Стратегия Ichimoku Cloud Nine для торговли

Обзор

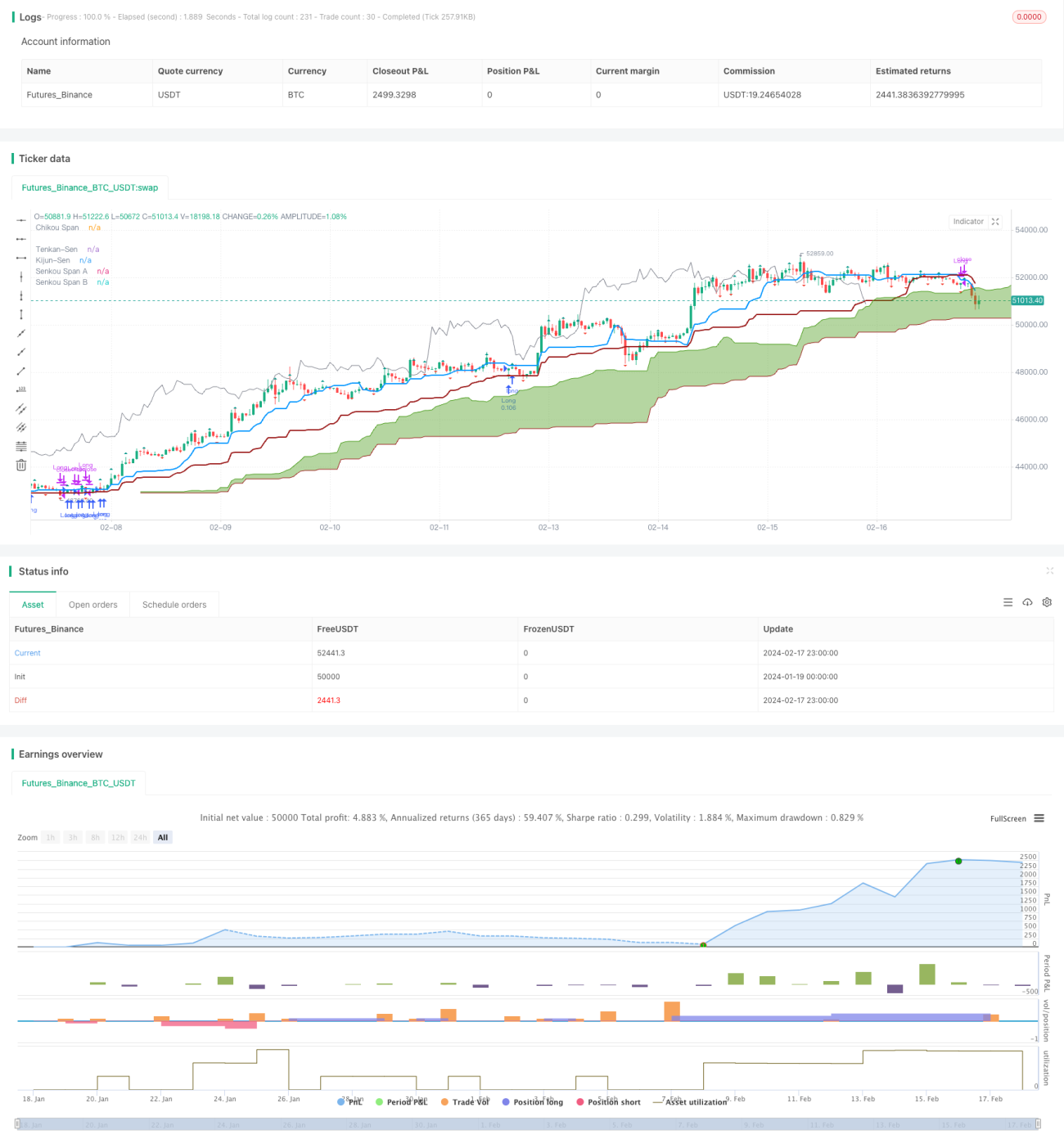

Стратегия Ichimoku Cloud Nine - это торговая стратегия, основанная на индикаторе Ichimoku Cloud и объединенная с классификацией Уильямса. Эта стратегия использует несколько торговых сигналов, предоставляемых индикатором Ichimoku Cloud, для создания торговых сигналов. Это стратегия, ориентированная на реальные сделки.

Стратегический принцип

В основном эта стратегия основана на следующих сигналах Ичимоку:

- Облачный прорыв: сигнал, который возникает, когда цена закрывается, прорывая верхний или нижний край облака

- TK-пересечение: сигнал, генерируемый при пересечении поворотной линии (Tenkan) и базовой линии (Kijun)

- Облачное поворотное движение: сигналы при пересечении линий Senkou Span A и Senkou Span B

- Краевой пересечение: сигнал, когда цена переходит из одного облака в другое

Кроме того, эта стратегия может привести к пассивному состоянию в следующих случаях:

- Ценовой сдвиг в облаке

- TK Прямая позиция при обратном скрещивании

- Williams пробивается на частично равновесном положении

Эта стратегия объединяет несколько торговых сигналов в Ichimoku Cloud Graph, чтобы повысить надежность торговых сигналов, а также использовать сортировку для установки стоп-лосса и контроля риска.

Стратегические преимущества

В отличие от стратегии с одним сигналом, эта стратегия использует несколько сигналов из Ichimoku Cloud Graph, чтобы отфильтровать некоторые ошибочные сигналы и повысить точность сигналов. При этом параметры стратегии могут быть гибко настроены для различных сортов и оптимизации параметров.

Кроме того, в стратегию вводятся Williams Breakthroughs для установки стоп-лосса, что позволяет более активно контролировать риск, блокировать прибыль и избегать крупных убытков.

Стратегический риск

Основные риски, связанные с этой стратегией:

- Показатели облачных графиков задерживаются и не отражают изменения цен

- Некоторые из них, возможно, слишком консервативны и упускают возможность.

- Потери от перелома

Для проблем с задержкой параметры могут быть соответствующим образом скорректированы или отключены части фильтровальных сигналов. Для риска отключения типа может быть скорректирована временная периодичность отключения типа или только частично.

Направление оптимизации стратегии

Эта стратегия может быть оптимизирована в следующих аспектах:

- Настройка параметров Ichimoku для различных циклов и сортов

- Настройка или отключение частичного фильтрационного сигнала, сохранение основного сигнала

- Настройка параметров сортировки с использованием более длительных временных периодов или с использованием только частичной остановки

- Добавление фильтров для других показателей, таких как показатели количественной мощности

Подвести итог

Стратегия Ichimoku Cloud Nine повышает точность и выигрышную вероятность сигналов, используя преимущества индикатора Cloud Chart, путем интеграции нескольких торговых сигналов Ichimoku Cloud Chart. Стратегия также использует сортировку в качестве метода остановки для контроля риска. Стратегия может быть оптимизирована с помощью параметров и сигналов и может применяться для многообразных алгоритмических торгов.

/*backtest

start: 2024-01-19 00:00:00

end: 2024-02-18 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Ichimoku Cloud Nine", shorttitle="Ichimoku Cloud Nine", overlay=true, calc_on_every_tick = true, calc_on_order_fills = false, initial_capital = 5000, currency = "USD", default_qty_type = "percent_of_equity", default_qty_value = 10, pyramiding = 3, process_orders_on_close = true)

color green = #459915- 1