رجحان بریک آؤٹ ڈبل موونگ ایوریج فلٹر حکمت عملی

خلاصہ

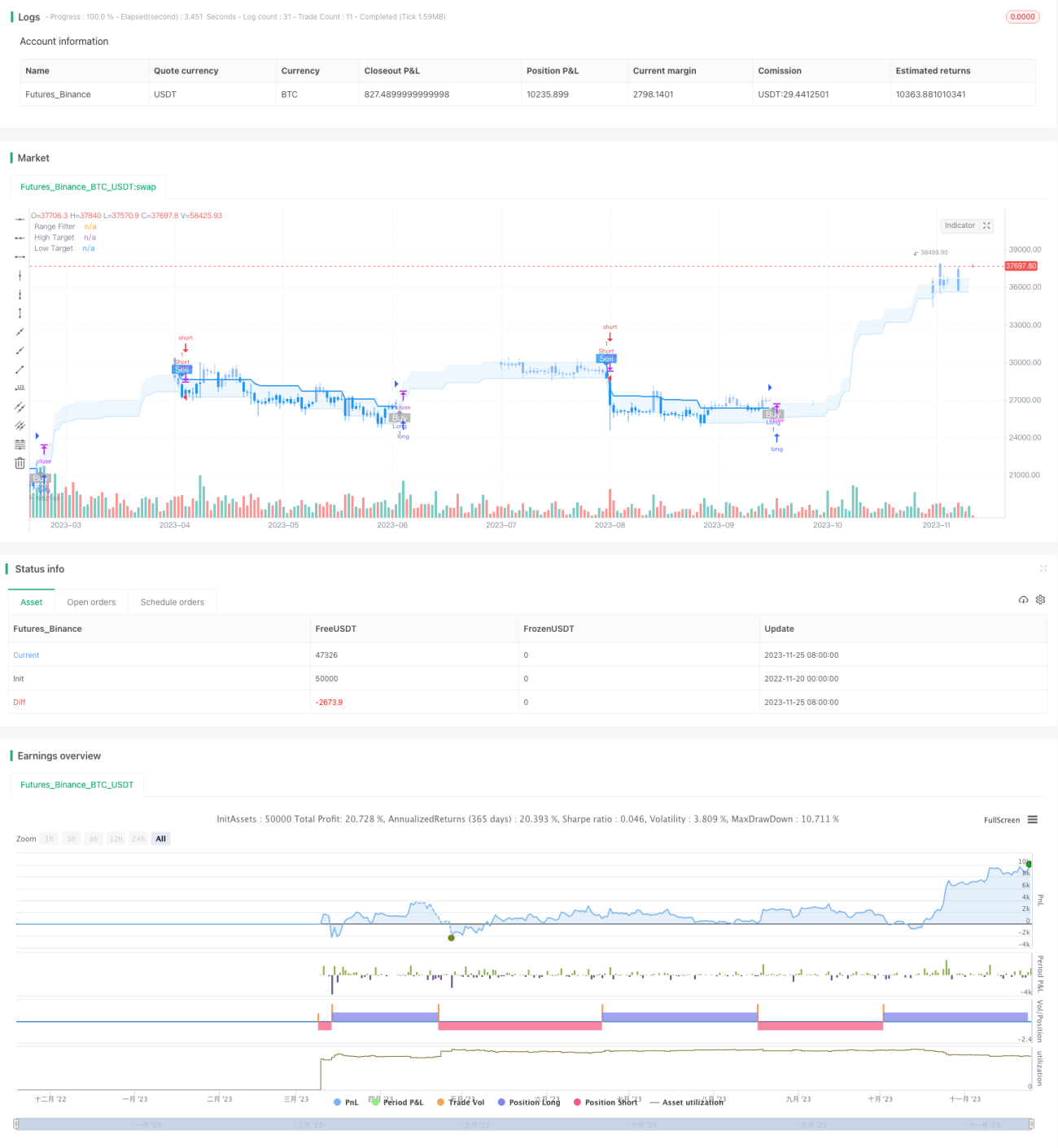

یہ ایک حکمت عملی ہے جو متحرک اوسط (Moving Averages) اور بولنگر بینڈ (Bollinger Bands) کا استعمال کرتے ہوئے رجحان کا تعین کرتی ہے اور بریک آؤٹ فلٹرنگ اور سٹاپ لاس کے اصول پر مبنی ہے۔ یہ رجحان میں تبدیلی کے وقت بروقت سگنل پکڑ سکتی ہے، دوہری متحرک اوسط کے ذریعے غلط سگنلز کو کم کرتی ہے، اور خطرے کو کنٹرول کرنے کے لیے سٹاپ لاس سیٹ کرتی ہے۔

حکمت عملی کا اصول

یہ حکمت عملی بنیادی طور پر درج ذیل حصوں پر مشتمل ہے:

-

رجحان کا تعین: MACD کا استعمال کرتے ہوئے قیمت کے رجحان کا تعین کیا جاتا ہے، اور تیزی (Bullish) اور مندی (Bearish) کے رجحانات میں فرق کیا جاتا ہے۔

-

حدود کی فلٹرنگ: بولنگر بینڈ کا استعمال قیمت کی اتار چڑھاؤ کی حد کا تعین کرنے اور ان سگنلز کو فلٹر کرنے کے لیے کیا جاتا ہے جو حد سے باہر نہیں جاتے۔

-

دوہری متحرک اوسط کی تصدیق: تیز رفتار EMA اور سست رفتار EMA پر مشتمل دوہری متحرک اوسط رجحان کے سگنل کی تصدیق کے لیے استعمال ہوتی ہے۔ صرف اس وقت خرید کا سگنل پیدا ہوتا ہے جب تیز رفتار EMA، سست رفتار EMA سے زیادہ ہو۔

-

سٹاپ لاس کا طریقہ کار: سٹاپ لاس پوائنٹ مقرر کیا جاتا ہے، اور جب قیمت ناپسندیدہ سمت میں سٹاپ لاس کو توڑتی ہے تو پوزیشن بند کر دی جاتی ہے۔

داخلے کے سگنل کے تعین کا منطق یہ ہے:

- MACD اوپر کی طرف رجحان ظاہر کرے۔

- قیمت بولنگر بینڈ کے اوپری بینڈ کو توڑے۔

- تیز رفتار EMA، سست رفتار EMA سے زیادہ ہو۔

جب یہ تینوں شرائط بیک وقت پوری ہوں تو خرید کا سگنل پیدا ہوتا ہے۔

پوزیشن بند کرنے کا منطق دو طرح کا ہے: منافع پر بند کرنا اور نقصان پر بند کرنا۔ منافع کا پوائنٹ داخلے کی قیمت کو ایک خاص تناسب سے ضرب دے کر مقرر کیا جاتا ہے، اور نقصان کا پوائنٹ بھی اسی طرح مقرر کیا جاتا ہے۔ جب قیمت ان میں سے کسی ایک پوائنٹ کو توڑتی ہے تو پوزیشن بند کر دی جاتی ہے۔

فوائد کا تجزیہ

اس حکمت عملی کے درج ذیل فوائد ہیں:

- یہ رجحان کی تبدیلی کو بروقت پکڑ سکتی ہے، اور پچھلی غلطیوں (traceback) کو کم کرتی ہے۔

- دوہری متحرک اوسط کے ذریعے غلط سگنلز کو فلٹر کرکے سگنل کے معیار کو بہتر بناتی ہے۔

- سٹاپ لاس کا طریقہ کار ایک ہی لین دین میں ہونے والے نقصان کو مؤثر طریقے سے کنٹرول کرتا ہے۔

- پیرامیٹرز کو بہتر بنانے کی گنجائش زیادہ ہے، اور انہیں بہترین حالت میں ڈھالا جا سکتا ہے۔

خطرے کا تجزیہ

اس حکمت عملی میں کچھ خطرات بھی موجود ہیں:

- اتار چڑھاؤ والی مارکیٹ (Sideways market) میں پیدا ہونے والے غلط سگنلز نقصان کا سبب بن سکتے ہیں۔

- سٹاپ لاس پوائنٹ کی نامناسب تعیناتی غیر ضروری نقصان کا باعث بن سکتی ہے۔

- پیرامیٹرز کی نامناسب ترتیب حکمت عملی کی کارکردگی کو خراب کر سکتی ہے۔

ان خطرات سے نمٹنے کے لیے پیرامیٹرز کو بہتر بنانے، سٹاپ لاس کی پوزیشن کو ایڈجسٹ کرنے جیسے طریقوں سے بہتری اور اصلاح کی جا سکتی ہے۔

بہتری کے امکانات

اس حکمت عملی کو درج ذیل سمتوں سے بہتر بنایا جا سکتا ہے:

- دوہری متحرک اوسط کی لمبائی کو ایڈجسٹ کرکے بہترین پیرامیٹر کنبینیشن تلاش کرنا۔

- مختلف سٹاپ لاس طریقوں جیسے ٹریلنگ سٹاپ (Trailing Stop)، رینج سٹاپ (Range Stop) وغیرہ کا تجربہ کرنا۔

- MACD کے پیرامیٹرز کو جانچ کر بہترین پیرامیٹر تلاش کرنا۔

- مشین لرننگ کا استعمال کرتے ہوئے پیرامیٹرز کی خودکار بہتری کرنا۔

- سگنل فلٹرنگ کے لیے اضافی شرائط شامل کرنا۔

مختلف پیرامیٹر سیٹنگز کی جانچ کرکے اور منافع کی شرح (Return Rate) اور شارپ ریشو (Sharpe Ratio) کا جائزہ لے کر اس حکمت عملی کی بہترین حالت تلاش کی جا سکتی ہے۔

خلاصہ

یہ ایک مقداری حکمت عملی ہے جو رجحان کے تعین، حدود کی فلٹرنگ، دوہری متحرک اوسط کی تصدیق اور سٹاپ لاس کے تصور کا استعمال کرتی ہے۔ یہ رجحان کی سمت کو مؤثر طریقے سے شناخت کر سکتی ہے اور منافع کو زیادہ سے زیادہ کرنے اور خطرے کو کنٹرول کرنے کے درمیان توازن قائم کر سکتی ہے۔ پیرامیٹرز کی بہتری اور مشین لرننگ جیسے طریقوں سے اس حکمت عملی میں بہتری کی بڑی گنجائش ہے، جس سے بہتر نتائج حاصل کیے جا سکتے ہیں۔

/*backtest

start: 2022-11-20 00:00:00

end: 2023-11-26 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(title="Range Filter Buy and Sell Strategies", shorttitle="Range Filter Strategies", overlay=true,pyramiding = 5)

// Original Script > @DonovanWall- 1