Modelo de Reversão de Rompimento Baseado na Estratégia dos Traders Tartaruga

Visão Geral

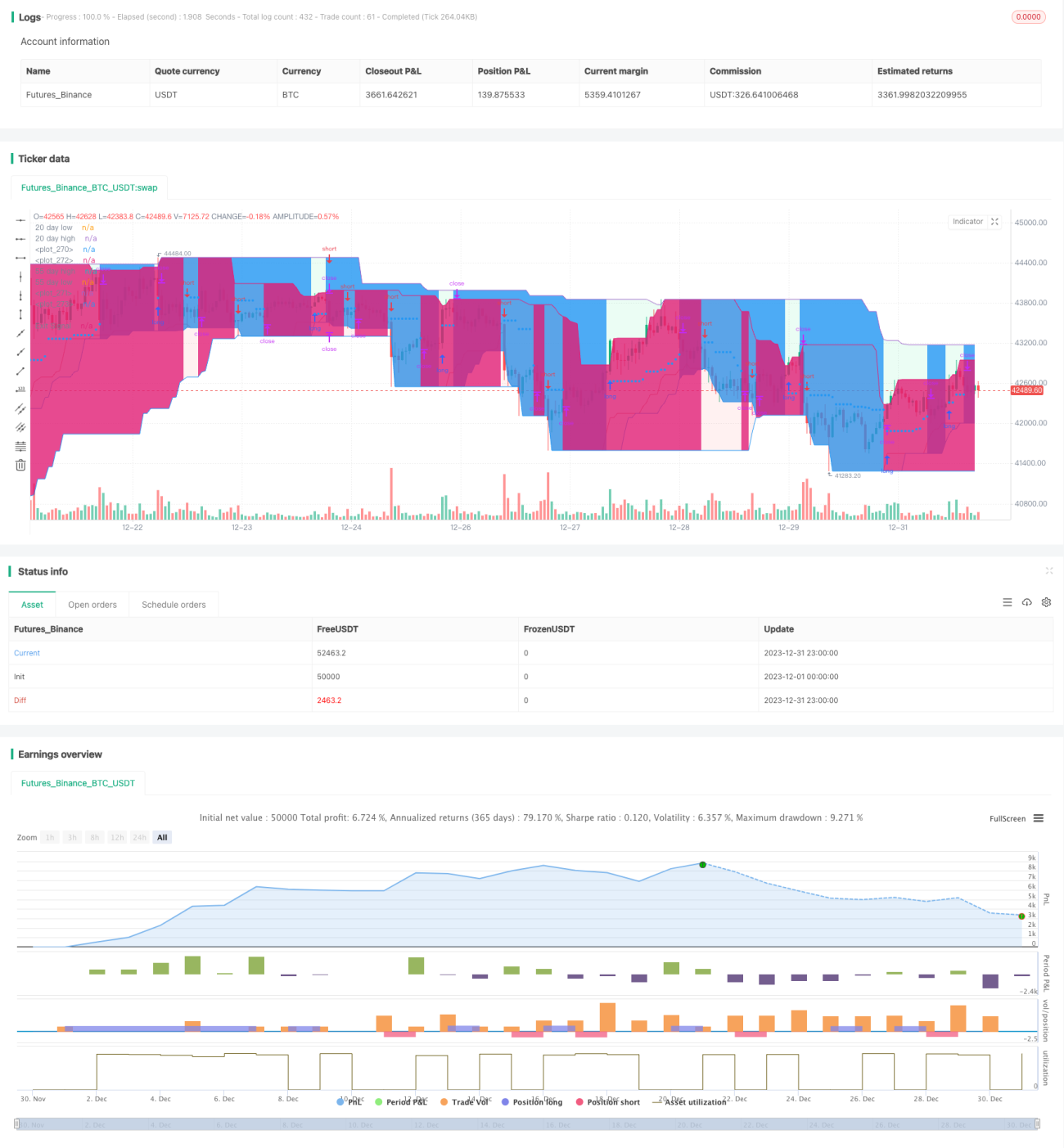

Esta estratégia é baseada na famosa "Estratégia dos Traders Tartaruga", que foi validada ao longo de muitos anos. Ela envia sinais de posições compradas e vendidas, permitindo até 5 ordens piramidais, o que significa que a estratégia pode acionar até 5 ordens na mesma direção. Possui uma boa gestão de risco e capital.

É importante notar que a estratégia combina dois sistemas que funcionam em conjunto (S1 e S2).

Princípio da Estratégia

O tamanho da posição é muito importante para os Traders Tartaruga, a fim de administrar adequadamente o risco. Esta estratégia de ajuste de posição se adapta à volatilidade do mercado e à conta (ganhos e perdas). Ela é baseada no ATR (Average True Range), também conhecido como "N". Seu comprimento padrão é 20.

O número de unidades compradas é:

unit = (percentage_to_risk/100)*account/atr*syminfo.pointvalue

De acordo com sua tolerância ao risco, você pode aumentar a porcentagem da conta, mas o padrão dos Traders Tartaruga é 1%. Se você negociar contratos, as unidades devem ser arredondadas para baixo por padrão.

Há também uma regra adicional para reduzir o risco quando o valor da conta fica abaixo do capital inicial: neste caso, na fórmula da unidade, deve-se substituir por:

account := (strategy.equity-strategy.openprofit)*(strategy.equity-strategy.openprofit)/strategy.initial_capital

Existem dois sistemas trabalhando juntos:

Um rompimento é uma nova máxima ou nova mínima. Se for uma nova máxima, abrimos uma posição comprada; inversamente, se for uma nova mínima, entramos em uma posição vendida.

Adicionamos uma regra extra:

Esta regra extra permite que o trader participe da tendência principal, caso o sinal do Sistema 1 seja ignorado. Se o sinal do Sistema 1 for ignorado e a próxima vela também for um novo rompimento de 20 períodos, o S1 não emitirá sinal. Devemos esperar pelo sinal do S2 ou por uma vela que não produza um novo rompimento para reativar o S1.

Análise de Vantagens

A estratégia Tartaruga permite adicionar unidades extras à posição quando o movimento do preço é favorável. Configurei a estratégia para permitir adicionar até 5 ordens na mesma direção. Portanto, se o preço se mover a nosso favor, adicionamos unidades.

Definimos a primeira ordem (comprada ou vendida) como a ordem máxima. As ordens piramidais subsequentes terão menos unidades do que a primeira ordem.

Definimos um stop loss máximo de 10% para a primeira ordem, o que significa que você não perderá mais do que 10% do valor da primeira ordem. No entanto, como o stop loss aumenta/diminui em 0,5 * ATR(20), suas ordens piramidais podem perder mais, e neste caso a perda de 10% não será garantida. O risco ainda é bem administrado, pois essas ordens têm valor menor do que a primeira ordem.

Análise de Risco

O maior risco desta estratégia é o tamanho excessivo da posição. Como as ordens são colocadas como ordens a mercado, se várias ordens a mercado de grande volume forem executadas simultaneamente, haverá um grande impacto na cotação, causando um grande deslizamento. Isso pode resultar em perdas substanciais de capital.

Outro risco é uma configuração inadequada de gerenciamento de capital. Se o stop loss for configurado incorretamente ou a porcentagem for muito grande, podem ocorrer perdas enormes. É necessário configurar cuidadosamente de acordo com sua própria tolerância ao risco.

Direções de Otimização

A estratégia pode ser otimizada nos seguintes aspectos:

-

Testar diferentes parâmetros no impacto sobre a taxa de retorno e o índice de Sharpe, como o período do ATR, o múltiplo do ATR para o stop loss, etc. Encontrar a combinação ideal de parâmetros.

-

Testar diferentes regras de entrada e saída. Por exemplo, usar formações de candlestick como filtros adicionais.

-

Experimentar outros tipos de stop loss, como stop loss móvel ou dinâmico. Isso pode reduzir a probabilidade de o stop loss ser atingido.

-

Testar diferentes quantidades de ordens piramidais. Quanto mais ordens, maior a alavancagem e o risco. Encontrar o ponto de equilíbrio ideal.

-

Tentar interromper a negociação em períodos específicos (por exemplo, antes da divulgação dos dados de emprego não-agrícolas dos EUA) para evitar o impacto de eventos importantes.

Resumo

No geral, esta estratégia apresenta um bom equilíbrio entre risco e retorno, sendo adequada para negociação de tendências de médio a longo prazo. Ela possui vantagens como sistematização da negociação e risco controlável. Através da otimização, é possível melhorar ainda mais a estabilidade e a taxa de retorno da estratégia.

- 1