Estratégia Quantitativa Baseada na Taxa de Variação de Preço e Média Móvel

Visão Geral

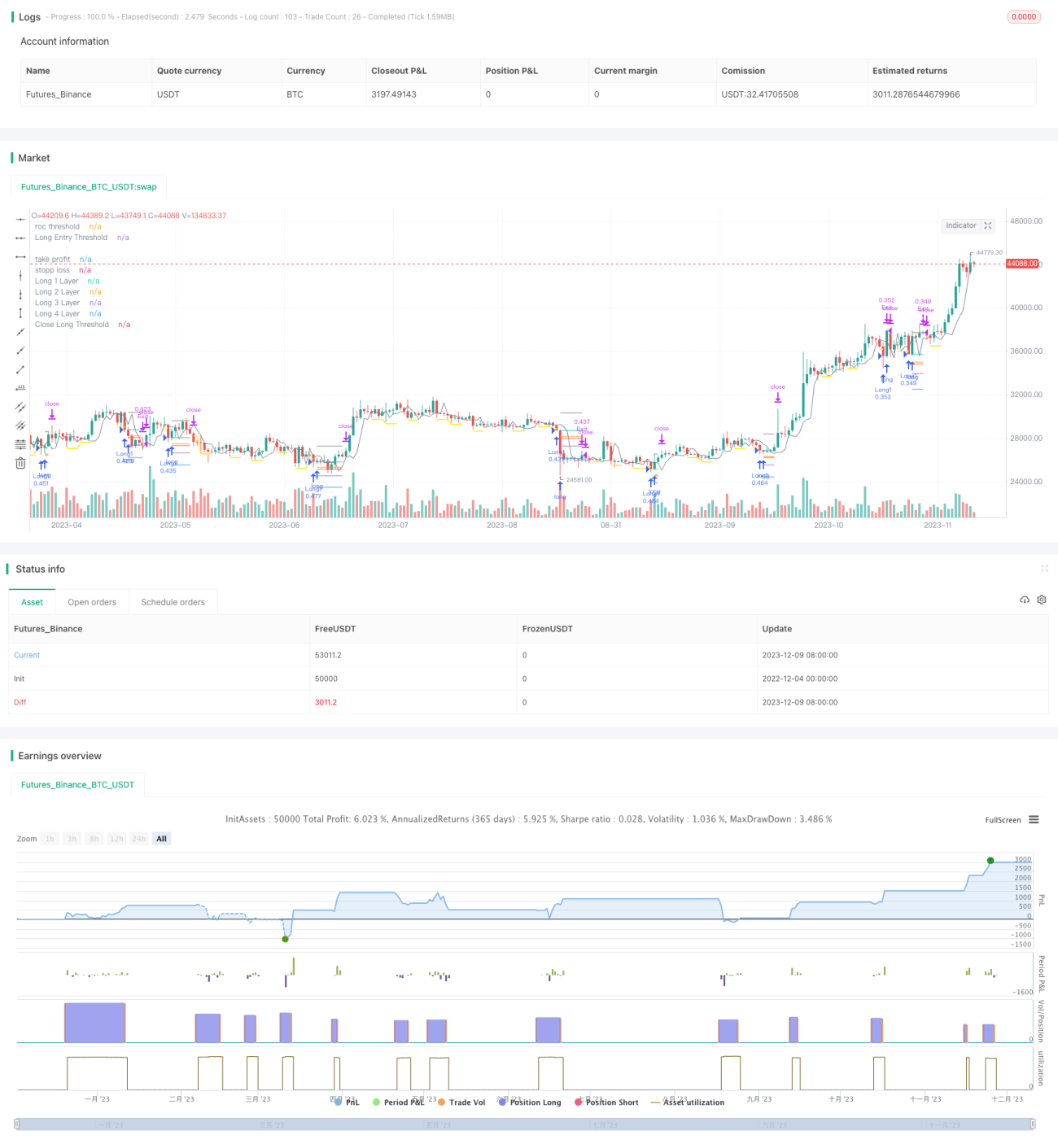

Esta estratégia combina indicadores técnicos de taxa de variação de preço e média móvel para realizar o posicionamento preciso de pontos de compra e venda. Quando o preço apresenta uma queda significativa, estabelece um limite de compra e, quando cai ainda mais, abre uma posição longa. Quando o preço sobe, estabelece um limite de venda e, quando continua subindo, fecha a posição. Ao mesmo tempo, a estratégia também adota o método de adicionar posições, comprando em várias etapas para reduzir o custo.

Princípio da Estratégia

Lógica de Compra

- Calcular a taxa de variação de preço (ROC) e definir a linha de limiar de compra.

- Quando o preço cai abaixo da linha de limiar de compra, registra esse ponto e ativa a linha de restrição de compra.

- A linha de restrição de compra define uma duração com base nos parâmetros de entrada e é fechada após expirar.

- Quando o preço continua caindo e quebra a linha de restrição de compra, abre a primeira posição longa.

Lógica de Venda

- Calcular a taxa de variação de preço (ROC) e definir a linha de limiar de venda.

- Quando o preço sobe acima da linha de limiar de venda, registra esse ponto e ativa a linha de restrição de venda.

- A linha de restrição de venda define uma duração com base nos parâmetros de entrada e é fechada após expirar.

- Quando o preço continua subindo e quebra a linha de restrição de venda, fecha todas as posições longas.

Controle de Risco

A estratégia possui funções integradas de stop loss e take profit, com parâmetros personalizáveis, controlando em tempo real o risco das posições existentes.

Método de Adição de Posições

A cada nova posição aberta, define o preço de compra subsequente em uma certa proporção com base nos parâmetros de entrada, realizando o efeito de compra em lotes para adicionar posições.

Análise de Vantagens

- Utiliza o indicador de taxa de variação de preço (ROC) para encontrar pontos de compra e venda. O ROC é muito sensível às mudanças de preço, posicionando com precisão os pontos de compra e venda.

- Adota o método de linha de restrição para confirmar ainda mais o momento de compra e venda, evitando falsos rompimentos.

- O método de adição de posições permite acompanhar o valor de mercado com base no risco controlável.

- As funções integradas de stop loss e take profit controlam rigorosamente o risco de cada posição individual.

Riscos e Soluções

- Quando o mercado apresenta volatilidade severa, a estratégia pode abrir muitas posições. A solução é definir razoavelmente os parâmetros de adição de posições, controlando o número total de posições.

- Quando a tendência de preço é oscilante e incerta, os preços de stop loss ou take profit podem ser acionados com frequência. Pode-se ajustar apropriadamente as amplitudes de take profit e stop loss, ou desativar essa função.

Sugestões de Otimização

- Combinar com outros indicadores para filtrar o momento de entrada. Por exemplo, usando a média móvel, só considerar o indicador ROC quando o preço cair abaixo da média móvel.

- Otimizar a lógica de adição de posições, iniciando a adição apenas quando certas condições forem atendidas. Por exemplo, continuar adicionando apenas quando o preço cair novamente além de um determinado limite.

- As configurações de parâmetros para diferentes instrumentos podem variar bastante, sendo necessário realizar backtesting e simulação em conta demo suficientes para obter a melhor combinação de parâmetros.

- Pode-se configurar stop loss e take profit adaptativos, definindo diferentes amplitudes de stop de acordo com o nível de volatilidade do mercado.

Resumo

Esta estratégia utiliza de forma abrangente o indicador ROC para posicionar precisamente pontos de compra e venda, o método de linha de restrição para filtrar sinais, stop loss e take profit integrados para prevenir riscos, e a adição de posições para ampliar os lucros. Com parâmetros definidos de forma razoável, pode-se obter retornos excessivos enquanto mantém o risco dentro de níveis controláveis. No futuro, pode-se otimizar ainda mais os mecanismos de filtragem de sinais e controle de risco, tornando a estratégia adaptável a mais condições de mercado.

- 1