Стратегия трейлинг-стопа на основе разворота тренда

Обзор

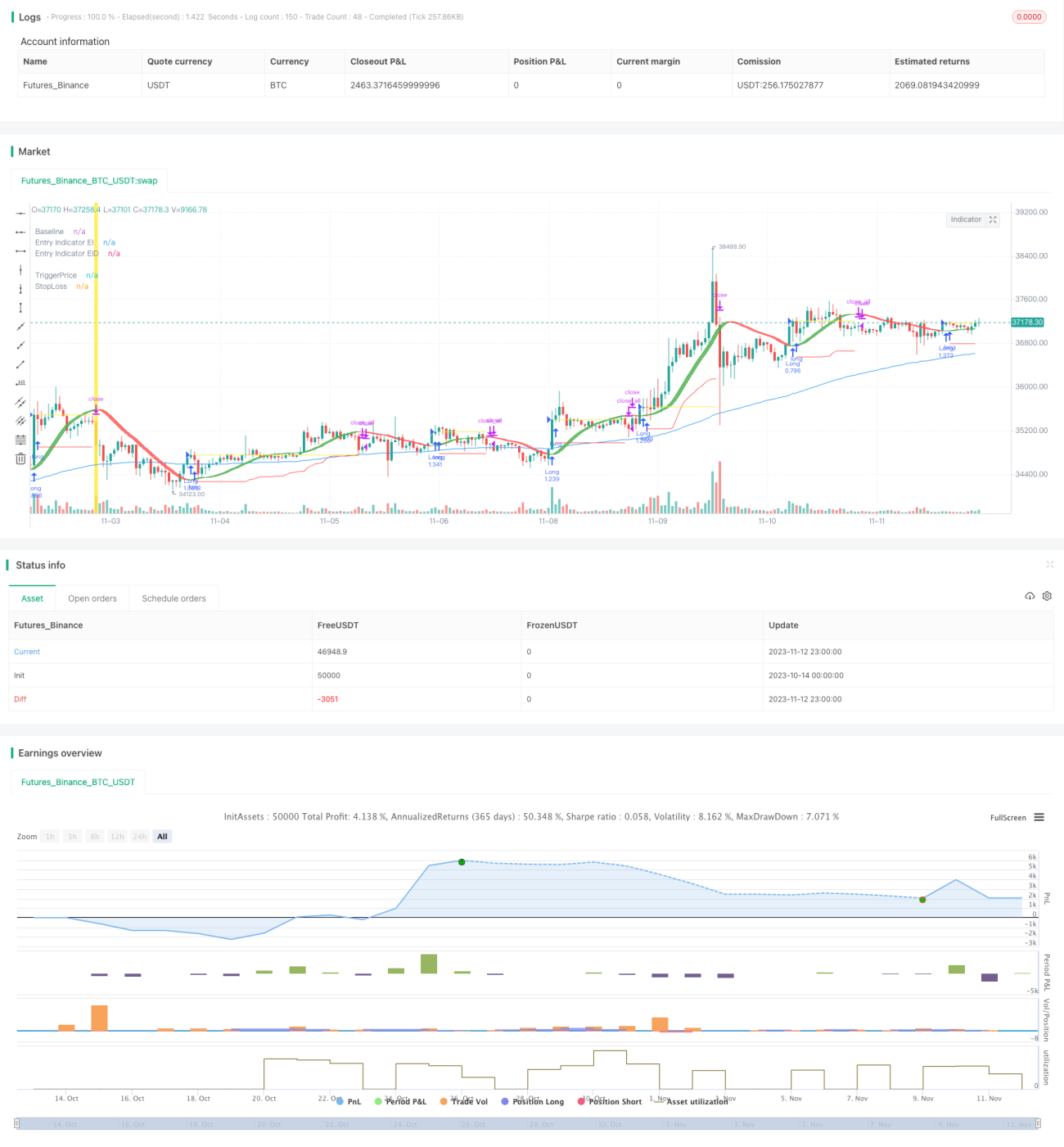

Данная стратегия основана на индикаторах разворота тренда и сочетает механизм трейлинг-стопа для отслеживания тренда на трендовых рынках и сокращения убытков на боковых рынках.

Принцип стратегии

В стратегии используется скользящая средняя Халла (Hull Moving Average) в качестве основного индикатора для определения тренда. Когда цена пересекает скользящую среднюю Халла снизу вверх, открывается длинная позиция; когда цена пересекает её сверху вниз, открывается короткая позиция. Одновременно для подтверждения тренда применяется скользящая средняя Макгинли (McGinley Moving Average).

После открытия позиции, если цена разворачивается, то есть при пересечении линий скользящей средней Халла, выполняется логика смены тренда и закрывается текущая позиция.

Стратегия также включает механизм трейлинг-стопа. После открытия позиции динамический уровень стопа рассчитывается на основе ATR. По мере движения цены линия стопа также корректируется динамически, обеспечивая трейлинг-стоп по прибыли.

Преимущества стратегии

- Использование скользящей средней Халла для определения точек разворота тренда – она обладает высокой чувствительностью к сигналам пробоя.

- Сочетание со скользящей средней Макгинли для подтверждения тренда позволяет отсеять часть ложных пробоев.

- Применение динамического трейлинг-стопа, который адаптируется к волатильности рынка, эффективно контролирует убытки.

- Своевременная реакция на разворот тренда при пересечении скользящей средней Халла предотвращает дальнейшее увеличение убытков.

- Возможность легко переключаться между различными комбинациями параметров для тестирования и поиска оптимальных значений.

Риски и решения

-

На боковом рынке может срабатывать стоп-лосс.

- Можно увеличить дистанцию стопа, добавив буферную зону.

-

При сильном движении цены трейлинг-стоп может не успевать за ней.

- Следует уменьшить период сглаживания, чтобы стоп быстрее следовал за ценой.

-

Ложные пробои могут приводить к ненужным убыткам.

- Добавить другие индикаторы для подтверждения сигнала, чтобы избежать ложных пробоев.

-

Неподходящие параметры могут ухудшить результаты стратегии.

- Провести бэктестинг на разных рыночных циклах для поиска оптимальных параметров.

Идеи по оптимизации

- Добавить другие индикаторы для подтверждения, например паттерны свечей, полосы Боллинджера, RSI и т.д., чтобы повысить качество сигналов.

- Оптимизировать параметры для разных инструментов и таймфреймов, найти наилучшую комбинацию.

- Рассмотреть возможность применения методов машинного обучения для адаптивной оптимизации параметров.

- Улучшить алгоритм стопа, чтобы минимизировать ненужные срабатывания при сохранении защиты.

- Объединить с управлением капиталом для оптимизации стратегии управления позициями.

- Рассмотреть добавление автоматического механизма фиксации прибыли.

Заключение

В целом данная стратегия представляет собой достаточно надёжный трендовый следящий подход. В отличие от фиксированного стопа, она использует динамический механизм, который адаптирует уровень стопа к рыночной волатильности, эффективно снижая вероятность срабатывания стопа. Введение скользящей средней Халла и логики смены тренда позволяет быстро реагировать на развороты тренда. Однако стратегия несёт определённые риски, такие как срабатывание стопа на боковом рынке, риск ложных пробоев и т.д. Дальнейшая оптимизация параметров индикаторов, алгоритма стопа и управления позициями может обеспечить более стабильную работу стратегии на различных рынках.

/*backtest

start: 2023-10-14 00:00:00

end: 2023-11-13 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// © Milleman

//@version=4

strategy("MilleMachine", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital=10000, commission_type=strategy.commission.percent, commission_value=0.06)

- 1