Стратегия разворота при пробое канала

Обзор

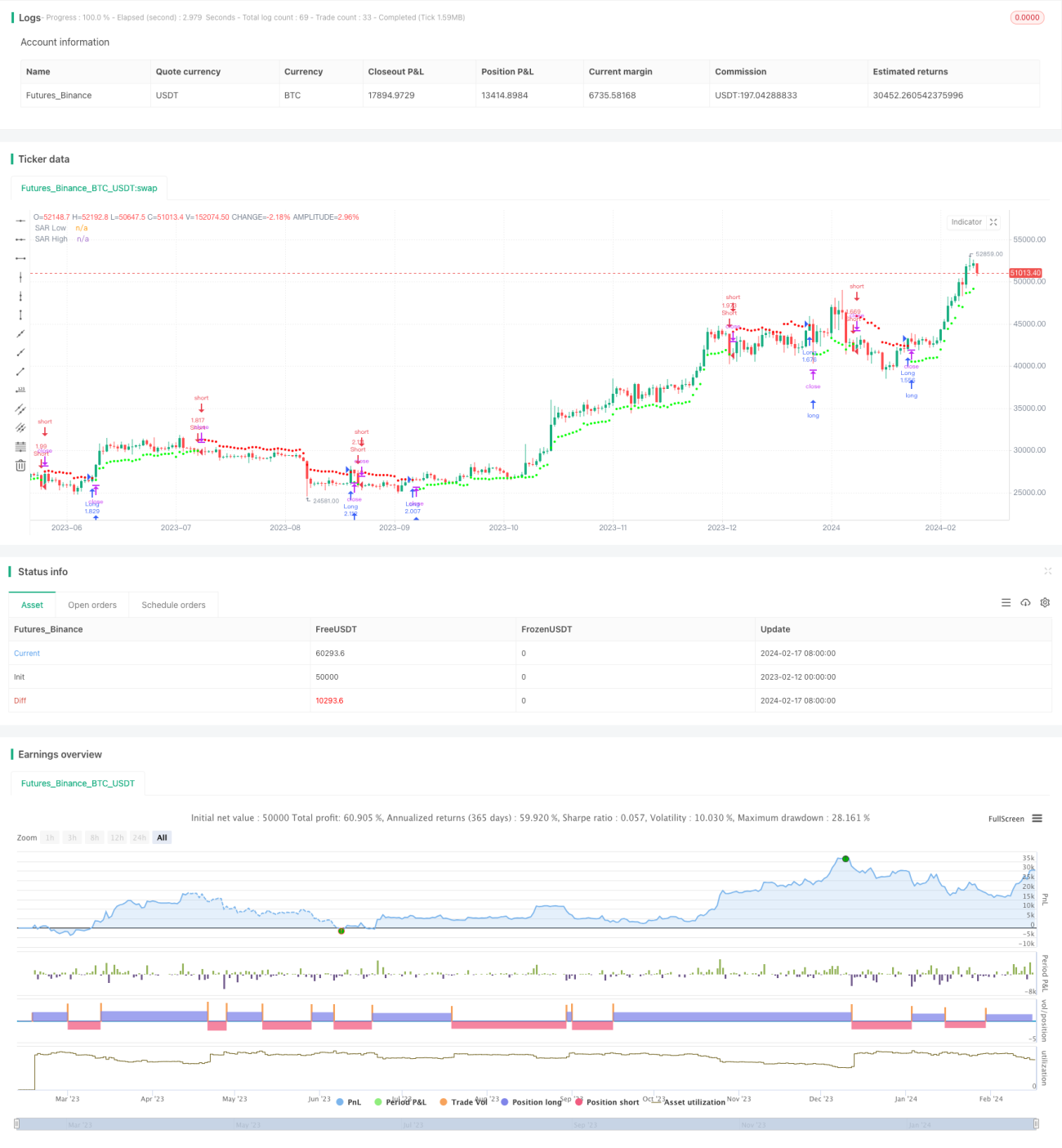

Стратегия разворота на пробой канала — это стратегия разворота с плавающими уровнями тейк-профита и стоп-лосса, следующими за ценовым каналом. Она использует взвешенное скользящее среднее для расчета ценового канала и открывает длинные или короткие позиции при пробое ценой границ канала.

Принцип стратегии

Стратегия сначала рассчитывает волатильность цены с помощью индикатора Average True Range (ATR) Уайлдера. Затем на основе значения ATR вычисляется константа среднего диапазона (ARC), которая равна половине ширины ценового канала. После этого рассчитываются верхняя и нижняя границы канала, которые служат точками тейк-профита и стоп-лосса, называемыми точками SAR. Когда цена пробивает верхнюю границу, открывается короткая позиция, при пробое нижней границы — длинная.

Конкретно, сначала рассчитывается ATR за последние N свечей. Затем ATR умножается на коэффициент для получения ARC. Умножение на коэффициент позволяет регулировать ширину канала. ARC прибавляется к максимальной цене закрытия за N свечей для получения верхней границы канала (верхний SAR). Вычитание ARC из минимальной цены закрытия дает нижнюю границу канала (нижний SAR). Если цена закрытия пробивает верхнюю границу, открывается короткая позиция; если пробивает нижнюю границу — длинная.

Преимущества стратегии

- Использование адаптивного канала на основе волатильности позволяет отслеживать изменения рынка.

- Разворотная торговля подходит для рынков со сменой тренда.

- Плавающие уровни тейк-профита и стоп-лосса позволяют фиксировать прибыль и контролировать риски.

Риски стратегии

- Разворотная торговля подвержена ложным входам, требуется правильная настройка параметров.

- На рынках с сильными колебаниями позиции могут быть закрыты преждевременно.

- Неправильные параметры могут привести к чрезмерно частым сделкам.

Способы решения:

- Оптимизация периода ATR и коэффициента ARC для установления разумной ширины канала.

- Добавление фильтров входа с использованием трендовых индикаторов.

- Увеличение периода ATR для снижения частоты сделок.

Направления оптимизации

- Оптимизация периода ATR и коэффициента ARC.

- Добавление условий открытия позиций, например, совместно с индикатором MACD.

- Внедрение дополнительных стоп-лосс стратегий.

Заключение

Стратегия разворота на пробой канала использует канал для отслеживания изменения цены, открывает позиции при усилении волатильности в направлении разворота и устанавливает адаптивные плавающие уровни тейк-профита и стоп-лосса. Эта стратегия подходит для консолидирующихся рынков с преобладанием разворотов. При точном определении точек разворота она может принести хорошую доходность. Однако необходимо следить за тем, чтобы уровни стоп-лосса не были слишком широкими, и уделять внимание оптимизации параметров.

- 1