Estratégia de Rompimento de Momentum com Duas Médias Móveis

Visão Geral

A Estratégia de Ruptura de Momentum com Duas Médias Móveis (Dupla MA) é uma estratégia de negociação quantitativa que combina duas médias móveis e o indicador RSI. A estratégia calcula a média móvel rápida, a média móvel lenta e o indicador RSI, definindo limites de sobrecompra e sobrevenda para o indicador de momentum RSI. Quando ocorre um cruzamento dourado das duas MAs, a posição é comprada; quando ocorre um cruzamento da morte, a posição é vendida, visando capturar movimentos de tendência do mercado.

Princípio da Estratégia

A Estratégia de Ruptura de Momentum com Duas MAs baseia-se principalmente em duas médias móveis e no indicador RSI. Primeiro, calculam-se duas médias móveis: uma rápida e uma lenta. A linha rápida é uma média móvel ponderada de 10 períodos, e a linha lenta é uma média móvel adaptativa linear de 100 períodos. Em seguida, calcula-se o RSI de 14 períodos e definem-se os limites de sobrecompra e sobrevenda. Quando a linha rápida cruza acima da linha lenta, considera-se um mercado de alta; quando a linha rápida cruza abaixo da linha lenta, considera-se um mercado de baixa. Além de determinar a direção do mercado, é necessário que o RSI esteja acima do limite de sobrecompra ou abaixo do limite de sobrevenda, filtrando assim eficazmente falsos rompimentos.

Especificamente, quando se identifica um mercado de alta e o RSI está acima do limite de sobrecompra, abre-se uma posição comprada; quando se identifica um mercado de baixa e o RSI está abaixo do limite de sobrevenda, abre-se uma posição vendida. Após a abertura da posição, quando o sinal de negociação se inverte, realiza-se a abertura da posição oposta.

Vantagens da Estratégia

A Estratégia de Ruptura de Momentum com Duas MAs combina os indicadores de Dupla MA e RSI, identificando eficazmente as tendências do mercado e utilizando o RSI para filtrar falsos rompimentos, aumentando assim a confiabilidade dos sinais de negociação. Em comparação com um sistema de MA único, esta estratégia pode reduzir significativamente a ocorrência de negociações ineficazes. Além disso, a otimização dos parâmetros do RSI confere flexibilidade à estratégia.

Riscos da Estratégia

A Estratégia de Ruptura de Momentum com Duas MAs também apresenta certos riscos. O sistema de Dupla MA é muito sensível aos parâmetros, exigindo uma cuidadosa testagem de combinações de parâmetros para diferentes mercados. Além disso, se os limites do RSI não forem definidos corretamente, podem perder oportunidades de negociação. Por fim, um stop loss móvel agressivo pode ser rompido em determinadas condições de mercado; é necessário ajustar o ponto de stop loss com base nos resultados do backtest.

Otimização da Estratégia

A Estratégia de Ruptura de Momentum com Duas MAs pode ser otimizada nos seguintes aspectos:

- Otimizar os parâmetros das MAs rápida e lenta para encontrar a melhor combinação.

- Otimizar os parâmetros do RSI, ajustando os limites de sobrecompra e sobrevenda.

- Adicionar um mecanismo de stop loss móvel adaptativo para controlar riscos.

- Adicionar um módulo de otimização do tamanho da posição para melhorar a eficiência do uso do capital.

Resumo

A Estratégia de Ruptura de Momentum com Duas MAs utiliza o sistema de Dupla MA para determinar a direção da tendência e o RSI para filtrar sinais, melhorando eficazmente as desvantagens de um sistema de MA único. Esta estratégia possui grande espaço para otimização de parâmetros e pode ser ajustada adaptativamente, sendo uma excelente estratégia de acompanhamento de tendências.

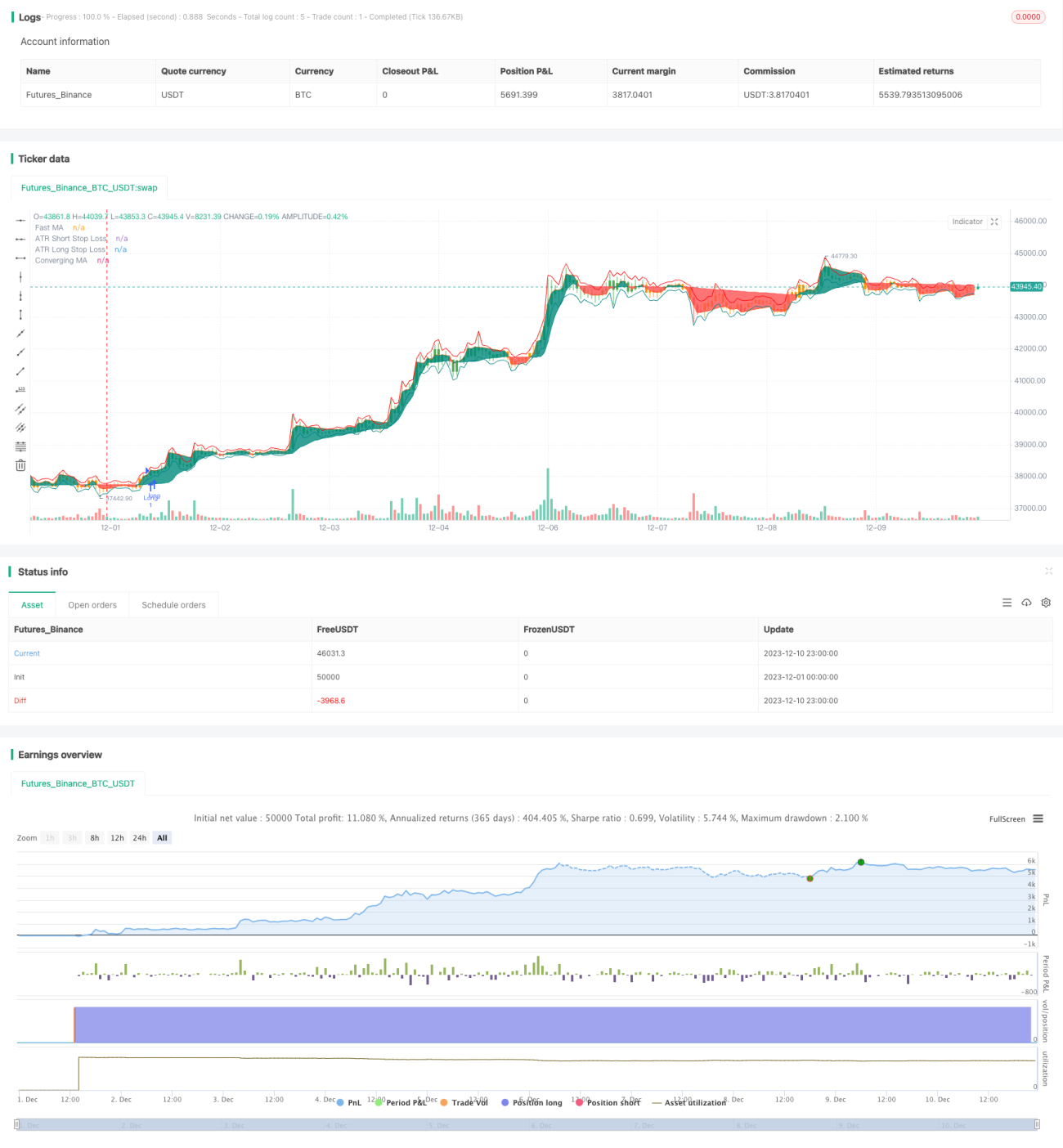

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-10 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This work is licensed under a Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0) https://creativecommons.org/licenses/by-nc-sa/4.0/

// © Salman4sgd

//@version=5- 1