Estratégia Quantitativa de Combinação de Médias Móveis Triplas e MACD

Visão Geral

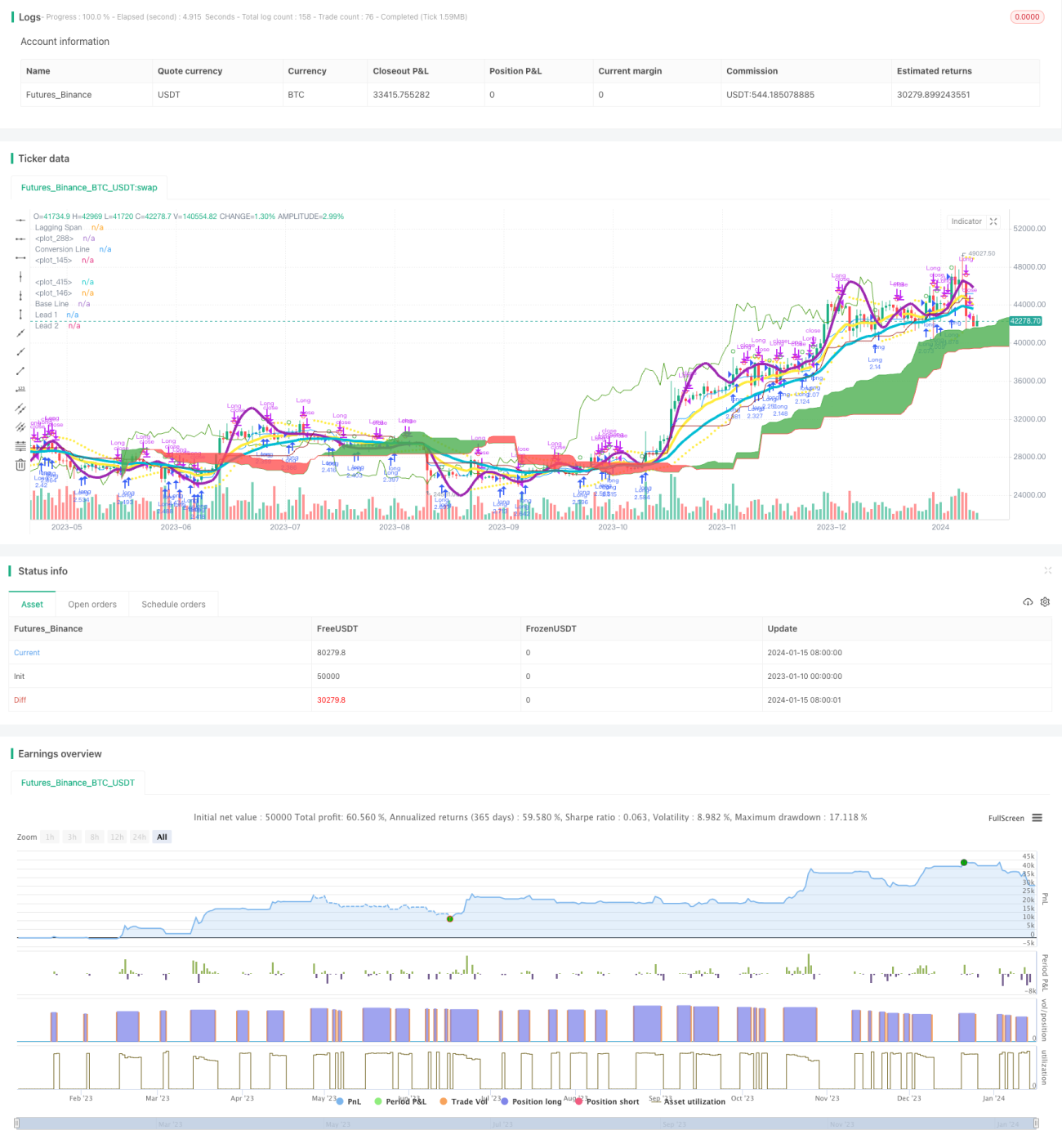

Esta estratégia desenvolve uma estratégia de negociação quantitativa relativamente estável e confiável combinando o uso do indicador de tripla média móvel e do indicador MACD. A estratégia visa capturar tendências futuras que possam surgir, sendo especialmente adequada para posições de médio e longo prazo.

Princípio da Estratégia

A estratégia baseia-se principalmente no uso combinado de triplas médias móveis e do indicador MACD.

Primeiramente, a estratégia utiliza triplas médias móveis exponenciais com comprimentos de 3, 7 e 2. Estas três médias móveis constroem um sistema de médias móveis que varia de rápido a lento, utilizado para determinar a direção da tendência futura. Quando a média móvel de curto prazo cruza acima da média móvel de longo prazo, é um sinal de compra; quando a média móvel de curto prazo cruza abaixo da média móvel de longo prazo, é um sinal de venda.

Em segundo lugar, a estratégia também utiliza simultaneamente o indicador MACD com parâmetros 3 e 7. Quando a linha principal do MACD cruza acima da linha de sinal, é um sinal de compra; quando cruza abaixo, é um sinal de venda.

Ao usar indicadores duplos em combinação, é possível evitar múltiplos sinais falsos gerados por um único indicador, aumentando assim a estabilidade da estratégia.

Vantagens da Estratégia

- Utiliza filtro de indicadores duplos, melhorando a qualidade dos sinais

- Parâmetros otimizados através de múltiplos testes, estáveis e confiáveis

- O sistema de tripla média móvel filtra eficazmente o ruído do mercado e identifica tendências futuras

- Os parâmetros do MACD são definidos como rápidos, capturando rapidamente oportunidades de curto prazo

Riscos da Estratégia

- Existe certo risco de drawdown e perdas consecutivas

- Quando o mercado não apresenta uma tendência clara, a estratégia gera um número maior de negociações erradas

- O indicador MACD tende a produzir sinais falsos, necessitando de uso combinado com indicadores de média móvel

Soluções:

- Adotar uma estratégia adequada de stop loss para controlar o drawdown máximo

- Quando o estado do mercado estiver claramente sem tendência, reduzir a frequência de negociações

- Otimizar os parâmetros do MACD e combiná-lo com outros indicadores

Direções de Otimização da Estratégia

- Testar e otimizar os parâmetros das médias móveis e do MACD para encontrar a melhor combinação

- Adicionar indicadores auxiliares como KDJ, VRSI, etc., para evitar sinais falsos

- Incorporar modelos de aprendizado de máquina para avaliar o estado do mercado, permitindo ajustes dinâmicos

- Combinar com estratégias de stop loss, definindo os melhores pontos de stop loss

Resumo

Esta estratégia alcança uma captura estável de tendências através da combinação de médias móveis e MACD. Sua vantagem reside no uso combinado de indicadores, reduzindo efetivamente sinais falsos e obtendo melhores resultados estratégicos. Como próximos passos, aprimorar ainda mais a estratégia por meio de otimização de parâmetros, introdução de stop loss e ajustes dinâmicos, tornando-a uma ferramenta eficaz para buscar oportunidades de médio e longo prazo.

/*backtest

start: 2023-01-10 00:00:00

end: 2024-01-16 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

strategy("Matt's MACD Algo v1", shorttitle="Matt's MACD Algo v1", overlay=true, pyramiding = 0, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital=7000, calc_on_order_fills = true, commission_type=strategy.commission.percent, commission_value=0, currency = currency.USD)

//study("MFI Fresh", shorttitle="MFI Fresh", overlay=true)

- 1