Estratégia de Negociação Quantitativa com MACD Reverso de Duplo Canal

Visão Geral

Esta estratégia é uma estratégia de negociação quantitativa de reversão MACD de trilha dupla. Ela se baseia nos indicadores técnicos descritos por William Blau em seu livro "Momentum, Direction and Divergence" e os expande. A estratégia também possui funcionalidade de backtest, podendo adicionar alertas, filtros, stop loss móvel e outros recursos adicionais.

Princípio da Estratégia

O indicador central da estratégia é o MACD. Ele calcula a média móvel rápida EMA(r) e a média móvel lenta EMA(slowMALen), e então calcula a diferença xmacd. Além disso, calcula a EMA(signalLength) do xmacd para obter xMA_MACD. Quando o xmacd cruza acima do xMA_MACD, é feita uma posição comprada; quando cruza abaixo, uma posição vendida. O ponto chave da estratégia são os sinais de negociação reversa, ou seja, a relação entre xmacd e xMA_MACD é oposta à do indicador MACD convencional, daí o nome "MACD Reverso". Além disso, a estratégia introduz filtros de tendência. Quando um sinal de compra é emitido, se um filtro de tendência de alta estiver configurado, ele verifica se o preço está subindo; similarmente, sinais de venda verificam a tendência de queda de preço. Os indicadores RSI e MFI também podem ser usados para filtrar sinais. A configuração de um mecanismo de stop loss pode evitar perdas que excedam um limite.

Análise de Vantagens

A maior vantagem desta estratégia é sua poderosa funcionalidade de backtest. Ela permite selecionar diferentes ativos de negociação, definir o período de backtest e otimizar a estratégia para dados de ativos específicos. Em comparação com uma estratégia MACD simples, ela adiciona julgamentos de tendência e sobrecompra/sobrevenda, podendo filtrar alguns sinais redundantes. O MACD reverso de trilha dupla difere do MACD tradicional, podendo capturar oportunidades que o MACD tradicional pode perder.

Análise de Riscos

Os riscos desta estratégia decorrem principalmente da abordagem de negociação reversa. Embora os sinais reversos possam capturar algumas oportunidades, também significam abrir mão de alguns pontos de compra e venda tradicionais do MACD, o que requer avaliação cuidadosa. Além disso, o próprio MACD é propenso a gerar sinais falsos de alta. Se houver um mercado lateral (oscilação), a estratégia pode gerar muitas negociações, aumentando os custos de transação e perdas por derrapagem (slippage). Para reduzir riscos, pode-se ajustar adequadamente os parâmetros, otimizar os comprimentos das médias móveis; combinar filtros de tendência e indicadores para evitar sinais em mercados laterais; aumentar adequadamente a distância do stop loss para garantir o controle de perdas em negociações individuais.

Direções de Otimização

A estratégia pode ser otimizada nos seguintes aspectos:

- Ajustar os parâmetros das trilhas rápida e lenta, otimizar os comprimentos das médias móveis, testar com dados de ativos específicos para encontrar a melhor combinação de parâmetros.

- Adicionar ou ajustar filtros de tendência, avaliar com base nos resultados do backtest se a taxa de retorno da estratégia melhora.

- Testar diferentes mecanismos de stop loss: se stop loss fixo ou stop loss móvel é melhor.

- Tentar combinar outros indicadores, como KD, Bandas de Bollinger, etc., definir mais condições de filtro para garantir a qualidade dos sinais.

Conclusão

A estratégia quantitativa de reversão MACD de trilha dupla se inspira no conceito do clássico indicador MACD, expandindo-o e aprimorando-o. A estratégia possui vantagens como configuração flexível de parâmetros, ampla seleção de mecanismos de filtro e uma poderosa funcionalidade de backtest. Isso permite otimizações personalizadas para diferentes ativos de negociação, tornando-a uma estratégia de negociação quantitativa promissora que vale a pena explorar.

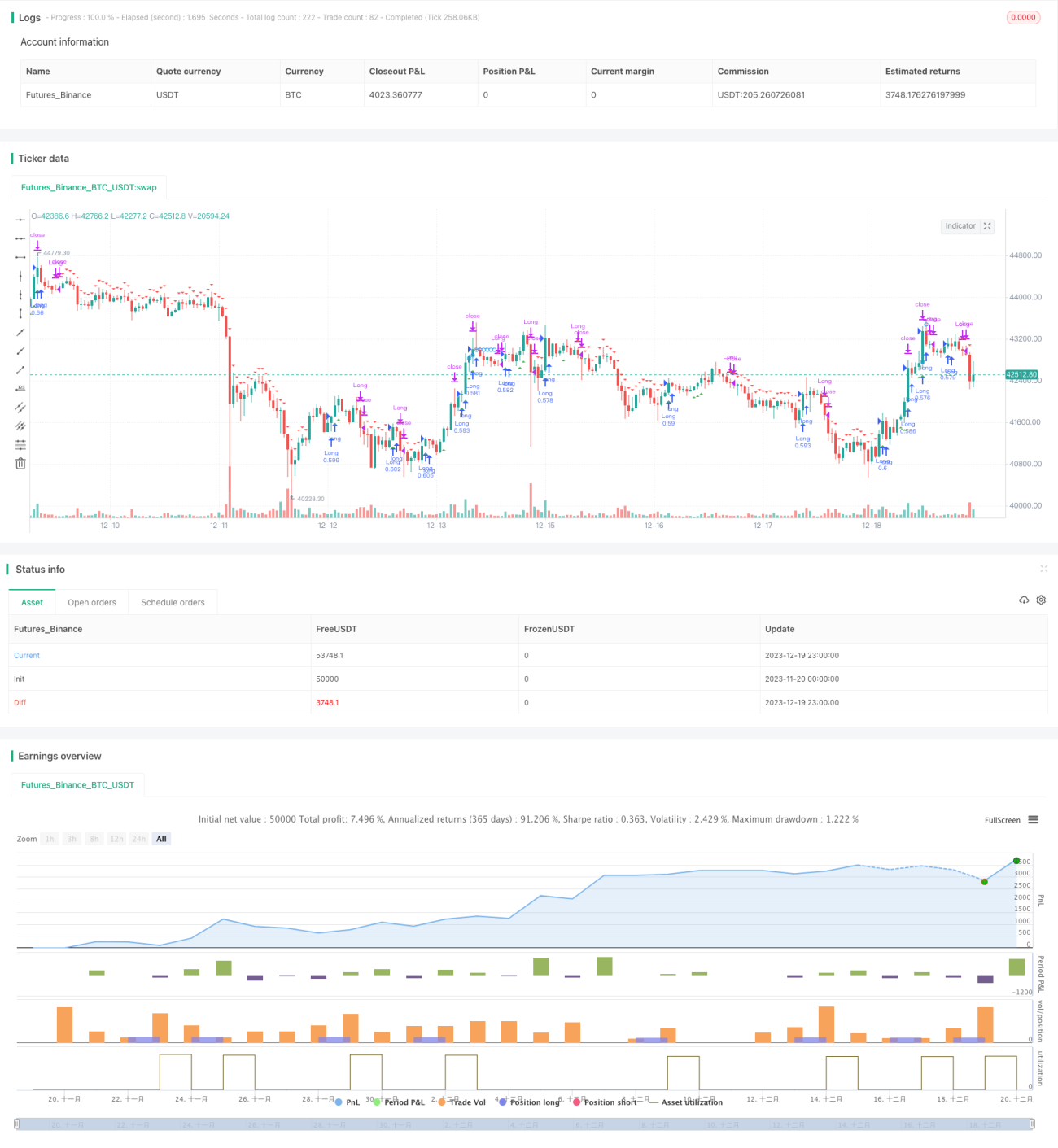

/*backtest

start: 2023-11-20 00:00:00

end: 2023-12-20 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version = 3

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 09/12/2016

// This is one of the techniques described by William Blau in his book- 1