Estratégia de Envelope Dinâmico de Média Móvel

Visão Geral

Esta estratégia baseia-se em médias móveis e envelopes dinâmicos, implementando negociações bidirecionais (compra e venda). Ela monitora o preço ultrapassando os envelopes superior e inferior para abrir posições e fecha todas as posições quando o preço cai novamente abaixo da média base. A estratégia é adequada para ações e moedas digitais com tendências mais evidentes.

Princípio da Estratégia

Primeiro, a estratégia calcula a média base com base no tipo e comprimento da média móvel selecionados pelo usuário. Médias comuns incluem SMA, EMA, etc.

Em seguida, com base no parâmetro percentual definido pelo usuário, são calculados os envelopes superior e inferior. Por exemplo, 5% significa que quando a flutuação de preço ultrapassa 105% do intervalo permitido, é acionada a abertura de posição. O número de envelopes pode ser personalizado.

Quanto às regras de entrada, se o preço romper o envelope inferior, compra-se; se romper o envelope superior, vende-se. As regras são muito simples e claras.

Finalmente, quando o preço cai novamente abaixo da média base, todas as posições são fechadas. Este é um ponto de saída para seguir a tendência.

É importante notar que a estratégia implementa a abertura de posições com divisão de lotes. Se houver múltiplos envelopes, os recursos serão alocados proporcionalmente. Isso evita o risco de apostar em uma única direção.

Análise de Vantagens

As principais vantagens desta estratégia são:

- Implementa o acompanhamento automático de tendências. O uso de médias móveis para determinar a direção da tendência é muito comum, sendo um método eficaz.

- O uso de envelopes filtra parte do ruído, evitando negociações desnecessárias por sensibilidade excessiva. Uma configuração razoável de parâmetros pode otimizar significativamente a lucratividade da estratégia.

- A abertura de posições com divisão de lotes aumenta a resiliência da estratégia. Mesmo que uma ruptura unilateral falhe, outras direções podem continuar funcionando bem. Isso otimiza a relação risco-retorno geral.

- Permite personalizar a média móvel e a quantidade de envelopes. Isso aumenta a flexibilidade da estratégia, permitindo que o usuário otimize os parâmetros para diferentes ativos.

Análise de Riscos

Os principais riscos da estratégia são:

- O sistema de médias móveis não é sensível a sinais de cruzamento dourado (golden cross). Se não houver uma tendência clara, a estratégia pode perder algumas oportunidades.

- Envelopes muito largos podem aumentar o número de negociações e o risco de slippage. Envelopes muito estreitos podem perder movimentos grandes. Encontrar um ponto de equilíbrio requer testes suficientes.

- Em mercados laterais, a estratégia pode sofrer mais posições presas. Portanto, ativos com tendências claras são mais adequados.

- A abertura com divisão de lotes limita o lucro por operação. Se o objetivo for buscar apenas o risco unilateral, otimizações adicionais são necessárias.

Direções de Otimização

A estratégia pode ser otimizada principalmente nas seguintes direções:

- Substituir as médias por outros indicadores para definir entrada e saída, como o KDJ, ou combinar múltiplos indicadores para criar filtros.

- Adicionar lógicas de stop-loss e take-profit, para travar parte dos lucros e evitar riscos ativamente.

- Otimizar parâmetros para encontrar a melhor combinação de média móvel e envelope. Isso requer backtesting e otimização completos para encontrar o par de parâmetros ideal.

- Incorporar técnicas como aprendizado profundo para otimização inteligente de parâmetros, aprendendo e atualizando parâmetros progressivamente.

- Considerar as diferenças entre ativos e mercados, definindo múltiplos conjuntos de parâmetros para se adaptar a diferentes ambientes de negociação. Isso aumentará significativamente a estabilidade da estratégia.

Resumo

De modo geral, esta estratégia de envelopes dinâmicos com média móvel é muito adequada para negociação de tendências. Ela é simples, eficiente, fácil de entender e otimizar. Como estratégia básica, sua modelabilidade e extensibilidade são muito fortes. Ao integrá-la com sistemas mais complexos, é possível otimizar ainda mais os indicadores de retorno total e risco ajustado. Portanto, pode servir como uma excelente base para negociação quantitativa.

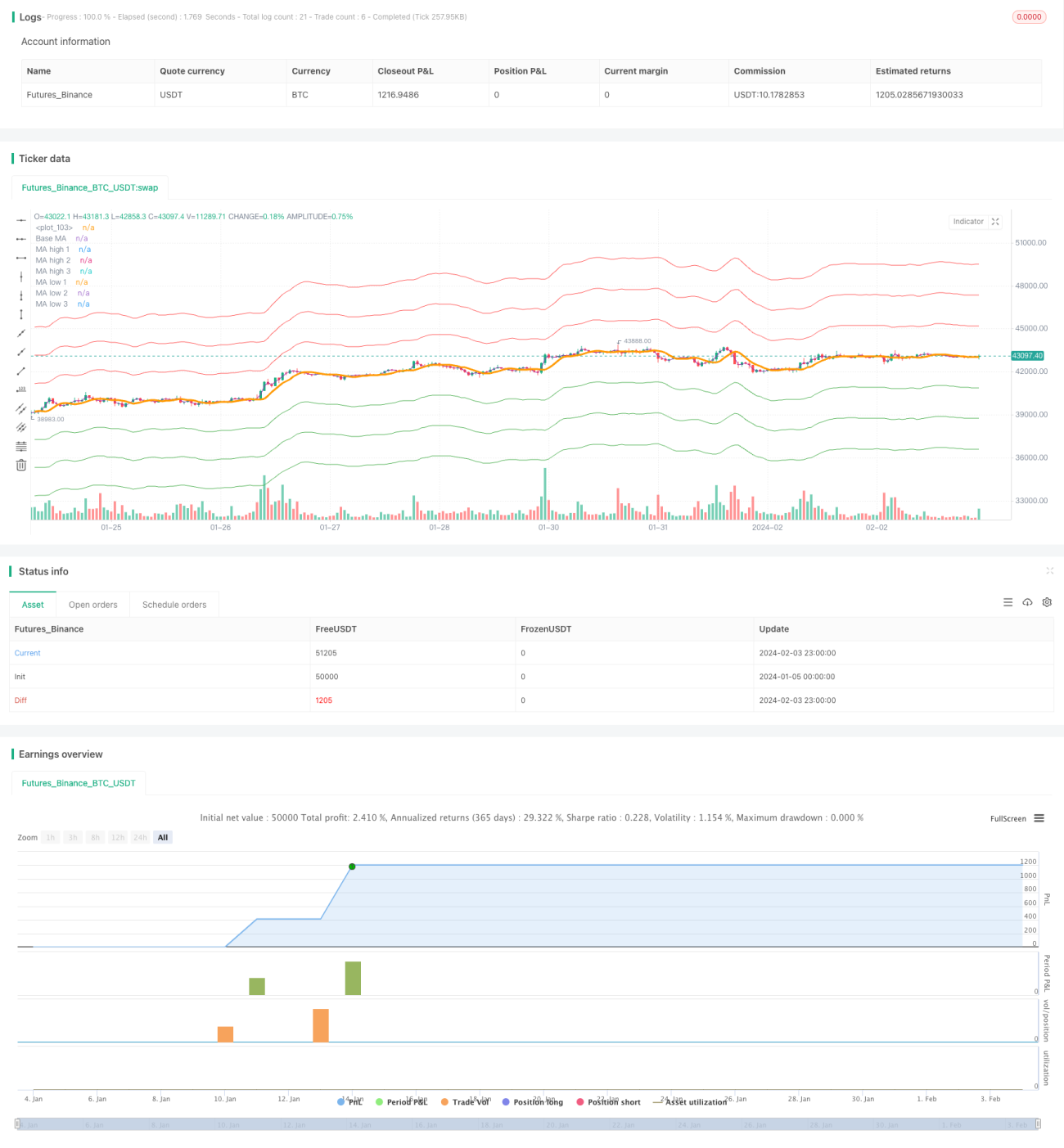

/*backtest

start: 2024-01-05 00:00:00

end: 2024-02-04 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Envelope Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100, initial_capital=1000, pyramiding = 5, commission_type=strategy.commission.percent, commission_value=0.0)

// CopyRight Crypto Robot- 1