Стратегия пересечения двух импульсно-взвешенных скользящих средних

1

Follow

1802

Followers

Обзор

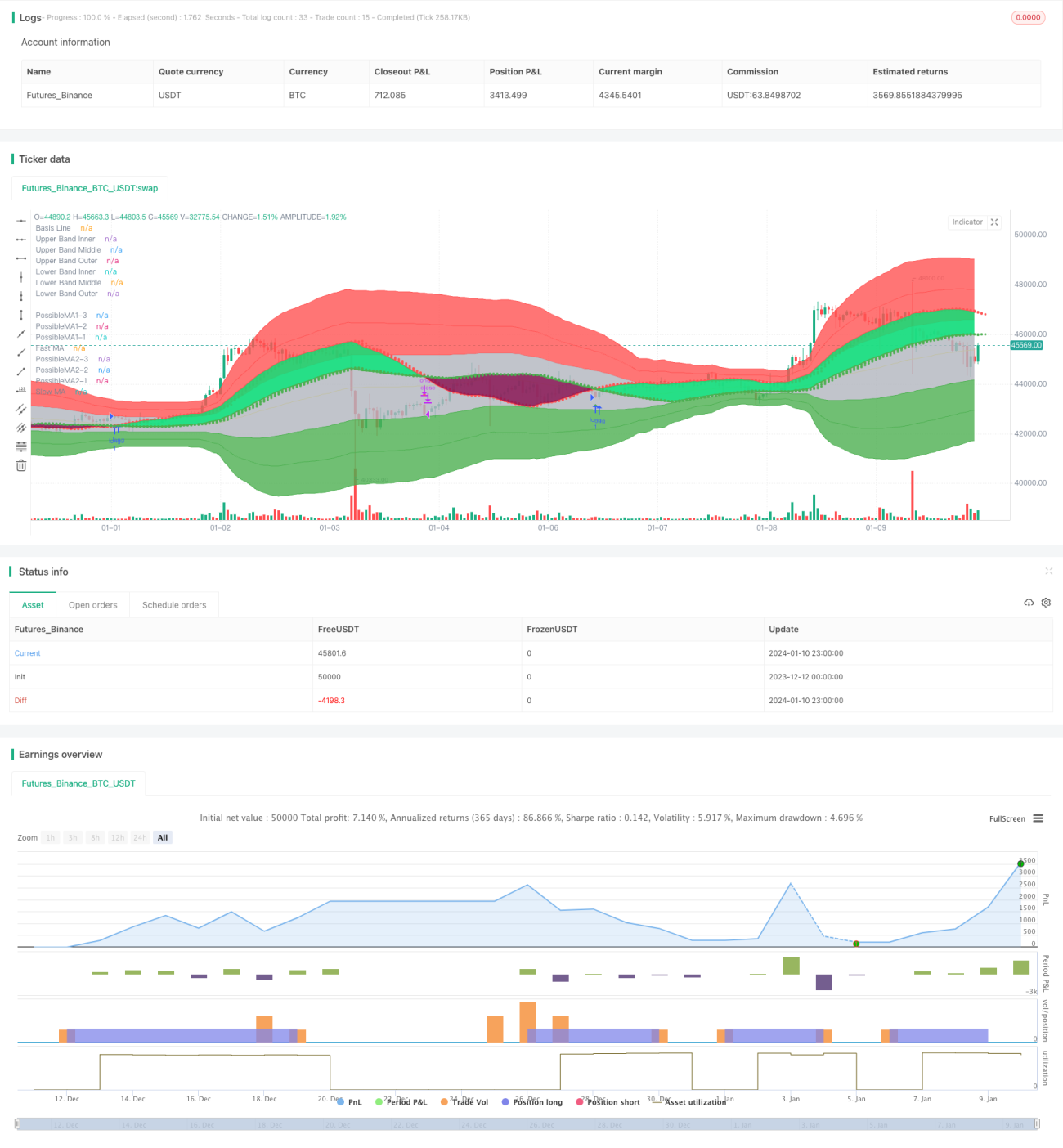

Данная стратегия вычисляет две моментум-взвешенные скользящие средние (MAEMA) с разными периодами и формирует сигналы на покупку и продажу при их пересечении. Короткопериодная линия используется для определения рыночного тренда и краткосрочных разворотов, а долгопериодная – для определения основного направления тренда.

Принцип

- Рассчитываются MAEMA быстрой линии (80 периодов) и медленной линии (144 периода).

- Быстрая линия отражает краткосрочный тренд и точки разворота. Медленная линия показывает основное направление тренда.

- Когда быстрая линия пересекает медленную снизу вверх, генерируется сигнал на покупку. Когда быстрая линия пересекает медленную сверху вниз, генерируется сигнал на продажу.

- Стратегия также отображает три прогнозные точки, указывающие возможные значения следующего периода, что помогает оценить будущее пересечение линий.

- В стратегии в полной мере используются импульсные свойства и прогнозирующая функция самого индикатора MAEMA.

Анализ преимуществ

- MAEMA сама по себе включает импульсный фактор, что позволяет быстрее улавливать изменения тренда.

- Стратегия с двойной скользящей средней определяет направление тренда на разных временных отрезках.

- Сочетание пересечений быстрой и медленной линий с прогнозными точками MAEMA делает сигналы на покупку/продажу более надёжными.

- Полная автоматическая отрисовка наглядно отражает рыночные колебания.

Анализ рисков

- При аномальных рыночных движениях чувствительность MAEMA может быть чрезмерной, что приведёт к ложным сигналам. Можно немного расширить стоп-лосс.

- Система скользящих средних часто даёт ложные сигналы на боковом рынке. Целесообразно добавить дополнительные фильтры.

- Периоды быстрой и медленной линий необходимо оптимизировать для каждого инструмента, чтобы найти наилучшие параметры.

Направления оптимизации

- Оптимизировать периоды быстрой и медленной линий MAEMA для поиска наилучшего сочетания параметров.

- Добавить фильтры, чтобы избежать открытия позиций при флэтовом рынке. Например, использовать DMI, MACD и другие индикаторы для определения тренда.

- На основе результатов бэктестинга постоянно корректировать коэффициент ATR и скользящий стоп-лосс для снижения ложноположительных сигналов и контроля рисков.

Заключение

Данная стратегия использует пересечение двух моментум-взвешенных скользящих средних для определения изменений рыночного тренда. Её основная концепция ясна и проста. Благодаря импульсным и прогнозным свойствам MAEMA, она достаточно эффективно выявляет сигналы разворота. Однако необходимо уделить внимание оптимизации параметров и усилению фильтрации для повышения устойчивости.

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1