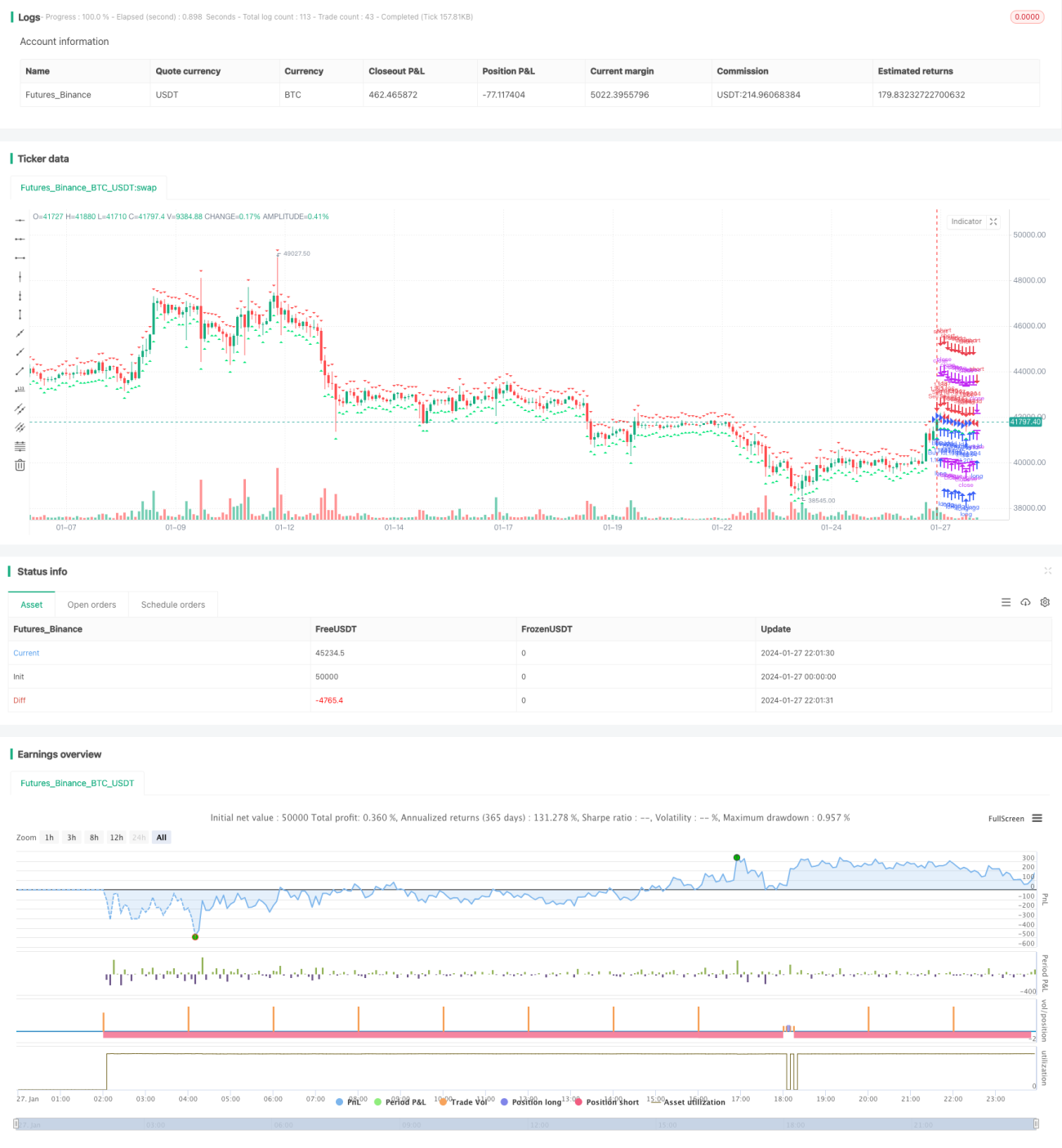

Стратегия направленной торговли PPO Price Sensitive Momentum Double Bottom

Обзор

PPO Price Sensitivity Dynamics Binary-Oriented Trading Strategy - это торговая стратегия, которая использует индикаторы ценной чувствительности для определения тенденций, формирующих двойные дно цены. Она объединяет в себе суждение о формировании двойных дно и суждение о характеристиках движения цены, обеспечивая точное определение точек обратной точки двойного дна цены, что приводит к созданию торгового сигнала.

Стратегический принцип

Эта стратегия использует показатель PPO для определения двойной нижней части цены, а также для определения нижней части цены, чтобы в режиме реального времени отслеживать, является ли показатель PPO нижней частью. Когда показатель PPO имеет двойную нижнюю часть, которая переворачивается вверх и вниз, это указывает на то, что в настоящее время есть возможность купить.

С другой стороны, эта стратегия работает с минимальными значениями цены, чтобы определить, находится ли цена на низком уровне. Когда цена находится на низком уровне, если индикатор PPO имеет нижние признаки, это создает сигнал к покупке.

Двойное определение, подтвержденное оценкой обратной характеристики показателя PPO и ценовым положением, позволяет эффективно идентифицировать возможности для обратного изменения цены, отфильтровывать некоторые ложные сигналы и повышать качество сигналов.

Анализ преимуществ

-

Используя двойную форму PPO, можно точно определить местоположение и время покупки.

-

В сочетании с определением местоположения цены, можно отфильтровать ложные сигналы, создаваемые в более высоких точках, и повысить качество сигнала.

-

Индекс PPO чувствителен, быстро улавливает тенденции изменения цен и подходит для отслеживания тенденций.

-

Применение механизма двойного подтверждения позволяет эффективно снизить риски транзакций.

Риски и решения

-

PPO-индикатор легко дает ложные сигналы, и его необходимо подтвердить другими индикаторами. В качестве вспомогательного инструмента можно использовать индикатор средней линии или индикатор колебаний.

-

Двойной обратный ход не всегда сохраняется, существует риск повторного падения. Можно установить точку остановки, оптимизировать управление позициями.

-

Неправильная настройка параметров может привести к риску утечки или ошибочной покупки. Комбинации параметров требуют повторного тестирования и оптимизации.

-

Большой объем кода позволяет продолжать модулирование и сокращать количество дублируемых кодов.

Направление оптимизации

-

Добавление модуля "стоп-лосс" и оптимизация стратегии управления позициями.

-

Добавление среднелинейного или волатильного индикатора для дополнительной подтверждения.

-

Модулирование кода, уменьшение логики повторного суждения.

-

Продолжайте оптимизировать параметры для повышения стабильности.

-

Попробуйте использовать арбитраж для других сортов.

Подвести итог

Двигательная динамика цены PPO Двухбаковая ориентированная торговая стратегия эффективно ориентируется на ценовые переломы путем захвата двухбаковых характеристик показателя PPO в сочетании с двойным подтверждением определения ценового положения. По сравнению с одиночным показателем, она обладает преимуществами более точного суждения и фильтрации шума. Однако эта стратегия также содержит определенные ложные сигналы риска, требующие дальнейшей оптимизации портфеля показателей, а также строгой стратегии управления позицией, которая может обеспечить стабильную прибыль в реальном мире.

- 1