Стратегия динамического усреднения стоимости при регулярном инвестировании с реинвестированием (сложный процент)

Обзор

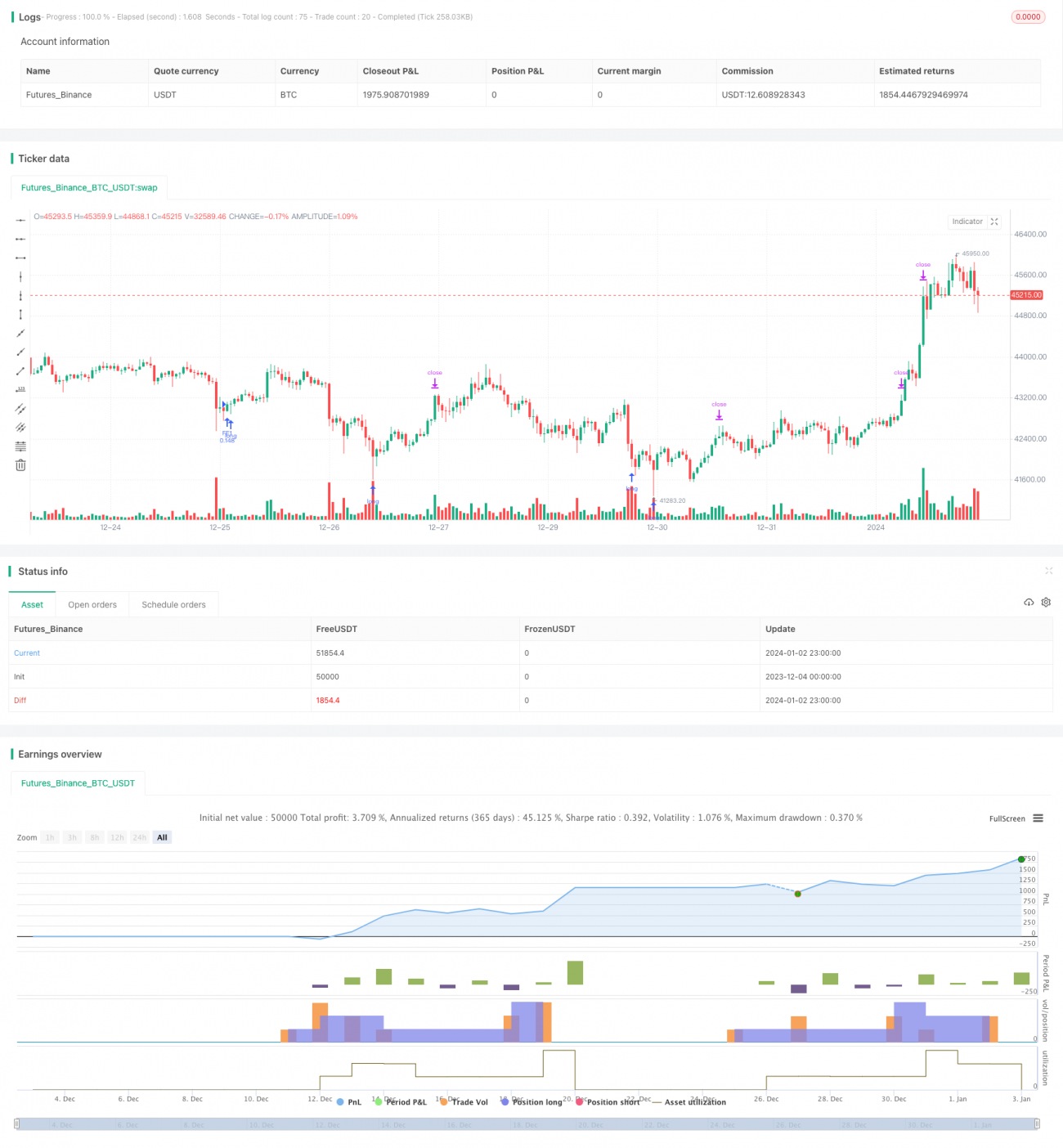

Стратегия динамического усреднения стоимости с реинвестированием (DCA) путем динамической корректировки объема каждой открываемой позиции. На начальном этапе тренда открывается небольшое количество позиций, а по мере увеличения глубины консолидации объем позиций постепенно наращивается. Стратегия использует экспоненциальную функцию для расчета уровней стоп-лосса на каждом уровне и при их пробое открывает новую партию позиций, что позволяет линии средней стоимости удерживания снижаться экспоненциально. С увеличением глубины стоимость позиции может постепенно смещаться вниз, а после разворота цены производится частичная фиксация прибыли для получения большего дохода.

Принцип стратегии

Стратегия использует простой сигнал перепроданности RSI в сочетании с выбором времени по скользящей средней для открытия позиции. Когда RSI опускается ниже уровня перепроданности и цена закрытия меньше скользящей средней, генерируется сигнал на открытие первой позиции. После открытия первой позиции, на основе экспоненциальной функции рассчитывается нижняя граница пробития цены, генерируя сигнал DCA. При каждом DCA объем позиции корректируется так, чтобы каждый лот был равным. Из-за динамического изменения объема и средней стоимости это создает эффект, аналогичный кредитному плечу.

С увеличением числа DCA средняя стоимость позиции постоянно снижается, и для получения прибыли достаточно небольшого отскока. После открытия нескольких последовательных позиций над средней ценой рисуется линия стоп-лосса. Как только цена снова пробивает вверх, превышая среднюю стоимость и линию стоп-лосса, позиция закрывается по стопу.

Главное преимущество стратегии заключается в том, что по мере снижения средней стоимости даже на боковом рынке можно постепенно уменьшать затраты. Когда тренд разворачивается, так как средняя стоимость уже значительно ниже рыночной цены, можно получить большую прибыль.

Риски и недостатки

Основной риск стратегии – ограниченный объем начальной позиции. При непрерывном нисходящем тренде существует риск срабатывания стоп-лосса. Поэтому необходимо установить приемлемый для себя уровень стоп-лосса.

Кроме того, настройка размера стоп-лосса также имеет две крайности. Слишком большой стоп-лосс может не дать получить отскок достаточной глубины, а слишком маленький – увеличить вероятность повторного пробоя цены вверх на средней коррекции. Поэтому очень важно выбрать подходящий размер стоп-лосса в зависимости от рынка и собственной толерантности к риску.

При длительном цикле DCA, когда формируется много уровней, если цена резко вырастет, возникает риск слишком высокой средней стоимости, при которой невозможно зафиксировать убыток. Это также требует разумной настройки количества уровней DCA в соответствии с общим объемом позиции и максимально допустимой средней стоимостью.

Рекомендации по оптимизации

-

Оптимизировать сигналы выбора времени. Можно протестировать различные параметры и комбинации индикаторов для получения сигналов с более высокой вероятностью успеха.

-

Оптимизировать механизм стоп-лосса. Можно протестировать использование стоп-лосса в форме Λ (перевернутой V) или дуги вместо простого трейлинг-стопа, что может дать лучшие результаты. Также можно добавить стратегию коррекции размера стоп-лосса с временным разделением позиции.

-

Оптимизировать способ фиксации прибыли. Можно протестировать различные типы трейлинг-тэйк-профита для поиска лучших точек выхода и повышения общей доходности.

-

Добавить механизм защиты от отскоков. После стоп-лосса может снова возникнуть сигнал DCA и повторное открытие позиции. В этом случае можно добавить защитный диапазон, чтобы избежать немедленного агрессивного открытия после стоп-лосса.

Заключение

Данная стратегия использует индикатор RSI для определения момента покупки и динамическую стратегию DCA со стоп-лоссом, рассчитанным по экспоненциальной функции, что позволяет динамически регулировать объем позиции и ее среднюю стоимость, получая ценовое преимущество на колебательных рынках. Оптимизация в основном направлена на сигналы входа/выхода, способы стоп-лосса и фиксации прибыли. В целом, стратегия использует основную концепцию экспоненциального DCA, что позволяет постоянно снижать среднюю стоимость, получая больше пространства для маневра на боковом рынке и более высокую доходность на трендовом рынке. Однако все равно необходимо выбирать подходящие параметры в соответствии с собственным планом управления капиталом для контроля общего риска позиции.

- 1