رجحان الٹنے والی ٹریلنگ اسٹاپ لاس حکمت عملی

خلاصہ

یہ حکمت عملی رجحان کے الٹنے کے اشارے پر مبنی ہے، رجحان کی پیروی کرنے والے اسٹاپ نقصان کے طریقہ کار کے ساتھ مل کر، رجحانی مارکیٹ میں رجحان کی پیروی کرنے اور سائیڈ ویز مارکیٹ میں نقصان کو کم کرنے کا اثر حاصل کرتی ہے۔

حکمت عملی کا اصول

یہ حکمت عملی ہل مووینگ ایوریج کو رجحان کے تعین کے لیے بنیادی اشارے کے طور پر استعمال کرتی ہے۔ جب قیمت ہل اوسط سے اوپر جاتی ہے تو لمبی پوزیشن لی جاتی ہے، جب قیمت ہل اوسط سے نیچے آتی ہے تو چھوٹی پوزیشن لی جاتی ہے۔ اس کے ساتھ ساتھ، میک گلنلے اوسط کا استعمال رجحان کی تصدیق کے لیے کیا جاتا ہے۔

پوزیشن کھولنے کے بعد، اگر قیمت الٹ جائے، یعنی جب ہل اوسط کا کراس اوور ہوتا ہے تو رجحان تبدیل کرنے کی منطق عمل میں آتی ہے اور موجودہ پوزیشن بند کر دی جاتی ہے۔

یہ حکمت عملی رجحان کی پیروی کرنے والے اسٹاپ نقصان کے طریقہ کار کو بھی شامل کرتی ہے۔ پوزیشن کھولنے کے بعد، ATR کی بنیاد پر متحرک اسٹاپ نقصان کی سطح کا حساب لگایا جاتا ہے۔ قیمت کی حرکت کے ساتھ، اسٹاپ نقصان کی لکیر بھی متحرک طور پر ایڈجسٹ ہوتی رہتی ہے، جس سے منافع کی پیروی کرنے والا اسٹاپ نقصان حاصل ہوتا ہے۔

حکمت عملی کے فوائد

- ہل اوسط کا استعمال رجحان کے الٹنے کے مقامات کا تعین کرنے کے لیے، ہل اوسط بریک آؤٹ سگنلز کے لیے حساس ہے

- میک گلنلے اوسط کے ساتھ رجحان کی تصدیق، جھوٹے بریک آؤٹس کو فلٹر کرنے میں مدد ملتی ہے

- متحرک پیروی کرنے والے اسٹاپ نقصان کا طریقہ کار، مارکیٹ کی اتار چڑھاؤ کے مطابق اسٹاپ نقصان کی وسعت کو ایڈجسٹ کر سکتا ہے، نقصان کو مؤثر طریقے سے کنٹرول کرتا ہے

- ہل اوسط کی تصدیق کے وقت رجحان کے الٹنے پر فوری ردعمل، نقصان کو مزید بڑھنے سے روکتا ہے

- مختلف پیرامیٹر کے امتزاج کو آسانی سے تبدیل کر کے جانچ کر سکتے ہیں، بہترین پیرامیٹر تلاش کر سکتے ہیں

خطرات اور حل

-

اتار چڑھاؤ والی مارکیٹ میں اسٹاپ نقصان متحرک ہونے کا امکان

- اسٹاپ نقصان کی وسعت کو مناسب حد تک بڑھایا جا سکتا ہے، اسٹاپ نقصان بفر میں اضافہ کیا جا سکتا ہے

-

شدید مارکیٹ میں، پیروی کرنے والا اسٹاپ نقصان قیمت کی حرکت کے ساتھ نہیں رہ سکتا

- ہموار کرنے کی مدت کو کم کیا جا سکتا ہے تاکہ اسٹاپ نقصان قیمت کے ساتھ تیزی سے آگے بڑھ سکے

-

جھوٹے بریک آؤٹ غیر ضروری نقصان کا سبب بن سکتے ہیں

- تصدیق کے لیے دیگر اشارے شامل کیے جا سکتے ہیں، جھوٹے بریک آؤٹ سے بچا جا سکتا ہے

-

نامناسب پیرامیٹر حکمت عملی کی کارکردگی کو خراب کر سکتے ہیں

- مختلف مارکیٹ سائیکلوں میں بیک ٹیسٹ کر کے بہترین پیرامیٹر تلاش کیے جا سکتے ہیں

بہتری کے خیالات

- دیگر اشارے جیسے کینڈل سٹک پیٹرن، بولنگر بینڈز، RSI وغیرہ شامل کر کے تصدیق، سگنل کے معیار کو بہتر بنایا جا سکتا ہے

- مختلف مصنوعات اور وقت کے فریموں کے پیرامیٹرز کو بہتر بنا کر بہترین امتزاج تلاش کیا جا سکتا ہے

- مشین لرننگ جیسے طریقوں سے پیرامیٹر کی خودکار بہتری کی کوشش کی جا سکتی ہے

- اسٹاپ نقصان کے الگورتھم کو بہتر بنایا جا سکتا ہے، اسٹاپ نقصان کو یقینی بناتے ہوئے غیر ضروری اسٹاپ نقصان کو کم کیا جا سکتا ہے

- سرمایہ کے انتظام کے ساتھ پوزیشن کے انتظام کی حکمت عملی کو بہتر بنایا جا سکتا ہے

- خودکار منافع لینے کے طریقہ کار کو شامل کرنے پر غور کیا جا سکتا ہے

خلاصہ

یہ حکمت عملی مجموعی طور پر ایک مستحکم رجحان کی پیروی کرنے والی حکمت عملی ہے۔ مقررہ اسٹاپ نقصان کے مقابلے میں، یہ حکمت عملی متحرک اسٹاپ نقصان کے طریقہ کار کا استعمال کرتی ہے، جو مارکیٹ کی اتار چڑھاؤ کے مطابق اسٹاپ نقصان کی وسعت کو ایڈجسٹ کر سکتی ہے، اسٹاپ نقصان میں پھنسنے کے امکان کو مؤثر طریقے سے کم کرتی ہے۔ اس کے ساتھ ساتھ، ہل اوسط اور رجحان تبدیل کرنے کی منطق کا تعارف رجحان کے الٹنے پر تیز ردعمل کی اجازت دیتا ہے۔ تاہم، اس حکمت عملی میں کچھ خطرات بھی ہیں، جیسے اتار چڑھاؤ والی مارکیٹ میں اسٹاپ نقصان کا خطرہ، جھوٹے بریک آؤٹ کا خطرہ وغیرہ۔ اشارے کے پیرامیٹرز، اسٹاپ نقصان الگورتھم، پوزیشن مینجمنٹ وغیرہ کو مزید بہتر بنا کر، حکمت عملی مختلف مارکیٹوں میں زیادہ مستحکم کارکردگی حاصل کر سکتی ہے۔

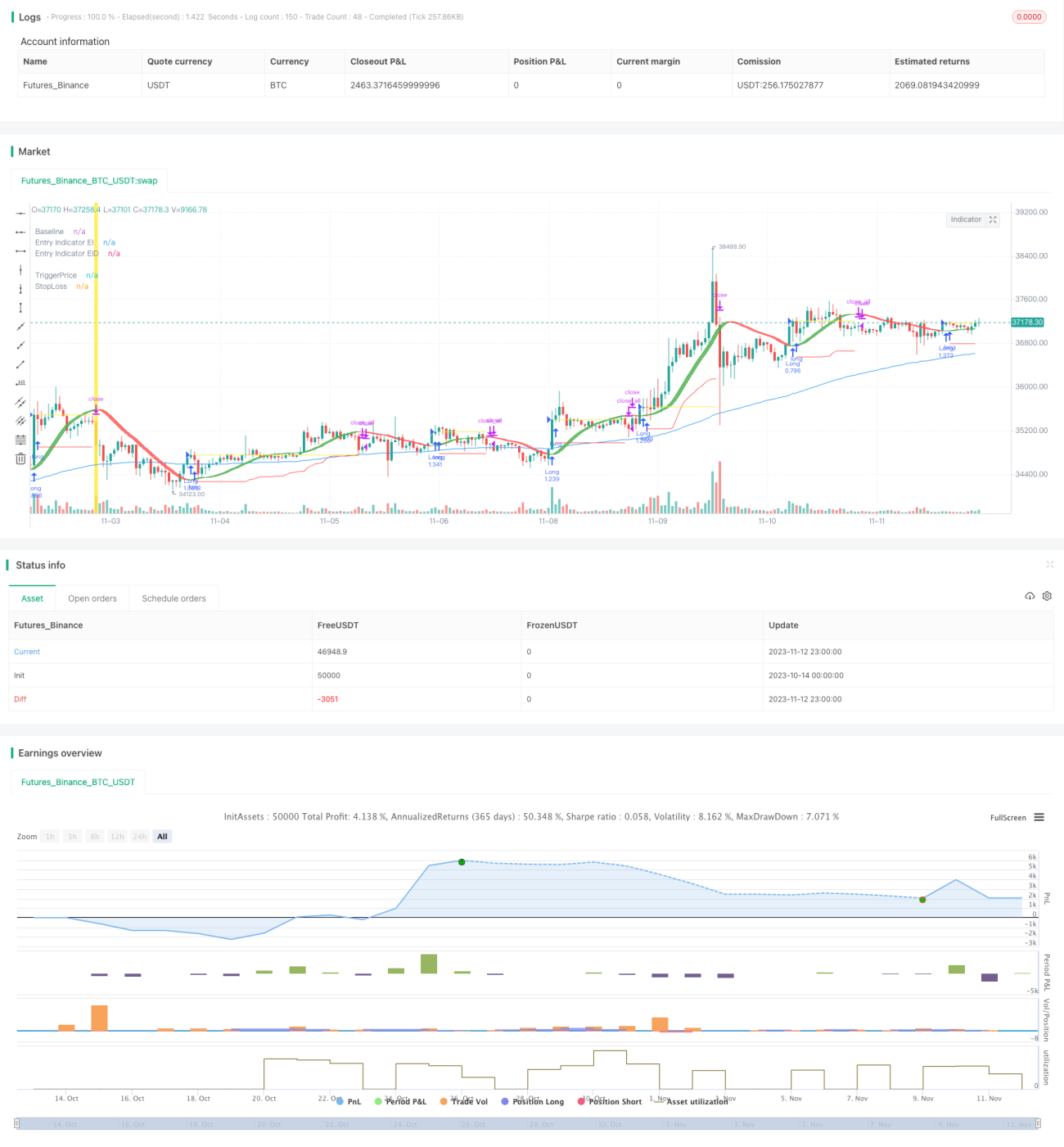

/*backtest

start: 2023-10-14 00:00:00

end: 2023-11-13 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// © Milleman

//@version=4

strategy("MilleMachine", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital=10000, commission_type=strategy.commission.percent, commission_value=0.06)

- 1