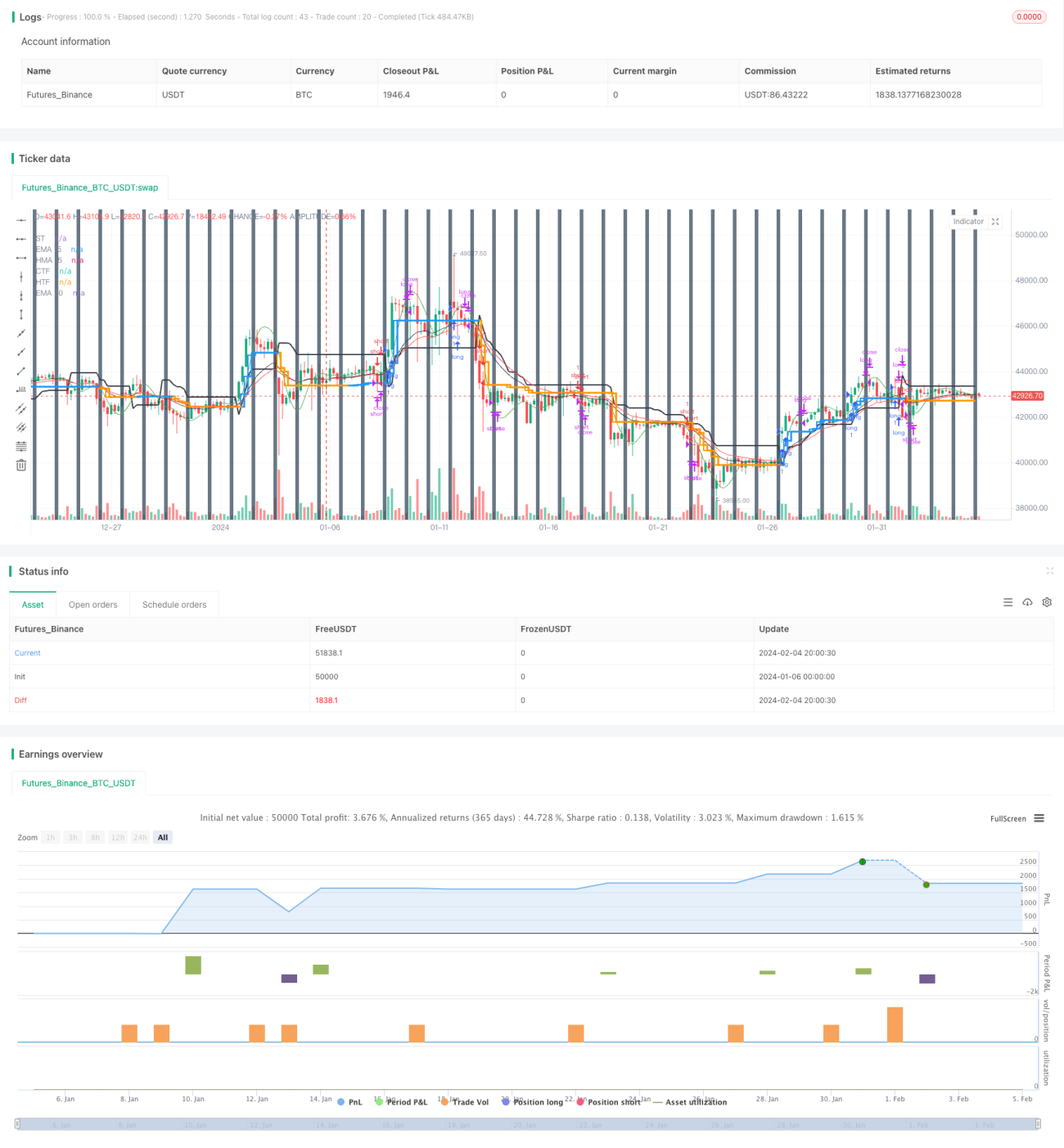

Estratégia de trailing stop baseada no Super Trend de Heikin Ashi

Visão Geral da Estratégia

Esta estratégia é uma estratégia de trailing stop loss de acompanhamento de tendência que combina velas Heikin Ashi e o indicador Super Trend. Ela utiliza as velas Heikin Ashi para filtrar o ruído do mercado, o indicador Super Trend para determinar a direção da tendência e o Super Trend como linha de stop loss dinâmico, alcançando um acompanhamento de tendência eficiente e controle de risco.

Princípio da Estratégia

- Calcular as velas Heikin Ashi: incluindo preço de abertura, fechamento, máxima e mínima.

- Calcular o indicador Super Trend: calcular a banda superior e inferior com base no ATR e no preço.

- Combinar as velas Heikin Ashi e o Super Trend para determinar a direção da tendência.

- Quando o preço de fechamento da Heikin Ashi está mais próximo da banda superior do Super Trend em relação ao fechamento da vela anterior, é uma tendência de alta; quando o fechamento está mais próximo da banda inferior, é uma tendência de baixa.

- Em tendência de alta, usar a banda superior do Super Trend como linha de trailing stop loss; em tendência de baixa, usar a banda inferior do Super Trend como linha de trailing stop loss.

Vantagens da Estratégia

- Utilizar Heikin Ashi para filtrar falsos rompimentos, identificando sinais de tendência de forma mais confiável.

- O Super Trend como stop loss dinâmico maximiza o bloqueio dos lucros da tendência, evitando retrações excessivas.

- Combinar diferentes períodos de tempo para julgar alta/baixa, confirmando sinais de níveis altos/baixos de forma mais confiável.

- A função de fechamento programado evita a influência de movimentos irracionais do mercado em horários específicos.

Riscos da Estratégia

- É fácil sofrer stop loss em reversões de tendência. É possível relaxar um pouco a linha de stop loss para reduzir esse risco.

- Parâmetros inadequados do Super Trend podem resultar em stop loss muito amplo ou muito estreito. É possível testar diferentes combinações de parâmetros.

- Não considera questões de gestão de capital. Deve-se definir controle de posição.

- Não considera custos de transação. Deve-se calcular o impacto dos custos.

Direções de Otimização da Estratégia

- Otimizar a combinação de parâmetros do Super Trend para encontrar os parâmetros ideais.

- Adicionar funcionalidade de controle de posição.

- Incluir considerações de custos, como taxas, slippage, etc.

- Ajustar flexivelmente a amplitude do stop loss conforme a força da tendência.

- Considerar combinar outros indicadores para filtrar sinais de entrada.

Resumo

Esta estratégia integra as vantagens dos indicadores Heikin Ashi e Super Trend, sendo capaz de capturar a direção da tendência, ao mesmo tempo que utiliza o Super Trend para realizar um trailing stop loss dinâmico automatizado, bloqueando assim os lucros da tendência. Os principais riscos da estratégia vêm das reversões de tendência e da otimização de parâmetros, ambos passíveis de melhoria através de otimização adicional. Em geral, a estratégia utiliza a integração de indicadores para aumentar a estabilidade do sistema de negociação e o potencial de lucro.

- 1