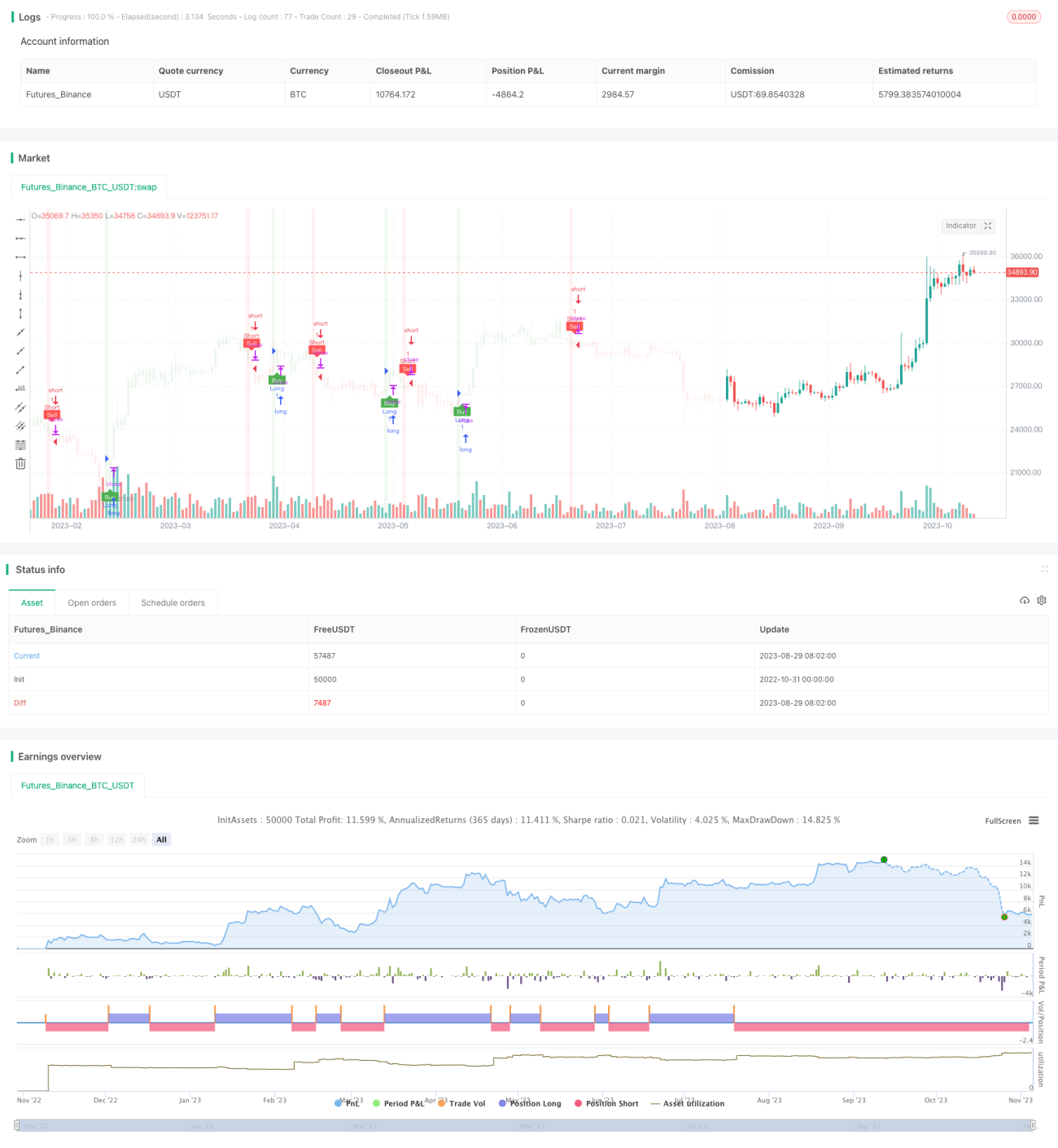

Chiến lược giao dịch dựa trên đường trung bình động T3 và ATR

Tổng quan

Chiến lược này sử dụng kết hợp đường trung bình động T3, chỉ báo ATR và Heiken Ashi để xác định tín hiệu mua và bán, đồng thời tính toán mức cắt lỗ và chốt lời dựa trên ATR, thực hiện giao dịch theo xu hướng. Ưu điểm của chiến lược là phản ứng nhanh, đồng thời kiểm soát được rủi ro giao dịch.

Phân tích nguyên lý

Tính toán chỉ báo

-

Đường trung bình động T3: Tính đường trung bình động T3 với tham số làm mịn là T3 (mặc định 100), dùng để xác định hướng xu hướng.

-

ATR: Tính ATR (Average True Range - Biên độ dao động trung bình thực tế), dùng để xác định kích thước các mức cắt lỗ và chốt lời.

-

Dừng lỗ động ATR: Tính một đường cắt lỗ động dựa trên ATR, có thể điều chỉnh theo biến động giá và mức độ biến động, thực hiện theo dõi xu hướng.

Logic giao dịch

-

Tín hiệu mua: Khi giá đóng cửa cắt lên trên đường cắt lỗ động ATR và thấp hơn đường trung bình T3, phát sinh tín hiệu mua.

-

Tín hiệu bán: Khi giá đóng cửa cắt xuống dưới đường cắt lỗ động ATR và cao hơn đường trung bình T3, phát sinh tín hiệu bán.

-

Cắt lỗ và chốt lời: Sau khi vào lệnh, tính toán giá cắt lỗ và chốt lời dựa trên giá trị ATR và tỷ lệ rủi ro/lợi nhuận do người dùng thiết lập.

Điểm vào và ra của chiến lược

-

Sau khi mua, giá cắt lỗ là giá vào lệnh trừ đi giá trị ATR, giá chốt lời là giá vào lệnh cộng với giá trị ATR nhân với tỷ lệ rủi ro/lợi nhuận.

-

Sau khi bán, giá cắt lỗ là giá vào lệnh cộng với giá trị ATR, giá chốt lời là giá vào lệnh trừ đi giá trị ATR nhân với tỷ lệ rủi ro/lợi nhuận.

-

Khi giá chạm mức cắt lỗ hoặc chốt lời, đóng vị thế thoát lệnh.

Phân tích ưu điểm

Phản ứng nhanh

Đường trung bình T3 có tham số mặc định là 100, nhạy hơn so với đường trung bình động thông thường, có thể phản ứng nhanh hơn với sự thay đổi giá.

Kiểm soát rủi ro

Đường cắt lỗ động sử dụng ATR có thể theo dõi giá theo biến động thị trường, tránh rủi ro bị phá vỡ mức cắt lỗ. Vị trí cắt lỗ/chốt lời dựa trên ATR có thể kiểm soát tỷ lệ rủi ro/lợi nhuận của mỗi giao dịch.

Theo dõi xu hướng

Đường cắt lỗ động ATR có thể bám theo xu hướng, ngay cả khi giá điều chỉnh ngắn hạn cũng không kích hoạt thoát lệnh, từ đó giảm tín hiệu sai.

Không gian tối ưu hóa tham số

Chu kỳ đường trung bình T3 và chu kỳ ATR đều có thể tối ưu hóa, từ đó điều chỉnh tham số cho các thị trường khác nhau, nâng cao độ ổn định của chiến lược.

Phân tích rủi ro

Rủi ro đột phá

Nếu thị trường biến động mạnh, giá có thể trực tiếp phá vỡ đường cắt lỗ gây thua lỗ. Có thể mở rộng chu kỳ ATR và khoảng cách cắt lỗ để giảm thiểu.

Rủi ro đảo chiều xu hướng

Khi xu hướng đảo chiều, giá vượt qua đường cắt lỗ động có thể gây thua lỗ. Có thể kết hợp các chỉ báo khác để xác định xu hướng, tránh giao dịch gần điểm đảo chiều.

Rủi ro tối ưu hóa tham số

Tối ưu hóa tham số cần dữ liệu lịch sử phong phú, tồn tại rủi ro tối ưu hóa quá mức. Nên sử dụng nhiều thị trường và nhiều khung thời gian để tối ưu hóa kết hợp tham số, không phụ thuộc vào một tập dữ liệu duy nhất.

Hướng tối ưu hóa

-

Kiểm tra các tham số chu kỳ khác nhau của đường trung bình động T3, tìm ra bộ tham số tối ưu cân bằng giữa độ nhạy và độ ổn định.

-

Kiểm tra tham số chu kỳ ATR, tìm ra sự cân bằng tối ưu giữa kiểm soát rủi ro và bắt xu hướng.

-

Kết hợp các chỉ báo như RSI, MACD để tránh giao dịch sai tại điểm đảo chiều xu hướng.

-

Sử dụng phương pháp học máy để huấn luyện tham số tối ưu, giảm hạn chế của tối ưu hóa thủ công.

-

Bổ sung chiến lược quản lý vị thế để kiểm soát rủi ro tốt hơn.

Tổng kết

Chiến lược này tích hợp ưu điểm của đường trung bình T3 và chỉ báo ATR, vừa phản ứng nhanh với biến động giá, vừa kiểm soát được rủi ro. Thông qua tối ưu hóa tham số và kết hợp các chỉ báo khác có thể nâng cao hơn nữa độ ổn định và hiệu quả giao dịch. Tuy nhiên, nhà giao dịch vẫn cần chú ý đến rủi ro đảo chiều và đột phá, tránh phụ thuộc quá mức vào kết quả backtest.

- 1