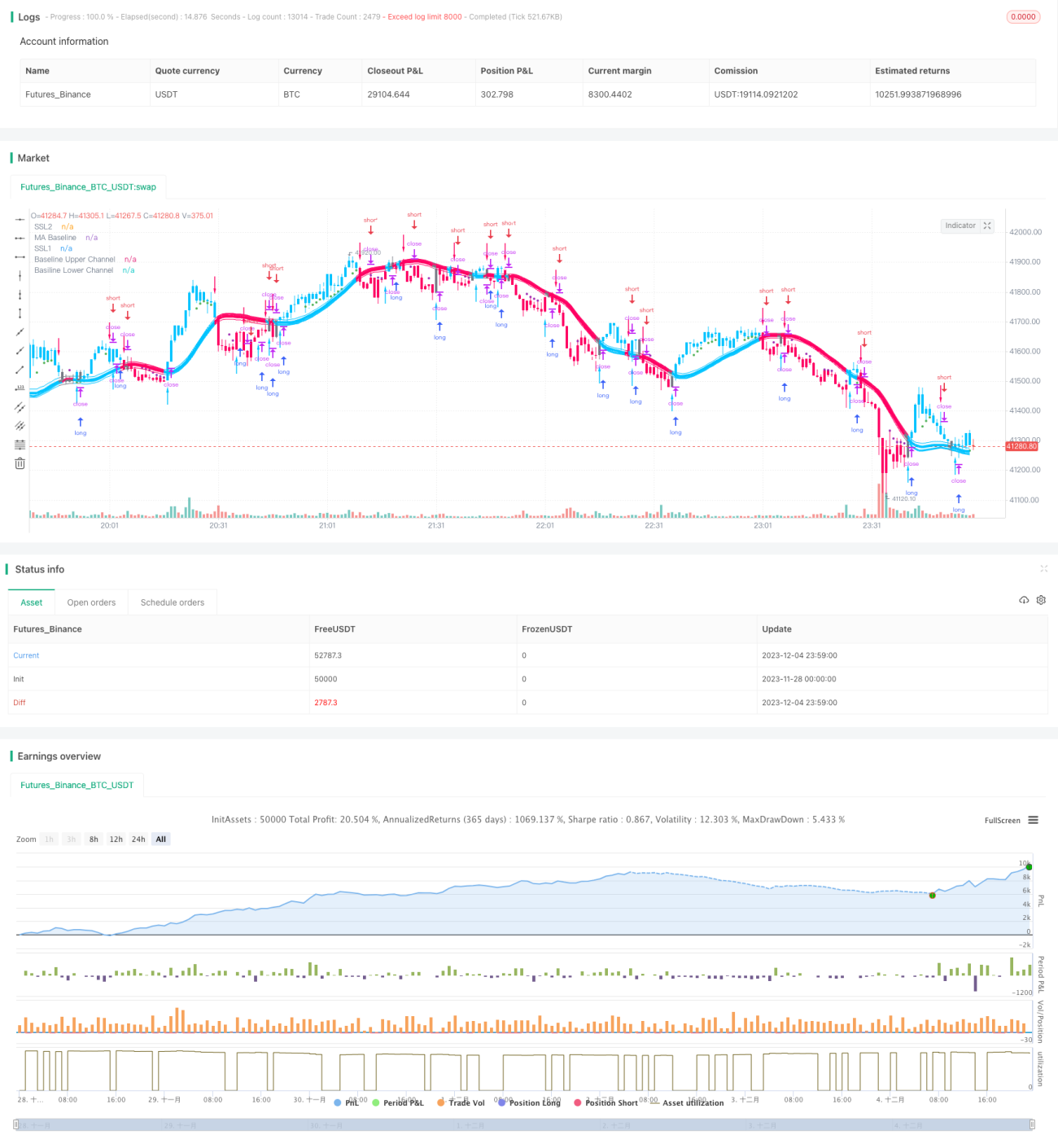

A estratégia quantitativa de curto prazo baseada no indicador Enrolamento e Distração Diários é uma estratégia de negociação quantitativa de curto prazo que utiliza médias móveis e indicadores de preço máximo e mínimo. Ela usa as setas EXIT do indicador híbrido SSL para determinar pontos de compra e venda, combinadas com o filtro do indicador QQE, e emprega o indicador ATR para calcular stops e níveis de adição em lotes. Esta estratégia é adequada para investidores sensíveis à volatilidade do mercado e com controle de risco rigoroso.

Princípio da Estratégia

A estratégia utiliza as setas EXIT do indicador híbrido SSL para determinar pontos de entrada de compra e venda. A seta EXIT possui um ponto alto (EXIT Alto) acima e um ponto baixo (EXIT Baixo) abaixo. Quando o preço de fechamento cruza para baixo a partir do EXIT Alto, gera-se um sinal de venda; quando o preço de fechamento cruza para cima a partir do EXIT Baixo, gera-se um sinal de compra.

Para aumentar a confiabilidade dos sinais, a estratégia introduz o indicador QQE como condição auxiliar de filtro. Os sinais gerados pela seta EXIT só são executados quando o indicador QQE está na mesma direção.

Para controlar o risco, a estratégia utiliza o indicador ATR com multiplicador para calcular os níveis de stop e adição em lotes. O stop de venda é dado por preço de fechamento + ATR × 1,8, e o stop de compra por preço de fechamento – ATR × 1,8. A adição é feita em três lotes, cada um com 10% do valor inicial, nos níveis: preço de fechamento – ATR × 0,1, preço de fechamento – ATR × 0,3 e preço de fechamento – ATR × 0,7.

Cada lote de adição possui seu próprio stop. O primeiro lote (20% do valor inicial) é interrompido ao atingir o stop, enquanto os demais lotes continuam mantidos.

Vantagens da Estratégia

- Lucro com as setas EXIT e stop rápido, controlando efetivamente o risco.

- Filtro do indicador QQE, aumentando a precisão dos sinais.

- Utilização do ATR para calcular stops e níveis de adição com base na volatilidade do mercado, resultando em um controle de risco mais preciso.

- Adição em lotes, aproveitando plenamente as tendências para obter lucro.

Riscos da Estratégia

- Posições lucrativas que atingem o stop parcial podem fazer com que as posições restantes enfrentem o risco de stops adicionais. Pode-se considerar um take profit geral ou baseado nos fundamentos do ativo.

- A sensibilidade diferente das setas EXIT e do indicador QQE à volatilidade do mercado pode gerar sinais contraditórios; é necessário ajustar os parâmetros para reduzir conflitos.

- A adição agressiva pode levar a compras em topos e vendas em fundos. Deve-se avaliar a situação e reduzir a alavancagem.

Direções de Otimização

- Combinar indicadores fundamentais do próprio ativo para take profit, como relação valor contábil, P/L e dividend yield, definindo níveis razoáveis.

- Ajustar os parâmetros do indicador QQE para alinhar os sinais com as setas EXIT.

- Reduzir a proporção de adição de acordo com o calor do mercado, diminuindo a adição em mercados laterais.

- Testar a melhor combinação de parâmetros com base em métricas como drawdown máximo e relação lucro/prejuízo.

Resumo

Esta estratégia utiliza as setas EXIT do indicador híbrido SSL como núcleo do sinal, empregando os indicadores QQE e ATR para filtragem e stop. Através da adição em lotes, amplia os lucros. É uma estratégia quantitativa de curto prazo, adequada para acompanhar tendências de curto prazo do mercado. A estratégia possui capacidade de controle de drawdown e risco, mas também requer atenção a riscos como conflitos de sinais e compras em topos/vendas em fundos. Se combinada com métodos de take profit baseados em fundamentos, e com maior cautela ao julgar oscilações do mercado e ajustar a proporção de adição, o potencial de lucro da estratégia será maior.

- 1