Стратегия следования за трендом с двойным разворотом

Обзор

Это стратегия следования за трендом, объединяющая двойные сигналы разворота. Она интегрирует стратегию разворота 123 и стратегию индекса производительности для отслеживания точек разворота цен, обеспечивая более надежное определение тренда.

Принцип стратегии

Стратегия состоит из двух подстратегий:

-

Стратегия разворота 123

Использует 14-дневные свечи для определения сигналов разворота. Правила:

- Сигнал на покупку: цена закрытия за предыдущие два дня снижалась, текущая свеча закрывается выше предыдущей, 9-дневный медленный стохастик (Stochastic Slow) ниже 50.

- Сигнал на продажу: цена закрытия за предыдущие два дня росла, текущая свеча закрывается ниже предыдущей, 9-дневный быстрый стохастик (Stochastic Fast) выше 50.

-

Стратегия индекса производительности

Рассчитывает процентное изменение цены за последние 14 дней в качестве индикатора. Правила:

- Если индекс производительности > 0, генерируется сигнал на покупку.

- Если индекс производительности < 0, генерируется сигнал на продажу.

Итоговый сигнал представляет собой комбинацию обоих сигналов. То есть для фактического совершения сделки требуются однонаправленные сигналы на покупку или продажу.

Это позволяет отфильтровать часть шума и сделать сигналы более надежными.

Преимущества стратегии

Данная двойная система разворота обладает следующими преимуществами:

- Комбинация двух факторов повышает надежность сигналов.

- Эффективно фильтрует рыночный шум, избегая ложных сигналов.

- Паттерн 123 является классическим и практичным, легко определяется и воспроизводится.

- Индекс производительности позволяет оценить будущее направление тренда.

- Гибкая комбинация параметров, возможна дальнейшая оптимизация.

Риски стратегии

Стратегия также сопряжена с определенными рисками:

- Возможен пропуск внезапных разворотов, что не позволяет полностью уловить тренд.

- Комбинация двух условий сокращает количество сигналов, что может снизить доходность.

- Требование однонаправленности сигналов делает стратегию чувствительной к особым колебаниям отдельных активов.

- Неправильная настройка параметров может привести к искажению сигналов.

Рекомендуется рассмотреть следующие направления оптимизации:

- Настройка параметров, таких как длина свечей, период стохастика и т.д.

- Оптимизация логики определения двойных сигналов.

- Включение дополнительных факторов, например, объема торгов.

- Добавление механизма стоп-лосса.

Заключение

Данная стратегия объединяет двойное определение разворота и эффективно выявляет точки смены тренда. Хотя вероятность появления сигналов снижается, их надежность возрастает, что делает стратегию подходящей для среднесрочного и долгосрочного следования за трендом. Эффективность стратегии может быть повышена за счет настройки параметров и добавления множества факторов.

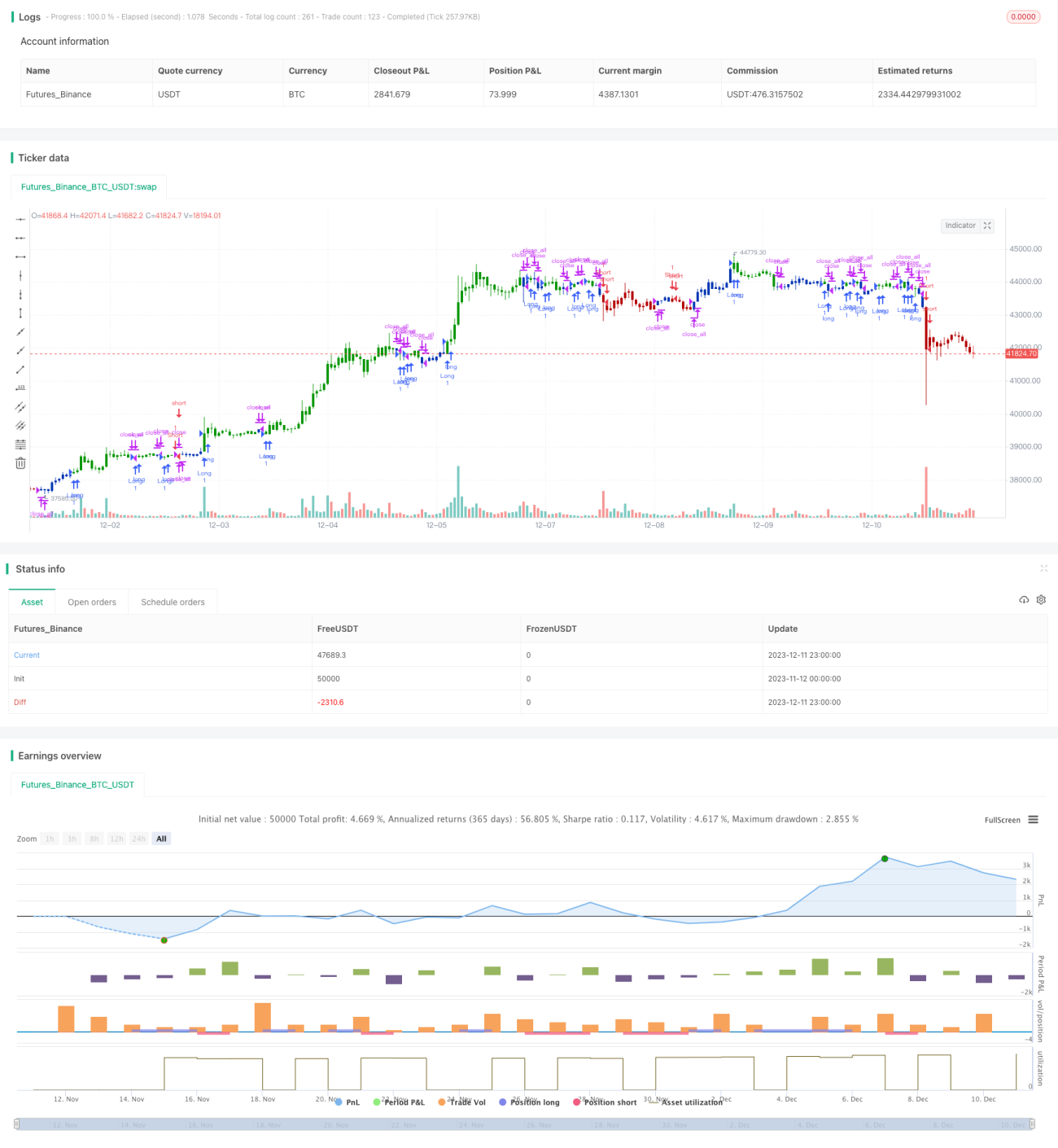

/*backtest

start: 2023-11-12 00:00:00

end: 2023-12-12 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 15/04/2021

// This is combo strategies for get a cumulative signal. - 1