Estratégia de Cruzamento de Combinação de Onze Médias Móveis

Visão Geral

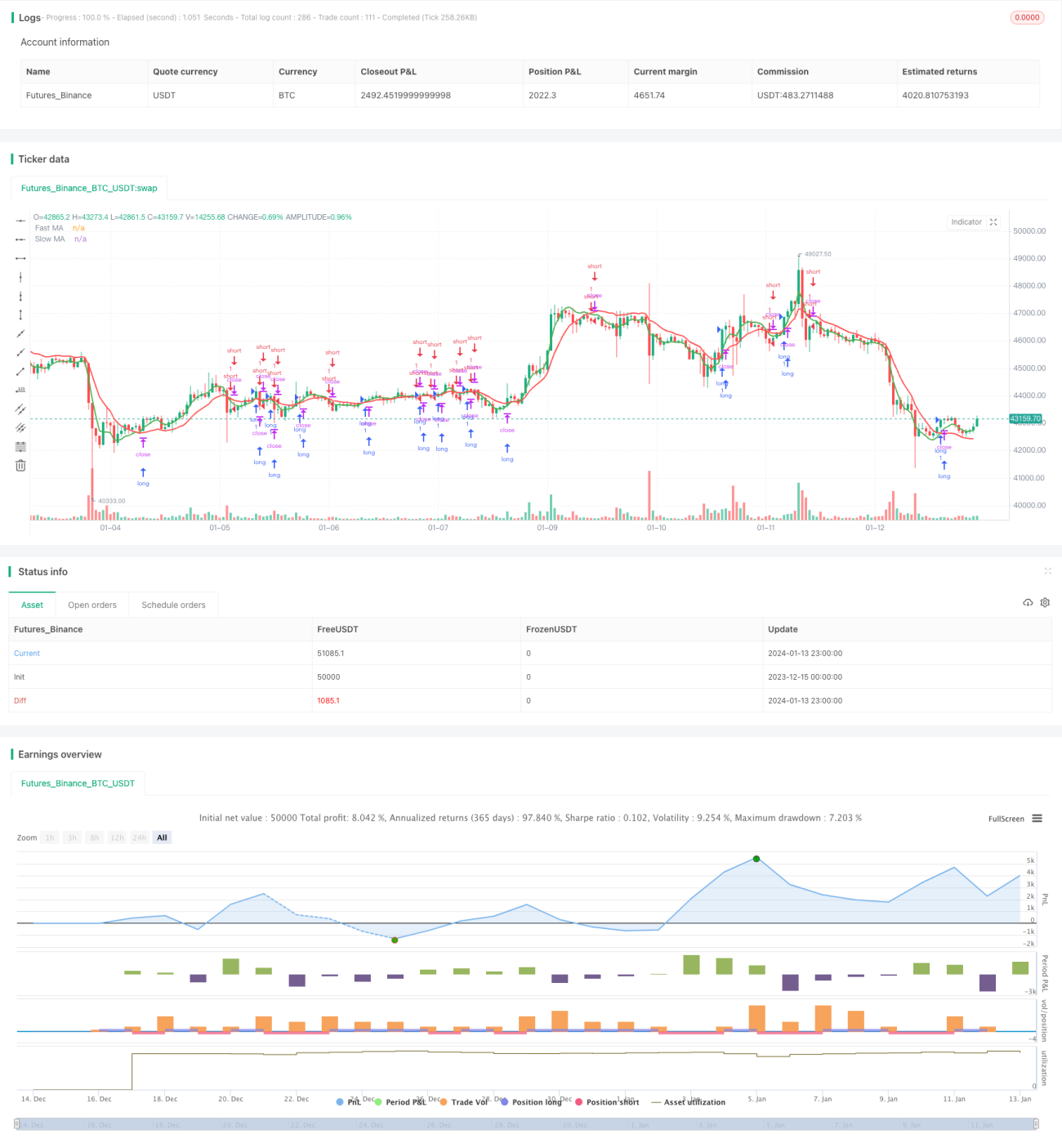

Esta estratégia combina cruzamentos de 11 tipos diferentes de médias móveis para realizar operações de compra (long) e venda (short). As 11 médias móveis utilizadas são: Média Móvel Simples (SMA), Média Móvel Exponencial (EMA), Média Móvel Ponderada (WMA), Média Móvel Ponderada por Volume (VWMA), Média Móvel Suavizada (SMMA), Média Móvel Exponencial Dupla (DEMA), Média Móvel Exponencial Tripla (TEMA), Média Móvel de Hull (HMA), Média Móvel Exponencial com Atraso Zero (ZEMA), Média Móvel Triangular (TMA) e Filtro Super Suave (SSMA).

A estratégia permite configurar duas médias móveis — uma mais rápida e uma mais lenta, ambas escolhidas entre as 11 opções. Quando a MM rápida cruza acima da MM lenta, gera-se um sinal de compra. Quando a MM rápida cruza abaixo da MM lenta, gera-se um sinal de venda.

Funcionalidades adicionais incluem configuração de escada, níveis de Take Profit e Stop Loss.

Lógica da Estratégia

A lógica central da estratégia depende do cruzamento entre duas médias móveis para determinar entradas e saídas.

As condições de entrada são:

Entrada de compra: MM rápida > MM lenta

Entrada de venda: MM rápida < MM lenta

A saída é determinada por um dos três critérios a seguir:

- Nível de Take Profit atingido

- Nível de Stop Loss atingido

- Geração de sinal oposto (cruzamento das médias móveis na direção contrária)

A estratégia permite configurar parâmetros-chave, como tipo e comprimento das MMs, configuração de escada, percentuais de Take Profit e Stop Loss. Isso oferece flexibilidade para otimizar a estratégia de acordo com diferentes condições de mercado e perfis de risco.

Vantagens

- Combina 11 tipos diferentes de MM para gerar sinais robustos

- Configuração flexível dos parâmetros principais

- Funções de Take Profit e Stop Loss protegem lucros e limitam perdas

- Escada permite aumentar posições durante tendências fortes

Riscos

- Como qualquer indicador técnico, os cruzamentos de MM podem gerar sinais falsos

- A otimização excessiva para condições atuais de mercado pode reduzir o desempenho futuro

- Stop Loss fixo pode encerrar prematuramente operações corretas em mercados voláteis

A gestão de risco pode ser aprimorada utilizando confirmação de preço para sinais de entrada, empregando stop loss trailing em vez de stop loss fixo e evitando otimização excessiva.

Espaço para Otimização

É possível melhorar a estratégidade de várias maneiras:

- Adicionar filtros extras antes da entrada, como volume e verificação de preço

- Testar sistematicamente o desempenho de diferentes tipos de MM e selecionar os 1-2 melhores

- Otimizar os comprimentos das MM para ativos e períodos específicos

- Utilizar stop loss trailing em vez de stop loss fixo

- Adicionar Take Profit escalonado à medida que a tendência se estende

Resumo

A estratégia de cruzamento de onze médias móveis oferece uma abordagem sistemática para negociar cruzamentos. Ao combinar sinais de múltiplos indicadores de MM e permitir a configuração de parâmetros-chave, ela fornece uma estrutura de negociação robusta e flexível. A otimização e a gestão de risco desempenharão papéis fundamentais na melhoria do desempenho. A estratégia possui forte potencial em negociação de momentum, mas deve ser ajustada conforme as diferentes condições de mercado.

- 1