Estratégia de acompanhamento de tendência baseada em múltiplos indicadores

Visão Geral

Esta estratégia identifica tendências combinando múltiplos indicadores e define um stop loss de acompanhamento de tendência para bloquear lucros. Utiliza principalmente Bandas de Bollinger, RSI, ADX, entre outros, para determinar o momento de entrada, bem como ATR e Bandas de Bollinger para o stop loss.

Princípio da Estratégia

Os principais indicadores da estratégia são Bandas de Bollinger, RSI e ADX. Quando o preço se aproxima da banda inferior de Bollinger e o RSI está abaixo de 30, considera-se sobrevendido e abre-se posição comprada; quando o preço se aproxima da banda superior de Bollinger e o RSI está acima de 70, considera-se sobrecomprado e abre-se posição vendida. Além disso, se o ADX estiver acima de 25, considera-se que uma tendência está formada, tornando os sinais de compra e venda mais eficazes.

Após abrir a posição, a estratégia utiliza o indicador ATR e as bandas superior e inferior de Bollinger para definir o stop loss. Especificamente, o ATR é usado para definir a distância máxima de stop loss; quando o preço atinge o ponto de stop loss máximo, a posição é encerrada. As bandas superior e inferior de Bollinger são usadas para definir um stop loss móvel, que é atualizado em tempo real conforme o movimento do preço.

Análise de Vantagens

Esta estratégia combina múltiplos indicadores para identificar tendências de forma eficaz e utiliza mecanismos de stop loss para bloquear lucros e reduzir riscos de perda, sendo uma estratégia relativamente robusta. As vantagens específicas são:

- Utiliza as Bandas de Bollinger para identificar condições de sobrecompra e sobrevenda, permitindo detectar oportunidades de reversão.

- A combinação com o indicador RSI aumenta a precisão das decisões.

- O indicador ADX confirma a formação da tendência, garantindo a direção correta da negociação.

- O stop loss móvel baseado em ATR e Bandas de Bollinger maximiza o bloqueio de lucros.

Análise de Riscos

A estratégia também apresenta alguns riscos:

- O uso de múltiplos indicadores pode tornar os parâmetros propensos a overfitting.

- Quando as Bandas de Bollinger estão muito largas, os sinais de sobrecompra/sobrevenda tornam-se menos eficazes.

- Um stop loss móvel inadequado pode levar ao aumento das perdas.

Para mitigar esses riscos, podemos adotar as seguintes medidas:

- Otimizar múltiplas combinações de parâmetros para evitar overfitting.

- Ajustar os parâmetros das Bandas de Bollinger de acordo com a volatilidade do mercado.

- Testar a distância do stop loss para garantir que a estratégia suporte flutuações normais.

Direções de Otimização

A estratégia pode ser otimizada nas seguintes áreas:

- Adicionar controle de tamanho de posição, ajustando o volume conforme o multiplicador do stop loss.

- Incluir um módulo de gerenciamento de capital para controlar rigorosamente o valor máximo de perda por negociação.

- Testar outros indicadores de stop loss, como DMI, Envelopes, etc.

- Incorporar modelos de aprendizado de máquina para estimar a probabilidade de tendência, melhorando o desempenho.

Resumo

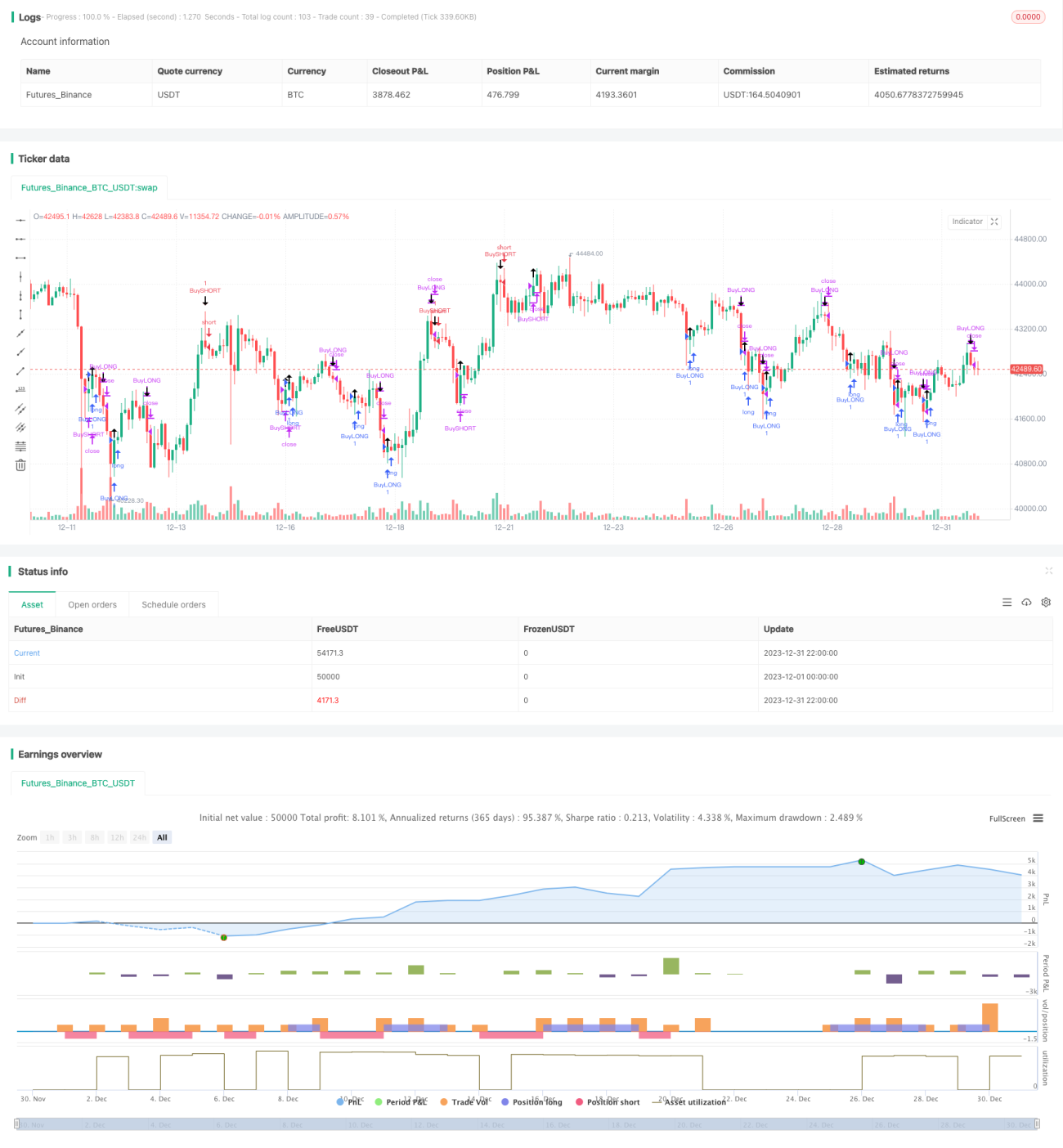

No geral, esta estratégia é um sistema de acompanhamento de tendências relativamente robusto. Ao determinar a direção da tendência com múltiplos indicadores e controlar o risco por meio de stop loss, é possível obter boas taxas de retorno. Também propusemos várias direções de otimização que, se implementadas, podem trazer resultados ainda melhores.

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

// THIS SCRIPT IS MEANT TO ACCOMPANY COMMAND EXECUTION BOTS

// THE INCLUDED STRATEGY IS NOT MEANT FOR LIVE TRADING

// THIS STRATEGY IS PURELY AN EXAMLE TO START EXPERIMENTATING WITH YOUR OWN IDEAS- 1