Estratégia Ichimoku Cloud Nine para Negociação

Visão Geral

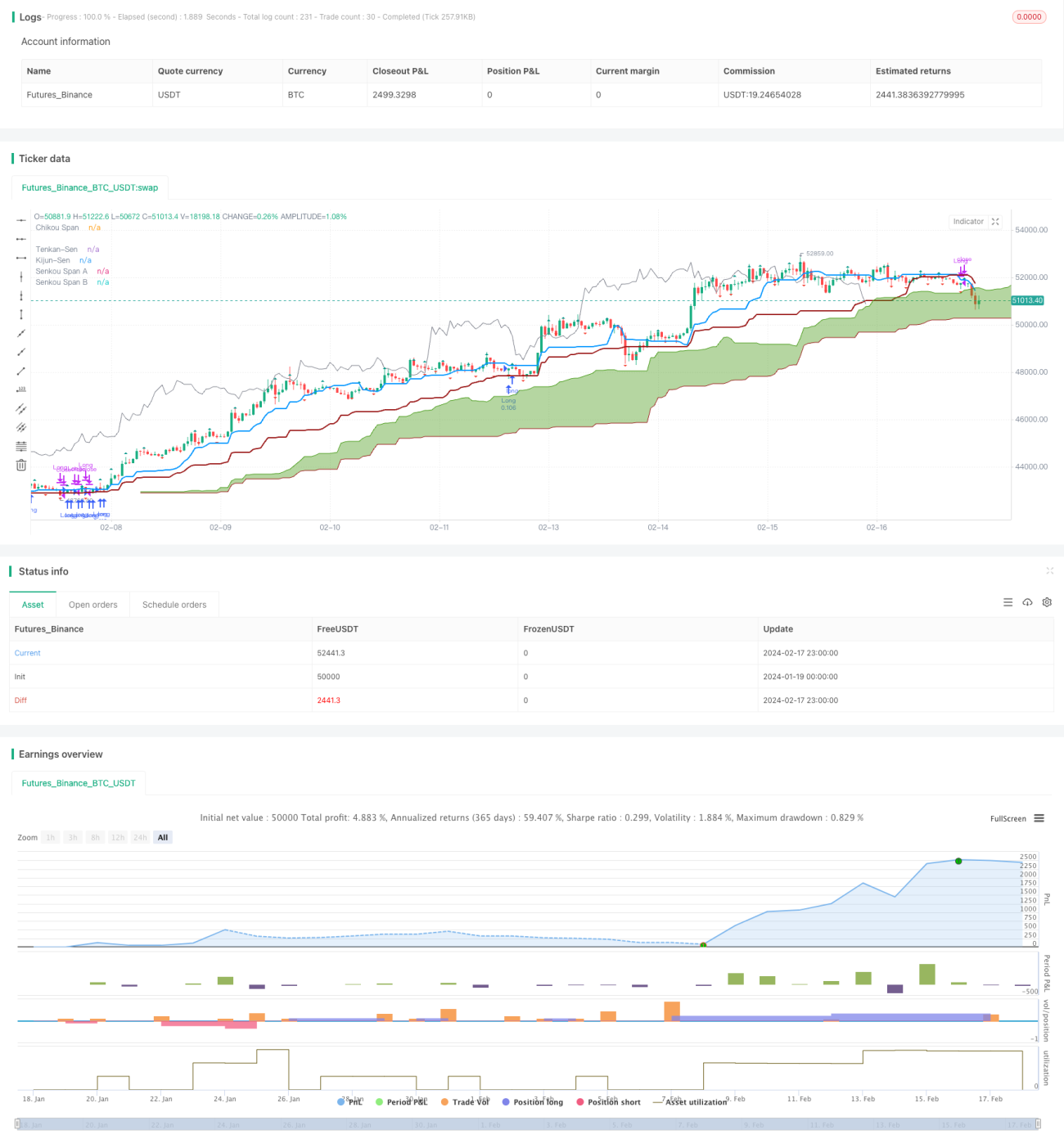

A Estratégia Ichimoku Cloud Nine é uma estratégia de negociação baseada no indicador Ichimoku Cloud combinado com fractais de Williams. Ela utiliza múltiplos sinais de negociação fornecidos pelo indicador Ichimoku Cloud para gerar sinais de negociação. Trata-se de uma estratégia orientada para a negociação real.

Princípio da Estratégia

A estratégia baseia-se principalmente nos seguintes sinais do Ichimoku para entrada:

- Rompimento da Nuvem: sinal gerado quando o preço de fechamento rompe a borda superior ou inferior da nuvem.

- Cruzamento TK: sinal gerado quando a Linha de Virada (Tenkan) cruza a Linha Base (Kijun).

- Torção da Nuvem: sinal gerado quando a linha Senkou Span A cruza a linha Senkou Span B.

- Cruzamento de Borda: sinal gerado quando o preço passa de um lado da nuvem para o outro.

Além disso, a estratégia fecha posições nas seguintes situações:

- Fechamento quando o preço de fechamento entra na nuvem.

- Fechamento quando ocorre um cruzamento reverso TK.

- Fechamento parcial quando um fractal de Williams é rompido.

A estratégia combina múltiplos sinais do gráfico Ichimoku Cloud, visando aumentar a confiabilidade dos sinais de negociação, enquanto utiliza fractais para definir stops e controlar riscos.

Vantagens da Estratégia

Em comparação com estratégias de sinal único, esta estratégia utiliza de forma abrangente múltiplos sinais do gráfico Ichimoku Cloud, podendo filtrar alguns sinais desalinhados e aumentar a precisão dos sinais. Além disso, os parâmetros da estratégia podem ser configurados de forma flexível, sendo adequados para diferentes ativos e otimizações de parâmetros.

Adicionalmente, a introdução do rompimento do fractal de Williams para definir stops permite um controle de risco mais ativo, travando lucros e evitando perdas elevadas.

Riscos da Estratégia

A estratégia enfrenta principalmente os seguintes riscos:

- O indicador Ichimoku Cloud possui defasagem, não refletindo prontamente as mudanças de preço.

- Múltiplos sinais podem ser excessivamente conservadores, perdendo algumas oportunidades.

- O stop baseado em fractal pode ser rompido, causando perdas.

Quanto ao problema da defasagem, pode-se ajustar adequadamente os parâmetros ou desativar parte dos filtros de sinal. Quanto ao risco de stop do fractal, pode-se ajustar o período do fractal ou utilizar apenas stops parciais.

Direções de Otimização da Estratégia

A estratégia pode ser otimizada principalmente nos seguintes aspectos:

- Ajustar os parâmetros do Ichimoku para se adequar a diferentes períodos e ativos.

- Ajustar ou desativar parte dos sinais de filtro, mantendo os sinais principais.

- Ajustar os parâmetros do fractal, utilizando fractais de períodos maiores ou adotando apenas stops parciais.

- Adicionar outros filtros de indicadores, como indicadores de volume, etc.

Resumo

A Estratégia Ichimoku Cloud Nine, ao integrar múltiplos sinais do gráfico Ichimoku Cloud, potencializa as vantagens do indicador Cloud, ao mesmo tempo que aumenta a precisão e a taxa de acerto dos sinais. A estratégia também utiliza fractais como método de stop para controlar o risco. Pode ser adaptada a múltiplos ativos em negociação algorítmica por meio de otimizações de parâmetros e sinais.

/*backtest

start: 2024-01-19 00:00:00

end: 2024-02-18 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Ichimoku Cloud Nine", shorttitle="Ichimoku Cloud Nine", overlay=true, calc_on_every_tick = true, calc_on_order_fills = false, initial_capital = 5000, currency = "USD", default_qty_type = "percent_of_equity", default_qty_value = 10, pyramiding = 3, process_orders_on_close = true)

color green = #459915- 1