Estratégia de Seguimento de Tendência com Reversão Dupla

Visão Geral

Esta é uma estratégia de acompanhamento de tendência que combina sinais de reversão dupla. Ela integra a estratégia de reversão 123 e a estratégia de índice de desempenho, rastreando pontos de reversão de preço para obter uma determinação de tendência mais confiável.

Princípio da Estratégia

A estratégia é composta por duas subestratégias:

-

Estratégia de Reversão 123

Utiliza velas de 14 dias para identificar sinais de reversão. As regras específicas são:

- Sinal de alta: o preço de fechamento dos dois dias anteriores está em queda, o preço de fechamento da vela atual é superior ao do dia anterior, e o Estocástico Lento de 9 períodos está abaixo de 50.

- Sinal de baixa: o preço de fechamento dos dois dias anteriores está em alta, o preço de fechamento da vela atual é inferior ao do dia anterior, e o Estocástico Rápido de 9 períodos está acima de 50.

-

Estratégia de Índice de Desempenho

Calcula a variação percentual dos últimos 14 dias como indicador. A regra é:

- Índice de desempenho > (0) gera sinal de alta.

- Índice de desempenho < (0) gera sinal de baixa.

O sinal final é a combinação dos dois sinais. Ou seja, é necessário que ambos os sinais estejam na mesma direção para gerar uma operação real de compra ou venda.

Isso ajuda a filtrar parte do ruído, tornando os sinais mais confiáveis.

Vantagens da Estratégia

Este sistema de reversão dupla possui as seguintes vantagens:

- Combinação de dois fatores para uma determinação de sinal mais confiável.

- Capacidade de filtrar eficazmente o ruído do mercado, evitando sinais falsos.

- O padrão 123 é clássico e prático, fácil de identificar e reproduzir.

- O índice de desempenho permite avaliar a direção futura da tendência.

- Combinação flexível de parâmetros que pode ser otimizada ainda mais.

Riscos da Estratégia

Esta estratégia também apresenta alguns riscos:

- Pode perder reversões súbitas, não capturando totalmente as tendências.

- A combinação de condições duplas reduz o número de sinais, podendo afetar a rentabilidade.

- Requer julgamento na mesma direção, sendo suscetível a flutuações atípicas de ações individuais.

- Problemas na configuração de parâmetros podem causar desvios nos sinais.

Podem ser consideradas as seguintes otimizações:

- Ajuste de parâmetros, como o comprimento das velas, período do Estocástico, etc.

- Otimização da lógica de julgamento dos sinais duplos.

- Combinação com mais fatores, como volume de negociação.

- Adição de mecanismo de stop loss.

Resumo

Esta estratégia integra julgamentos de reversão dupla, sendo eficaz na identificação de pontos de inflexão de preço. Embora a probabilidade de ocorrência de sinais seja reduzida, a confiabilidade é alta, sendo adequada para capturar tendências de médio a longo prazo. O desempenho da estratégia pode ser ainda mais aprimorado através de ajustes de parâmetros e otimização multifatorial.

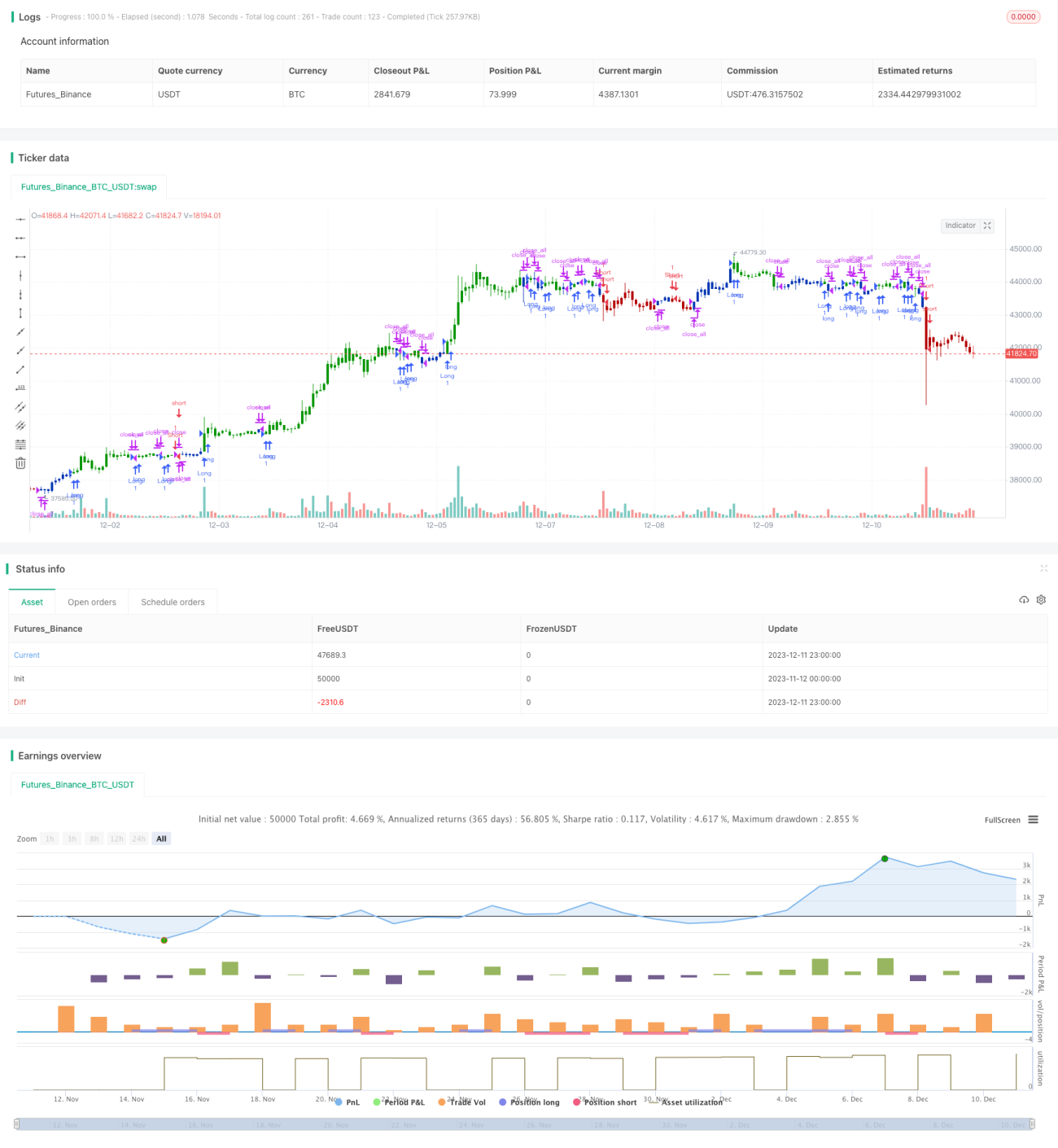

/*backtest

start: 2023-11-12 00:00:00

end: 2023-12-12 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 15/04/2021

// This is combo strategies for get a cumulative signal. - 1