Количественная стратегия на основе скорости изменения цены и скользящей средней

Обзор

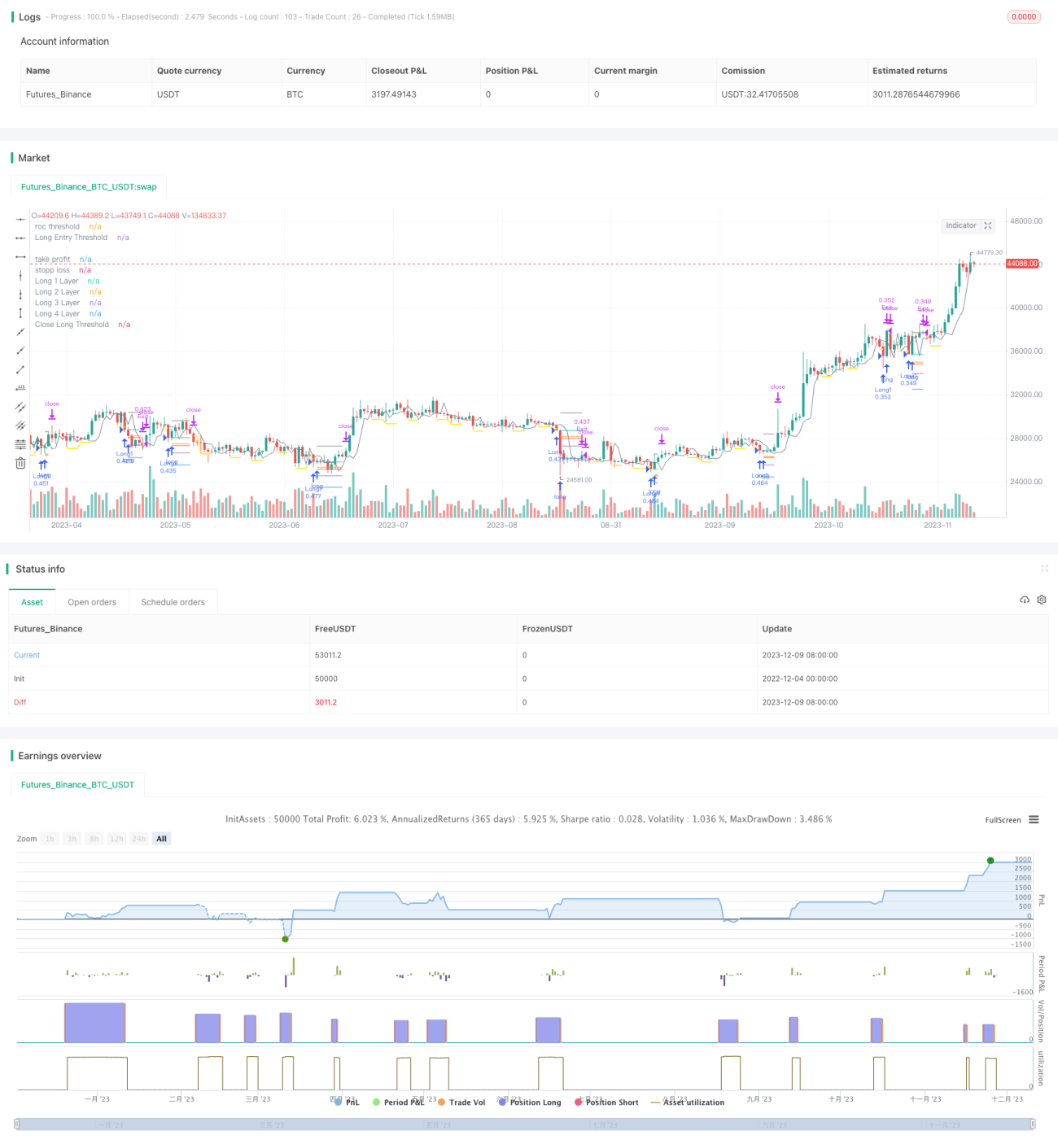

Данная стратегия сочетает в себе технические индикаторы темпа изменения цены (ROC) и скользящие средние, что позволяет точно определять точки входа и выхода. Когда цена демонстрирует значительное снижение, устанавливается порог покупки, и при дальнейшем падении открывается длинная позиция; при росте цены устанавливается порог продажи, и при продолжении роста позиция закрывается. Кроме того, стратегия использует метод добавления позиций, разделяя покупки на несколько этапов для снижения средней цены входа.

Принцип стратегии

Логика покупки

- Рассчитывается темп изменения цены (ROC) и устанавливается линия порога покупки.

- Когда цена пробивает линию порога покупки, фиксируется эта точка и активируется ограничительная линия покупки.

- Ограничительная линия покупки действует в течение заданного параметрами времени, после чего отключается.

- Если цена продолжает снижаться и пробивает ограничительную линию покупки, открывается первая длинная позиция.

Логика продажи

- Рассчитывается темп изменения цены (ROC) и устанавливается линия порога продажи.

- Когда цена пробивает линию порога продажи вверх, фиксируется эта точка и активируется ограничительная линия продажи.

- Ограничительная линия продажи действует в течение заданного параметрами времени, после чего отключается.

- Если цена продолжает расти и пробивает ограничительную линию продажи, все длинные позиции закрываются.

Управление рисками

Стратегия включает встроенные функции стоп-лосса и тейк-профита с настраиваемыми параметрами для контроля рисков по открытым позициям в реальном времени.

Метод добавления позиций

При открытии каждой новой позиции последующая цена покупки устанавливается с заданным процентом от предыдущей, что позволяет добавлять позиции частями и усреднять цену входа.

Преимущества анализа

- Использование индикатора ROC для поиска точек входа/выхода: ROC очень чувствителен к изменениям цены, что обеспечивает точное определение точек.

- Применение ограничительных линий для дополнительного подтверждения моментов входа/выхода, что позволяет избежать ложных пробоев.

- Метод добавления позиций позволяет отслеживать рыночную стоимость при сохранении контролируемого риска.

- Встроенные стоп-лосс и тейк-профит строго контролируют риск по каждой отдельной позиции.

Риски и решения

- При резких колебаниях рынка стратегия может открыть слишком много позиций. Решение: разумно настроить параметры добавления позиций и ограничить общее количество позиций.

- При неопределённом боковом тренде цены могут часто срабатывать стоп-лосс или тейк-профит. Решение: можно расширить диапазоны стоп-лосса и тейк-профита или временно отключить эту функцию.

Рекомендации по оптимизации

- Комбинировать с другими индикаторами для фильтрации моментов входа. Например, использовать скользящие средние: учитывать сигналы ROC только тогда, когда цена находится ниже скользящей средней.

- Оптимизировать логику добавления позиций: запускать добавление только при выполнении определённых условий, например, только если цена снова снизилась на определённую величину.

- Параметры для разных инструментов могут сильно различаться, поэтому требуется тщательное бэктестирование и симуляция на реальных данных для поиска оптимального набора параметров.

- Можно настроить адаптивные стоп-лосс и тейк-профит, которые изменяются в зависимости от волатильности рынка.

Заключение

Данная стратегия комплексно использует индикатор ROC для точного определения точек входа и выхода, ограничительные линии для фильтрации сигналов, встроенные стоп-лосс и тейк-профит для управления рисками, а также метод добавления позиций для увеличения прибыли. При условии разумной настройки параметров стратегия способна получать сверхдоходность при сохранении контролируемого уровня риска. В будущем можно дополнительно оптимизировать фильтрацию сигналов и механизмы управления рисками, чтобы сделать стратегию применимой в большем количестве рыночных условий.

- 1