Estratégia de rastreamento dinâmico de tendências

Visão Geral

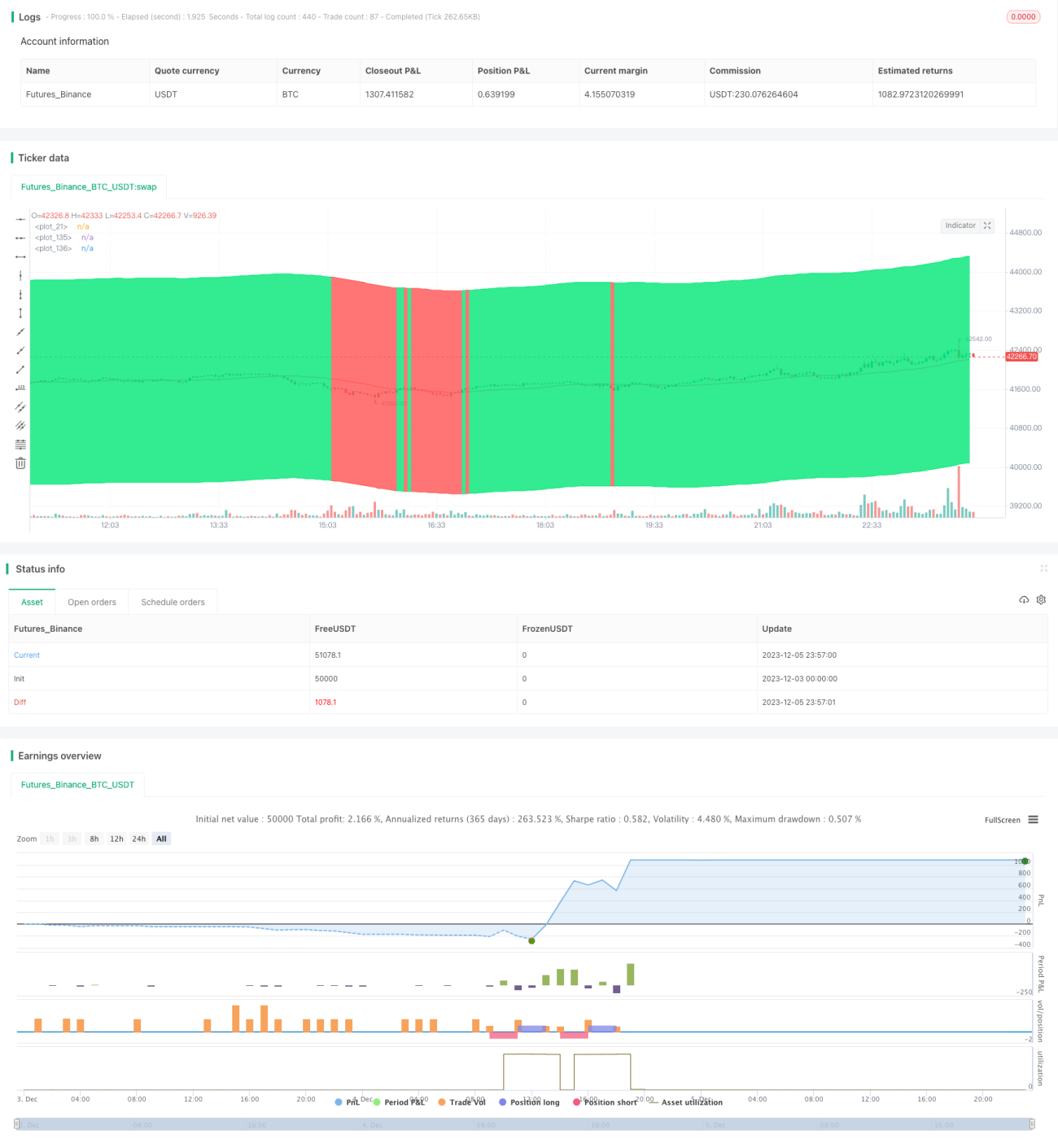

A ideia principal desta estratégia é acompanhar dinamicamente a tendência do mercado, comprando quando a tendência é de alta e vendendo quando a tendência é de baixa. Ela determina a direção da tendência através da combinação de vários indicadores, como regressão linear e uma média móvel Hull modificada.

Princípio da Estratégia

Esta estratégia utiliza vários indicadores técnicos para determinar a direção da tendência. Primeiro, calcula um canal de alcance, cujos limites superior e inferior são baseados na média móvel simples do fechamento e em um parâmetro de entrada. Em seguida, calcula a média móvel Hull modificada, que é considerada mais precisa na descrição da tendência. Além disso, também é calculado o indicador de regressão linear. Quando a média móvel Hull modificada cruza para cima a regressão linear, gera sinais de compra; quando cruza para baixo, gera sinais de venda. Dessa forma, é possível acompanhar dinamicamente as mudanças da tendência.

Para reduzir sinais falsos, a estratégia também projeta vários filtros. Por exemplo, utiliza a EMA para determinar se o mercado está em tendência de queda e um indicador de janela para analisar as variações do RSI. Esses filtros ajudam a evitar a geração de sinais de negociação em mercados laterais.

Quanto à entrada e ao stop loss, a estratégia registra o último preço de abertura e define percentuais de stop gain e stop loss. Por exemplo, se o último preço de uma posição comprada for 100 dólares, o objetivo de lucro é definido em 102 dólares e o stop loss em 95 dólares. Isso permite um acompanhamento dinâmico.

Análise de Vantagens

Esta estratégia apresenta as seguintes vantagens:

- Acompanha dinamicamente as mudanças de tendência, capturando direções de longo prazo com eficiência;

- Utiliza múltiplos filtros para reduzir ruídos e evitar negociações frequentes em mercados laterais;

- Ajusta automaticamente os níveis de stop gain e stop loss, realizando um rastreamento de tendência;

- Permite a otimização de parâmetros para encontrar automaticamente a melhor combinação de parâmetros.

Análise de Riscos

A estratégia também apresenta alguns riscos:

- Ainda não é possível evitar completamente o risco de ficar preso em movimentos adversos. Quando a tendência se inverte, podem surgir perdas flutuantes significativas.

- Uma configuração inadequada de parâmetros pode levar a um desempenho ruim. É necessário otimizar para encontrar a melhor combinação de parâmetros.

- Um tempo de processamento de dados muito longo pode causar atraso nos sinais. É necessário otimizar o cálculo dos indicadores para torná-los o mais em tempo real possível.

Para controlar o risco, pode-se utilizar stop loss, trailing stop ou opções para travar lucros. Além disso, é essencial testar repetidamente as combinações de parâmetros para encontrar faixas confiáveis. Por fim, também é preciso monitorar o tempo de cálculo dos indicadores, buscando a máxima atualidade dos sinais.

Direções de Otimização

A estratégia pode ser otimizada nos seguintes aspectos:

- Testar combinações de mais indicadores para encontrar formas mais confiáveis de determinar a tendência;

- Ajustar a faixa de parâmetros para encontrar os parâmetros ideais;

- Otimizar os filtros de sinal, encontrando um equilíbrio entre a redução de ruído e o atraso;

- Experimentar métodos como aprendizado de máquina para gerar regras de negociação automaticamente.

Durante o processo de otimização, é crucial utilizar backtesting e simulação de negociações para avaliar a qualidade dos sinais e a estabilidade da estratégia. Somente após validação suficiente as soluções otimizadas podem ser aplicadas em negociações reais.

Resumo

No geral, esta estratégia é uma boa estratégia de rastreamento de tendência. Ela utiliza vários indicadores para julgar a tendência, configura filtros para reduzir sinais falsos e pode ajustar automaticamente os stops de lucro e perda para acompanhar a tendência. Se os parâmetros forem configurados adequadamente, ela pode capturar eficientemente tendências de médio e longo prazo. O próximo passo é encontrar os parâmetros ideais e continuar validando e otimizando a estratégia.

- 1