Estratégia de investimento periódico com custo médio dinâmico e capitalização composta

Visão Geral

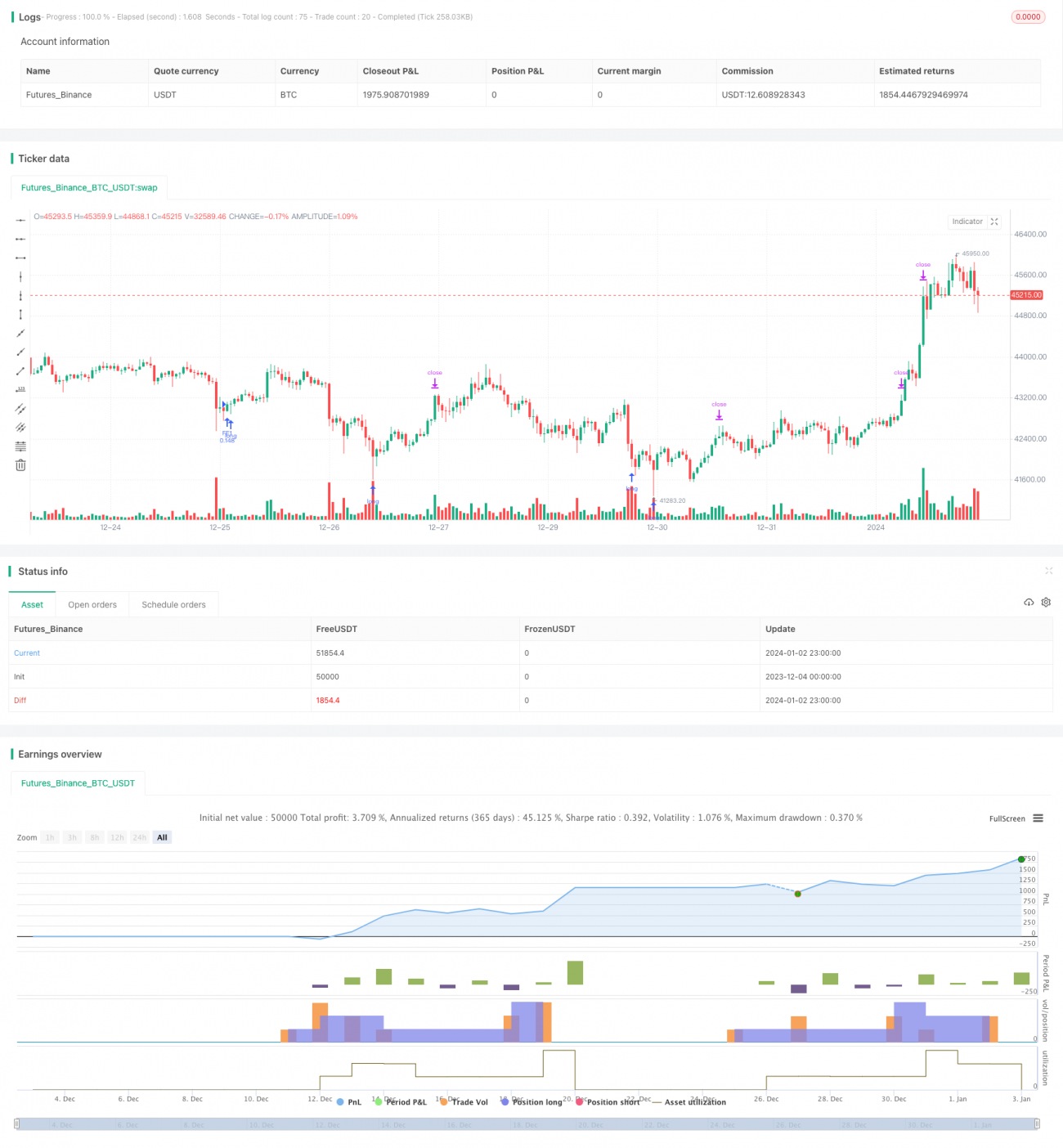

A estratégia de investimento com custo médio dinâmico e juros compostos ajusta dinamicamente a quantidade de cada abertura de posição, começando com uma pequena quantidade no início da tendência e aumentando gradualmente a posição à medida que a profundidade da consolidação aumenta. A estratégia utiliza uma função exponencial para calcular o nível de stop loss de cada camada e aciona a reabertura de novas posições em lotes, permitindo que a linha de custo da posição desça de forma exponencial. Com o aumento da profundidade, o custo da posição pode ser gradualmente comprimido para baixo. Após a reversão do preço, as posições são fechadas em lotes para obter lucros maiores.

Princípio da Estratégia

Esta estratégia combina sinais simples de oversold do RSI com uma média móvel para selecionar o momento de abertura de posição. Quando o RSI está abaixo da linha de oversold e o preço de fechamento é menor que a média móvel, gera-se um sinal para a primeira ordem. Após a abertura da primeira ordem, com base em uma função exponencial, calcula-se o limite inferior de queda do preço, gerando um sinal de DCA (Dollar-Cost Averaging). A cada DCA, ajusta-se a quantidade da posição para que cada lote seja igual. Devido às mudanças dinâmicas na quantidade e no custo da posição, isso gera um efeito semelhante ao de alavancagem. À medida que o número de DCAs aumenta, o custo da posição continua caindo, exigindo apenas um pequeno rebote para obter lucro em cada fechamento parcial.

Após a abertura de várias ordens consecutivas, uma linha de stop loss é desenhada acima do preço médio. Quando o preço rompe para cima, ultrapassando o custo médio e a linha de stop loss, a posição é fechada com stop loss.

A maior vantagem da estratégia é que, à medida que o custo da posição diminui, mesmo em um mercado lateral, é possível acumular e reduzir gradualmente os custos. Quando a tendência se inverte, como o custo da posição já está muito abaixo do preço de mercado, é possível obter lucros maiores.

Riscos e Deficiências

O maior risco desta estratégia é a quantidade limitada de posições no início. Em uma tendência de queda contínua, há risco de stop loss. Portanto, é necessário definir uma margem de stop loss que seja aceitável.

Além disso, a definição da margem de stop loss também apresenta dois extremos. Se a margem for muito grande, pode não capturar um rebote profundo o suficiente. Se a margem for muito pequena, a probabilidade de o preço sofrer uma reversão total em uma correção de médio prazo é maior. Portanto, é crucial escolher uma margem de stop loss adequada com base no mercado e na tolerância ao risco do investidor.

Quando o ciclo de DCA é longo e muitos níveis são formados, se o preço subir significativamente, a posição pode enfrentar o risco de um custo muito alto e impossibilidade de stop loss. Isso também requer a definição razoável dos níveis de DCA com base na quantidade total da posição e no custo máximo suportável.

Sugestões de Otimização

-

Otimizar os sinais de tempo. É possível testar diferentes parâmetros e combinações de indicadores para obter sinais com maior taxa de acerto.

-

Otimizar o mecanismo de stop loss. Pode-se testar o uso de stop loss em forma de "Λ" ou stop loss arredondado para substituir o stop loss móvel simples, o que pode resultar em melhor eficácia. Também é possível adicionar uma estratégia de ajuste da margem de stop loss baseada na divisão temporal da posição.

-

Otimizar a forma de realizar lucros. Pode-se testar diferentes tipos de take profit móvel para encontrar melhores oportunidades de saída, aumentando assim a taxa de retorno geral.

-

Adicionar um mecanismo anti-rebote. Após o stop loss, pode ocorrer um novo gatilho de sinal de DCA, reabrindo a posição. Nesse caso, pode-se considerar adicionar uma margem anti-rebote de amplitude definida para evitar uma reabertura agressiva imediatamente após o stop loss.

Resumo

Esta estratégia utiliza o indicador RSI para determinar o momento de compra, combinado com uma estratégia DCA dinâmica baseada em função exponencial para stop loss. Isso permite ajustar dinamicamente a quantidade e o custo da posição, obtendo vantagem de preço em mercados de oscilação. As otimizações concentram-se principalmente nos sinais de entrada e saída, métodos de stop loss e take profit. No geral, a estratégia utiliza o conceito central de DCA exponencial, fazendo com que o custo da posição caia continuamente. Isso proporciona mais espaço de manobra durante períodos de consolidação e maior retorno em movimentos de tendência. No entanto, ainda é necessário escolher parâmetros adequados com base no plano de gerenciamento de capital para controlar o risco geral da posição.

- 1