Estratégia de stop-loss de acompanhamento de tendência do RSI

Visão Geral

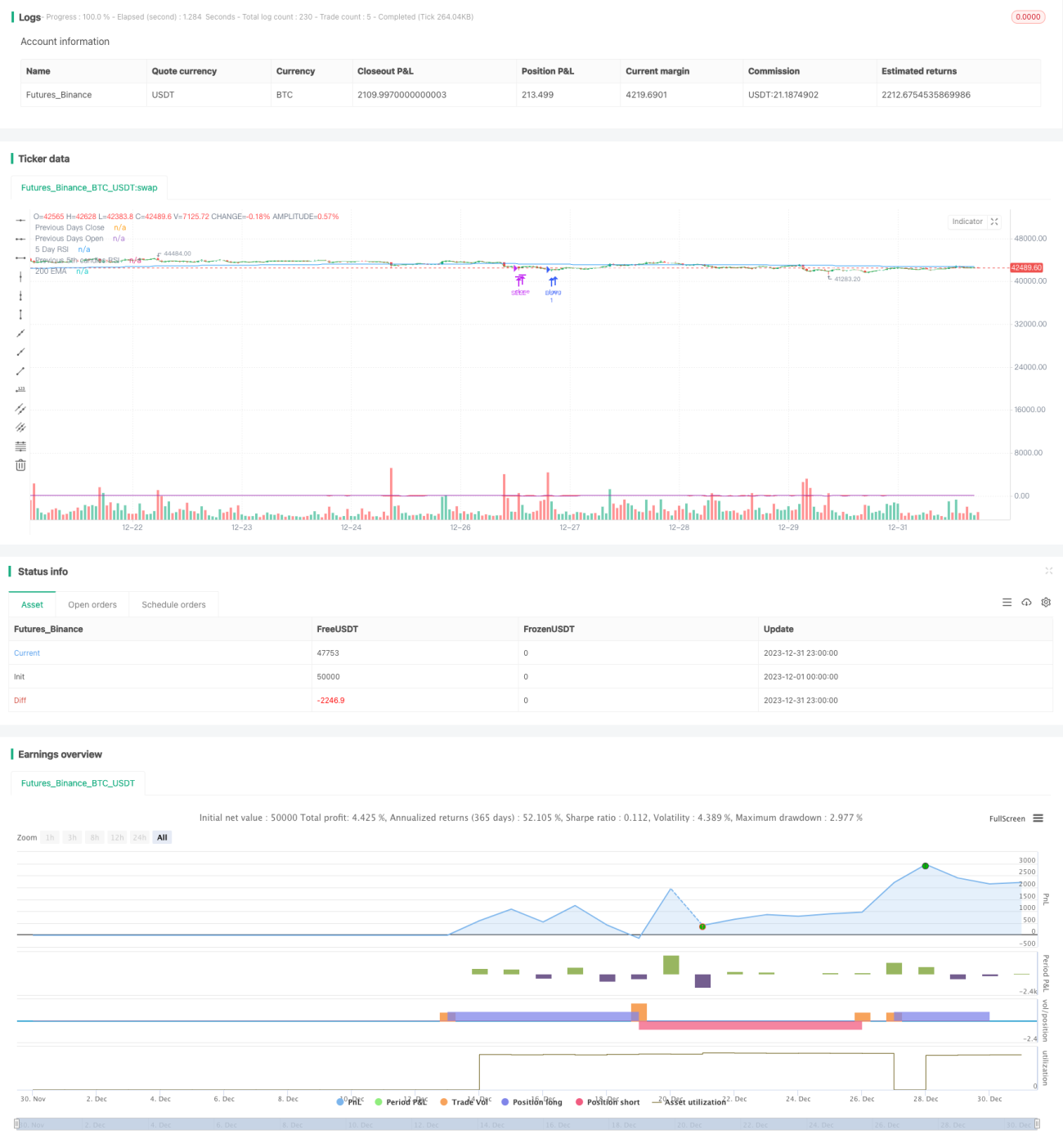

Esta é uma estratégia de trading quantitativo que utiliza o indicador RSI para identificar tendências e definir stop loss e take profit. A estratégia combina o indicador RSI para determinar a direção da tendência do mercado, bem como define stop loss e take profit dinâmicos para travar lucros e minimizar riscos.

Princípio da Estratégia

A estratégia determina principalmente a direção da tendência do mercado utilizando o indicador RSI para decidir entre comprar (long) ou vender (short). Quando o RSI cruza acima da linha de sobrevenda, considera-se que o mercado está em tendência de alta, e faz-se uma posição comprada (long). Quando o RSI cruza abaixo da linha de sobrecompra, considera-se que o mercado está em tendência de baixa, e faz-se uma posição vendida (short).

Ao mesmo tempo, a estratégia monitora o preço de abertura de cada ordem e define stop loss e take profit flutuantes. Para ordens compradas, define-se uma percentagem do preço de abertura como linha de stop loss; para ordens vendidas, define-se uma percentagem do preço de abertura como linha de take profit. Quando o preço toca essas linhas, a estratégia fecha automaticamente a posição para limitar perdas ou garantir lucros.

Vantagens da Estratégia

- Utiliza o indicador RSI para identificar a direção da tendência do mercado, evitando negociar em zonas de consolidação.

- Define stop loss e take profit flutuantes, o que permite travar lucros de forma flexível e controlar riscos de maneira eficaz.

- Os parâmetros do RSI e as percentagens de stop loss/take profit podem ser ajustados e otimizados através de inputs externos.

Riscos da Estratégia

- O indicador RSI possui algum atraso, podendo perder pontos de reversão de tendência de curto prazo.

- Linhas de stop loss/take profit excessivamente próximas podem ser rompidas, resultando no fecho prematuro da posição.

Direções de Otimização

- Testar o indicador RSI em diferentes períodos para avaliar sua eficácia.

- Testar diferentes combinações de parâmetros para encontrar as percentagens ideais de stop loss e take profit.

- Adicionar indicadores auxiliares para filtrar sinais.

Resumo

Em resumo, esta estratégia é uma abordagem quantitativa que utiliza o indicador RSI para seguir tendências, acompanhada de stop loss e take profit flutuantes. Comparada com estratégias baseadas em um único indicador, esta estratégia gerencia melhor o risco, permitindo travar lucros de forma eficaz. O desempenho pode ser melhorado através da otimização de parâmetros e da adição de indicadores auxiliares.

- 1