Estratégia de Rompimento de Oscilação de Preço

Visão Geral

A estratégia de rompimento de oscilação utiliza formações de preço em range, realizando operações de compra ou venda quando o preço rompe níveis-chave de suporte ou resistência. A estratégia combina múltiplos indicadores técnicos para identificar oportunidades de negociação relevantes.

Princípio da Estratégia

A estratégia baseia-se principalmente em quatro indicadores técnicos: a linha média das Bandas de Bollinger, a Média Móvel Simples (SMA) de 48 dias, o MACD e o ADX. A lógica específica é:

-

Quando o preço de fechamento cruza acima ou abaixo da SMA de 48 dias, considera-se uma oportunidade de negociação;

-

Quando o preço de fechamento rompe a linha média das Bandas de Bollinger, funciona como sinal de entrada;

-

O MACD deve ser maior ou menor que 0, atuando como indicador auxiliar para determinar a direção da tendência;

-

O ADX deve ser maior que 25, para filtrar mercados sem tendência definida.

Quando as quatro condições acima são atendidas, realiza-se uma operação de compra (long) ou venda (short).

Vantagens da Estratégia

Esta é uma estratégia que combina indicadores de tendência e de oscilação. Suas principais vantagens são:

-

A SMA de 48 dias filtra negociações excessivamente frequentes, focando em tendências de médio a longo prazo;

-

O rompimento da linha média das Bandas de Bollinger captura pontos-chave de suporte e resistência, oferecendo forte função de stop-loss;

-

O MACD determina a direção da tendência principal, evitando negociações contrárias à tendência;

-

O ADX filtra mercados sem tendência, aumentando a taxa de acerto da estratégia.

Em resumo, a estratégia otimiza diversos aspectos como controle da frequência de negociação, identificação de pontos-chave, determinação de tendência e filtragem de movimentos ineficazes, resultando em uma alta taxa de acerto.

Riscos da Estratégia

Os principais riscos da estratégia são:

-

Em mercados laterais, a linha média das Bandas de Bollinger pode gerar sinais de negociação com frequência, levando a excesso de operações;

-

O indicador ADX, ao avaliar tendências e mercados sem direção, também apresenta certa margem de erro;

-

O risco de drawdown é elevado, sendo adequada para investidores com certa tolerância ao risco.

Otimização da Estratégia

A estratégia pode ser aprimorada nos seguintes aspectos:

-

Incluir o indicador ATR para definir stops de perda, reduzindo a perda por operação;

-

Otimizar os parâmetros das Bandas de Bollinger, diminuindo a frequência de rompimento da linha média;

-

Adicionar indicadores de volume ou de força da tendência para avaliar a intensidade do movimento, evitando reversões fracas.

Conclusão

Em resumo, a estratégia de rompimento de oscilação é relativamente consolidada, capturando de forma eficaz os pontos críticos de negociação em mercados oscilantes. Ao combinar indicadores de tendência e oscilação, ela equilibra risco e retorno. Com otimizações adicionais, é possível obter retornos excedentes mais estáveis.

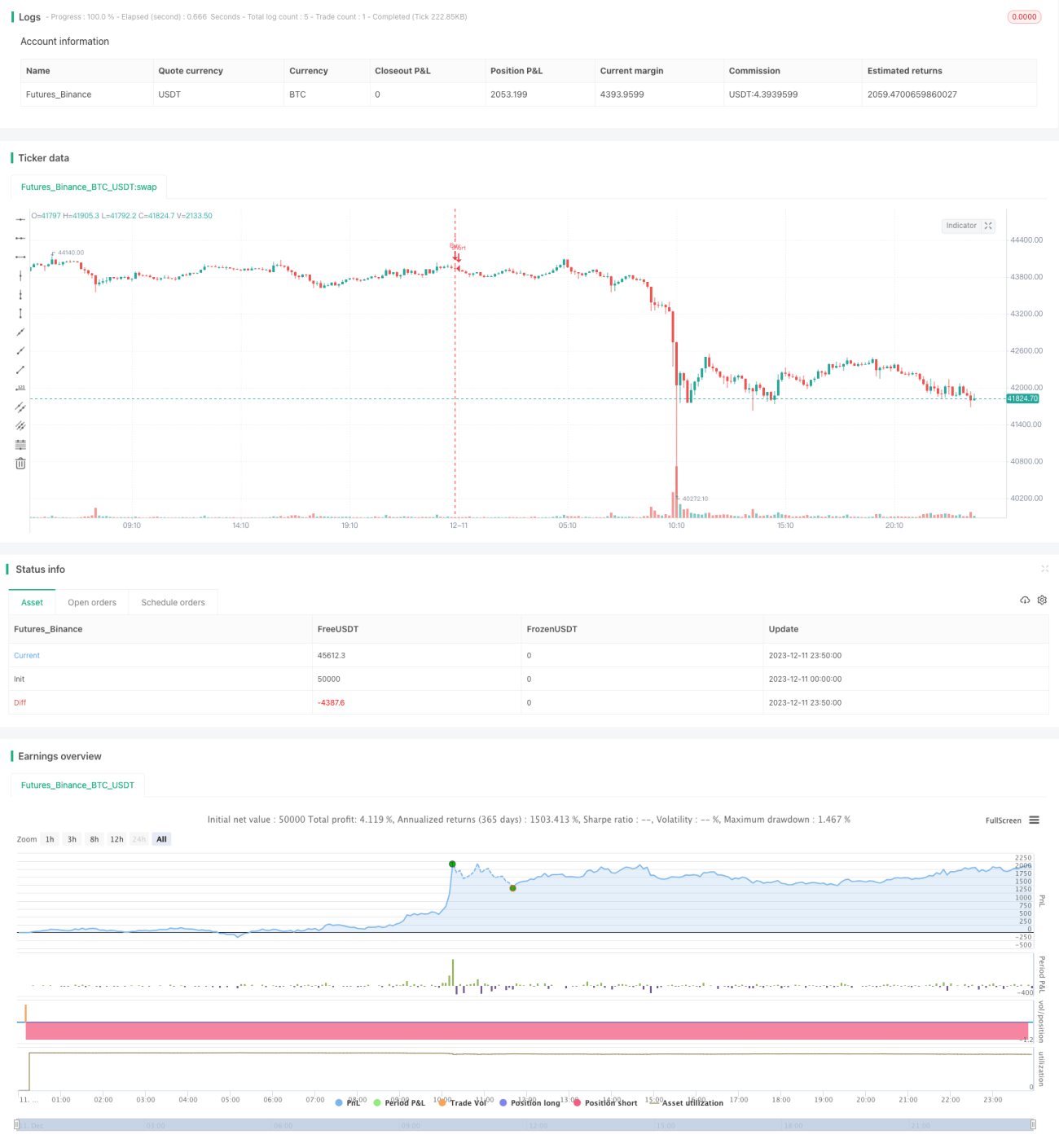

/*backtest

start: 2023-12-11 00:00:00

end: 2023-12-12 00:00:00

period: 10m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © 03.freeman

//Volatility Traders Minds Strategy (VTM Strategy)

//I found this startegy on internet, with a video explaingin how it works.- 1