Estratégia de Razão de Médias Móveis em Cadeia com Filtro de Tendência Dupla

Visão Geral

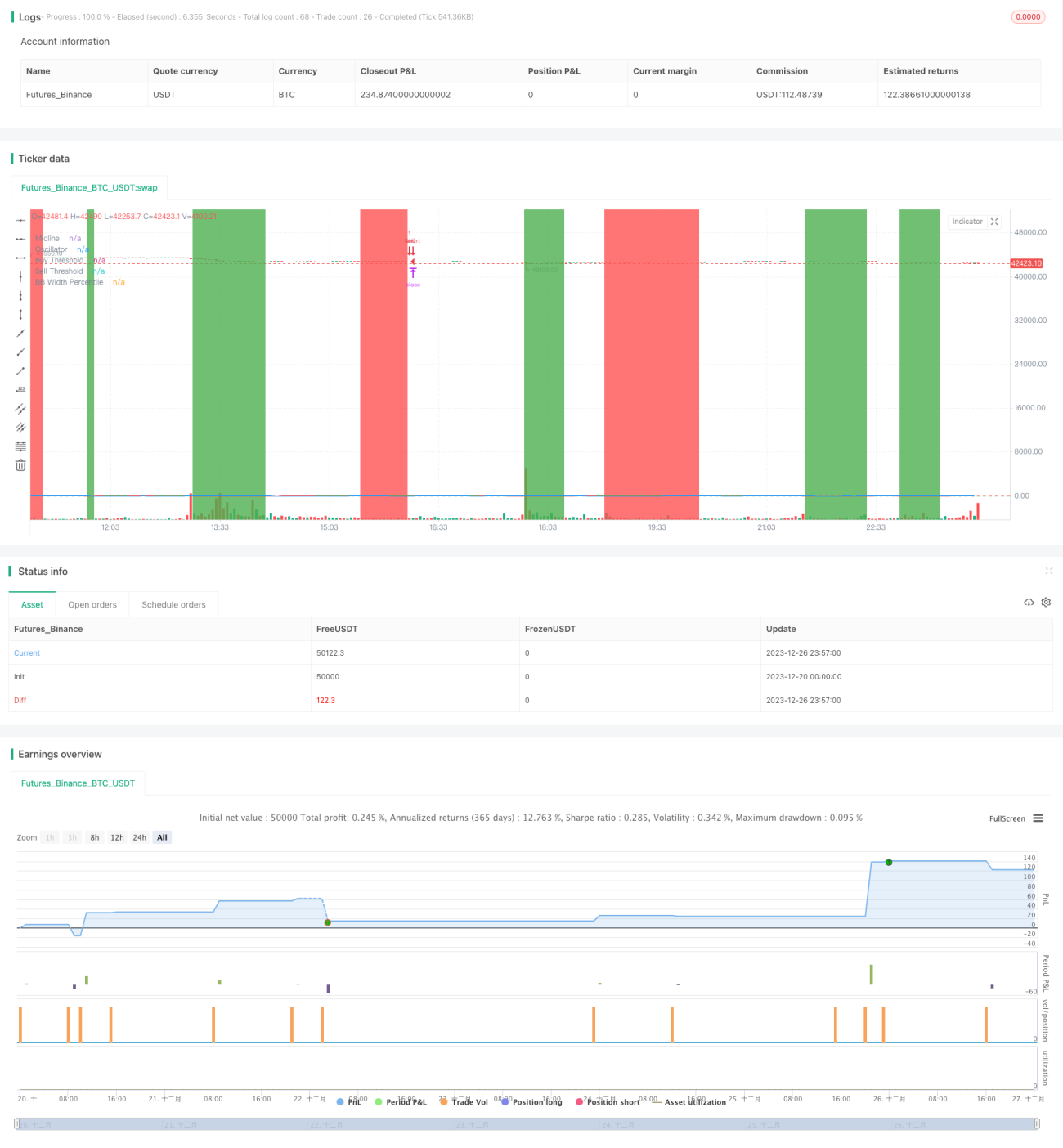

Esta estratégia é uma estratégia de seguimento de tendência baseada no indicador de dupla média móvel, combinando um filtro de Bandas de Bollinger e um indicador de dupla filtragem de tendência, utilizando um mecanismo de saída em cadeia. A estratégia visa identificar a direção da tendência de médio a longo prazo através do indicador de razão de médias móveis, escolher bons pontos de entrada quando a direção da tendência é clara, e definir mecanismos de saída de take profit e stop loss para bloquear lucros e reduzir perdas.

Princípio da Estratégia

- Calcular a média móvel rápida (10 períodos) e a média móvel lenta (50 períodos), e calcular sua razão, chamada de razão de média móvel de preço. Essa razão pode identificar eficazmente as mudanças na tendência de médio a longo prazo do preço.

- Converter a razão de média móvel de preço em um percentil, ou seja, a força relativa da razão atual em um determinado período passado. Esse percentil é definido como o oscilador.

- Quando o oscilador cruza acima do limite de compra definido (10), gera um sinal de compra; quando cruza abaixo do limite de venda (90), gera um sinal de venda, realizando o seguimento de tendência.

- Combinar o indicador de largura das Bandas de Bollinger para filtrar os sinais de negociação, operando quando as Bandas de Bollinger se estreitam.

- Utilizar um indicador de dupla filtragem de tendência: só gerar sinal de compra quando o preço está em um canal de tendência de alta, e só gerar sinal de venda quando o preço está em um canal de tendência de baixa, evitando assim operações contra a tendência.

- Definir um mecanismo de saída em cadeia, incluindo take profit, stop loss e saída combinada, podendo pré-definir várias condições de saída, priorizando a saída que maximize o lucro.

Vantagens da Estratégia

- Mecanismo de dupla filtragem de tendência, que avalia de forma confiável a direção principal da tendência, evitando operações contra a tendência.

- O indicador de razão de média móvel é mais eficaz do que uma única média móvel para identificar mudanças de tendência.

- O indicador de largura das Bandas de Bollinger identifica eficazmente períodos de baixa volatilidade do mercado, onde os sinais de negociação são mais confiáveis.

- O mecanismo de saída em cadeia torna os lucros mais estáveis, maximizando o lucro total.

Riscos e Soluções

- Em mercados laterais sem tendência clara, podem ocorrer muitos sinais falsos e reversões. A solução é combinar a filtragem de largura das Bandas de Bollinger, operando quando há estreitamento.

- Quando ocorre uma reversão clara da tendência, as médias móveis podem apresentar atraso, não identificando imediatamente o sinal de reversão. A solução é reduzir adequadamente os parâmetros do período das médias móveis.

- Quando ocorrem gaps de preço, o stop loss pode ser acionado instantaneamente, causando grandes perdas. A solução é ampliar adequadamente os parâmetros do stop loss.

Direções de Otimização da Estratégia

- Otimização de parâmetros. Pode-se realizar testes exaustivos nos períodos das médias móveis, pontos de compra/venda do oscilador, parâmetros das Bandas de Bollinger e parâmetros de filtragem de tendência para encontrar a melhor combinação.

- Incorporação de outros indicadores. Pode-se considerar a adição de outros indicadores de reversão de tendência, como Estocástico (KD), MACD, etc., para melhorar a precisão da estratégia.

- Aprendizado de máquina. Pode-se coletar dados históricos e utilizar algoritmos de aprendizado de máquina para treinar modelos, otimizando dinamicamente vários parâmetros e realizando ajustes adaptativos.

Resumo

Esta estratégia combina o indicador de dupla razão de média móvel e o indicador de Bandas de Bollinger para determinar a direção da tendência de médio a longo prazo. Após confirmar a tendência, busca o melhor ponto de entrada e define um mecanismo de saída em cadeia para bloquear lucros. Apresenta alta confiabilidade e resultados significativos. A estratégia pode ser melhorada e ter sua taxa de lucro aumentada através da otimização de parâmetros, adição de outros indicadores auxiliares e aprendizado de máquina.

- 1