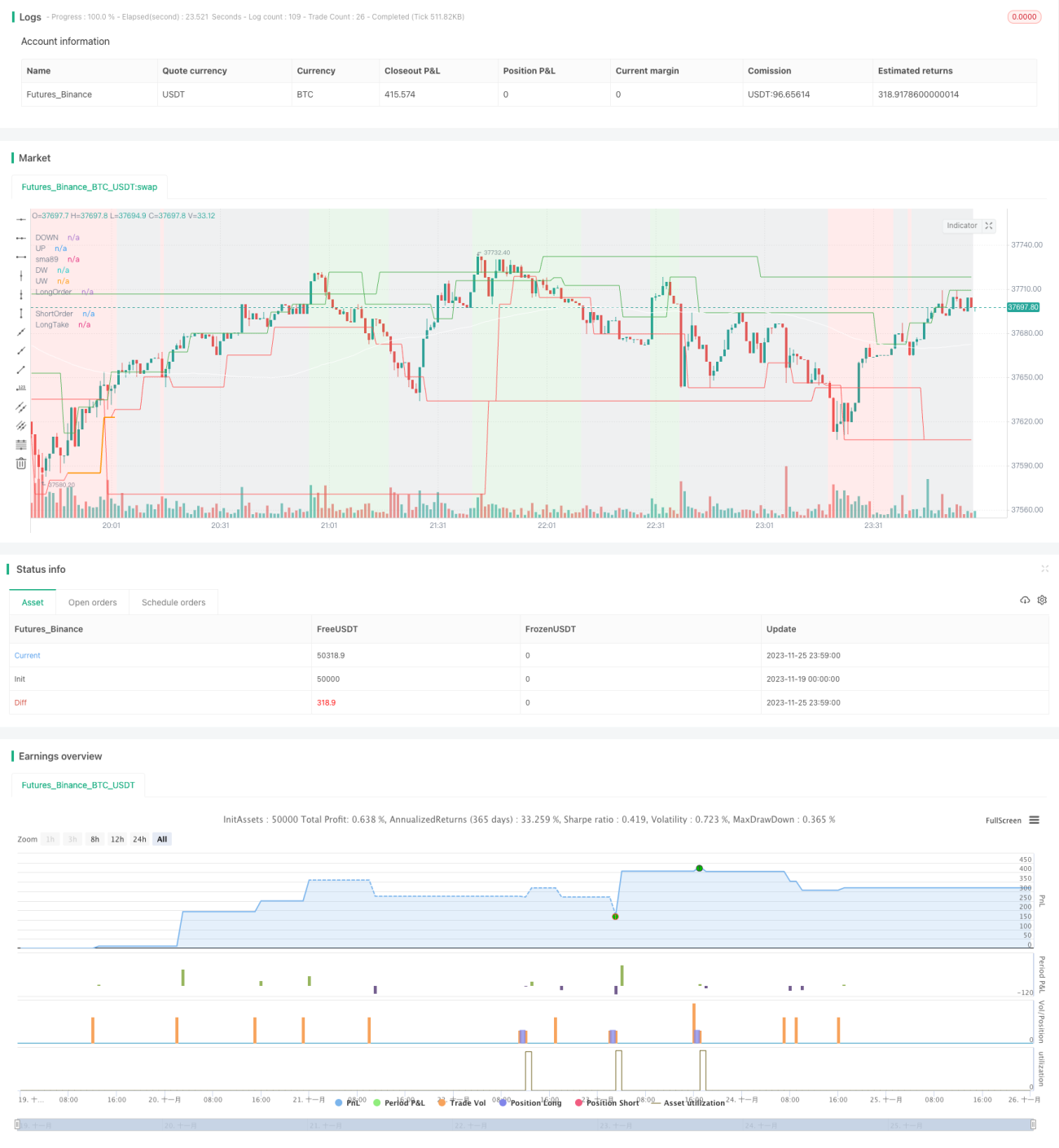

Стратегия высокочастотной количественной торговли на основе двойной фильтрации

Обзор

Данная стратегия называется «Двойная фильтрация в количественной торговле». Она использует мультивременной фреймворк и реализует высокочастотную количественную торговую стратегию, основанную на концепции двойной фильтрации. Стратегия применяет индикаторы на разных таймфреймах для принятия решений, что позволяет более строго отфильтровывать торговые сигналы, отсеивая большое количество ложных сигналов и тем самым добиваясь более высокой вероятности успеха.

Принцип стратегии

Основной принцип стратегии заключается в следующем:

-

Использование недельных и дневных графиков для определения направления рыночного тренда в качестве фильтра направления стратегии. Торговля разрешена только при соответствии условиям тренда.

-

На 4-часовом таймфрейме строится канал для определения точек продажи и покупки, генерирующий торговые сигналы.

-

Согласованность направления, определённого на недельных и дневных графиках, с направлением на 4-часовом графике позволяет отсеять большое количество ложных сигналов, повышая надёжность торговых сигналов.

-

Использование уровней коррекции Фибоначчи для установки уровней тейк-профита и стоп-лосса, что обеспечивает быструю фиксацию прибыли и остановку убытков.

В частности, стратегия сначала определяет приоритетное направление тренда на недельных и дневных графиках. Принцип определения приоритетного направления: если цена закрытия текущей свечи находится на стороне с большим углом отставания от линии периода, то это направление и считается направлением данной линии периода. Затем на 4-часовом уровне строится канал A B C D, по которому через направление канала и точки разворота определяются точки покупки и продажи, генерируя торговые сигналы. Наконец, обязательно требуется, чтобы приоритетное направление, определённое на текущей линии периода, совпадало с направлением торгового сигнала на 4-часовом графике. Это позволяет отфильтровать множество ложных сигналов, тем самым повышая надёжность торговых сигналов.

Преимущества стратегии

Данная стратегия обладает следующими основными преимуществами:

-

Механизм двойной фильтрации сигналов на основе нескольких таймфреймов позволяет отсеять значительный шум и получить высоконадёжные торговые возможности.

-

Использование каналов для определения точек покупки и продажи даёт чёткие торговые сигналы.

-

Установка уровней тейк-профита и стоп-лосса на уровнях коррекции Фибоначчи позволяет быстро фиксировать прибыль и останавливать убытки.

-

Стратегия имеет небольшое количество параметров, что облегчает её понимание и освоение.

-

Обладает хорошей расширяемостью, легко поддаётся оптимизации и улучшению.

Риски стратегии

Основные риски данной стратегии следующие:

-

Мониторинг слишком большого количества таймфреймов увеличивает сложность и повышает вероятность ошибок.

-

Не учитываются особые ситуации на рынке, такие как резкие колебания, вызванные важными новостными событиями.

-

Установка уровней тейк-профита и стоп-лосса на точках разворота может привести к недостаточной прибыли.

-

Неправильная настройка параметров может привести к чрезмерной торговле или пропуску сделок.

Меры противодействия:

-

Усилить мониторинг нештатных ситуаций и значимых новостных событий.

-

Оптимизировать логику тейк-профита и стоп-лосса, чтобы обеспечить определённый уровень прибыли.

-

Провести детальное тестирование и оптимизацию параметров, чтобы снизить вероятность чрезмерной торговли и пропуска сделок.

Направления оптимизации стратегии

Основные направления оптимизации стратегии:

-

Добавить модели машинного обучения для определения приоритетного направления тренда, используя больше данных для повышения точности определения.

-

Протестировать другие индикаторы для построения каналов и определения точек покупки/продажи.

-

Попробовать более продвинутые методы тейк-профита и стоп-лосса, такие как скользящий тейк-профит, прыжковый тейк-профит и т.д.

-

Использовать результаты бэктестинга для вывода оптимальных параметров, чтобы настройка параметров больше соответствовала принципам количественного инвестирования.

-

Добавить механизмы мониторинга и реагирования на серьёзные неожиданные события.

Заключение

В целом, основная идея данной стратегии — высокочастотная количественная торговая стратегия, основанная на двойной фильтрации для снижения шума. Она использует оценку на нескольких таймфреймах и метод определения точек покупки/продажи через каналы, что обеспечивает двойную надёжную фильтрацию торговых сигналов. Кроме того, стратегия имеет небольшое количество параметров и легко осваивается; она обладает хорошей расширяемостью и легко поддаётся оптимизации. На следующем этапе планируется оптимизировать точность определения, методы тейк-профита/стоп-лосса, параметры и другие аспекты, чтобы сделать стратегию более эффективной.

- 1