Chiến lược đột phá biên độ động

Tổng quan

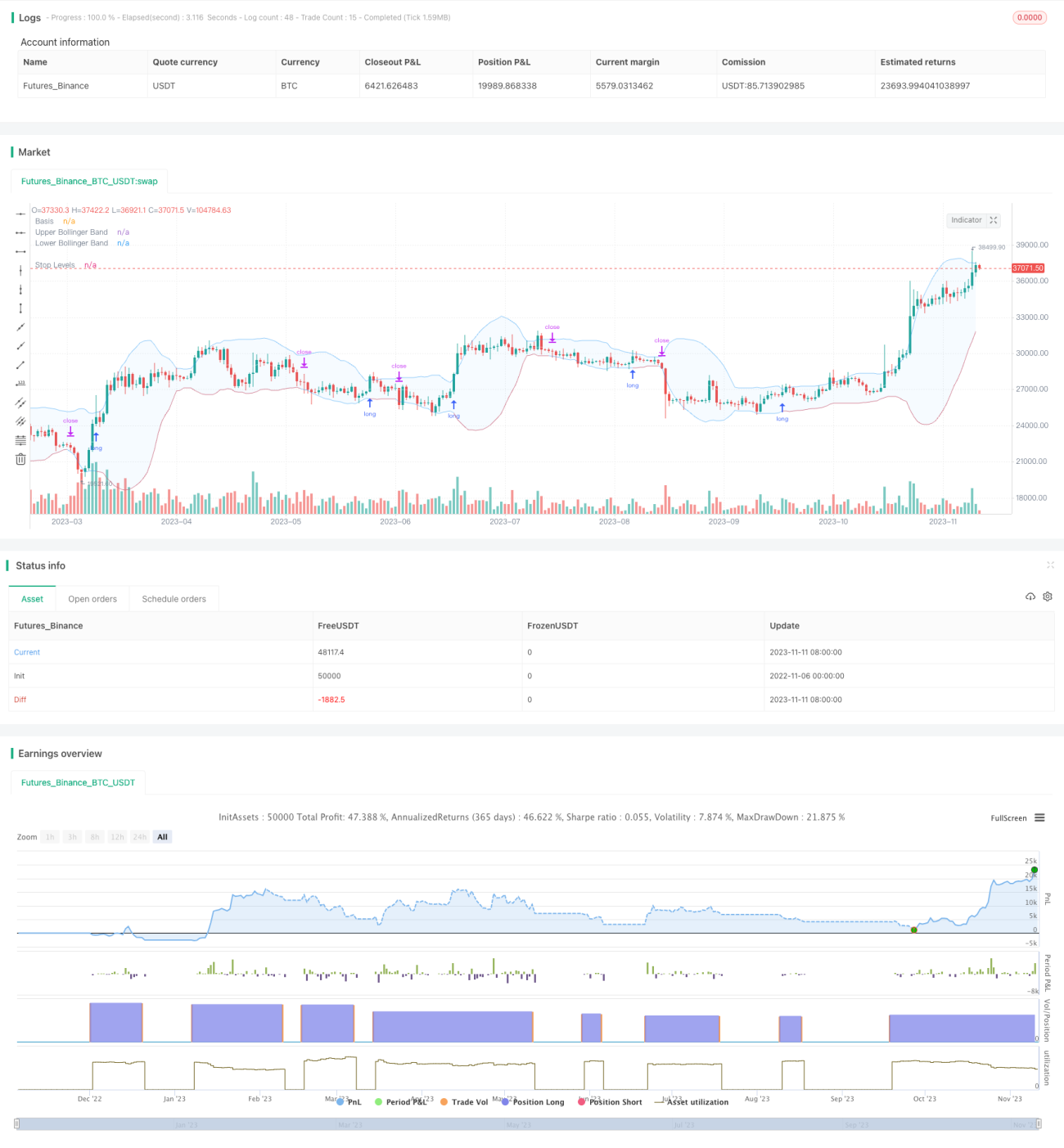

Chiến lược này sử dụng dải trên và dải dưới động của Bollinger Bands để thực hiện lệnh mua khi giá phá vỡ dải trên và đóng vị thế khi giá phá vỡ dải dưới. Khác với chiến lược đột phá truyền thống, dải trên và dưới của Bollinger Bands thay đổi linh hoạt dựa trên biến động lịch sử, giúp đánh giá tốt hơn trạng thái quá mua/quá bán của thị trường.

Nguyên lý chiến lược

Chiến lược chủ yếu dựa vào chỉ báo Bollinger Bands để xác định sự đột phá giá. Bollinger Bands bao gồm ba đường:

- Đường giữa: Đường trung bình động n ngày

- Dải trên: Đường giữa + k * độ lệch chuẩn n ngày

- Dải dưới: Đường giữa - k * độ lệch chuẩn n ngày

Khi giá tăng vượt quá dải trên, thị trường được coi là ở trạng thái quá mua, có thể mua vào. Khi giá giảm vượt quá dải dưới, thị trường được coi là ở trạng thái quá bán, nên đóng vị thế.

Chiến lược cho phép tùy chỉnh các tham số Bollinger Bands: độ dài đường giữa n và bội số độ lệch chuẩn k. Mặc định độ dài đường giữa là 20 ngày, bội số độ lệch chuẩn là 2.

Sau khi thị trường đóng cửa mỗi ngày, kiểm tra xem giá đóng cửa có phá vỡ dải trên hay không. Nếu có, vào đầu phiên giao dịch ngày hôm sau sẽ thực hiện tín hiệu mua. Sau khi mua, theo dõi giá theo thời gian thực xem có phá vỡ dải dưới hay không, nếu có thì đóng vị thế.

Chiến lược cũng áp dụng bộ lọc đường trung bình động, chỉ khi giá cao hơn đường trung bình động mới phát sinh tín hiệu mua. Có thể chọn vẽ đường trung bình động ở chu kỳ hiện tại hoặc chu kỳ cao hơn để kiểm soát thời điểm vào lệnh.

Phương thức cắt lỗ cũng cung cấp hai lựa chọn: cắt lỗ theo tỷ lệ phần trăm cố định hoặc theo dõi dải dưới Bollinger Bands. Phương thức sau mang lại không gian lớn hơn để lợi nhuận chạy.

Ưu điểm của chiến lược

- Sử dụng Bollinger Bands để xác định trạng thái quá mua/quá bán của thị trường

- Bộ lọc đường trung bình động, tránh giao dịch ngược xu hướng

- Có thể tùy chỉnh tham số Bollinger Bands, thích ứng với các chu kỳ khác nhau

- Cung cấp hai lựa chọn phương thức cắt lỗ

- Hỗ trợ tối ưu hóa tham số trong backtest, xác thực chiến lược trên thực tế

Rủi ro của chiến lược

- Bollinger Bands không thể xác định hoàn toàn tình trạng quá mua/quá bán

- Bộ lọc đường trung bình động có thể bỏ lỡ cơ hội đột phá nhanh

- Cắt lỗ cố định có thể quá thận trọng, cắt lỗ theo dõi có thể quá mạo hiểm

- Cần tối ưu hóa tham số để thích ứng với các loại tài sản và chu kỳ khác nhau

- Không thể giới hạn mức lỗ, cần phải quản lý vốn

Tối ưu hóa chiến lược

- Thử nghiệm các tổ hợp tham số đường trung bình động khác nhau

- Thử nghiệm các tham số Bollinger Bands khác nhau

- So sánh tỷ suất lợi nhuận giữa cắt lỗ theo tỷ lệ phần trăm cố định và cắt lỗ theo dõi dải dưới

- Thêm mô-đun quản lý vốn, giới hạn tổn thất mỗi giao dịch

- Kết hợp các chỉ báo khác để xác thực tín hiệu Bollinger Bands

Tổng kết

Chiến lược này sử dụng dải trên và dải dưới động của Bollinger Bands để xác định quá mua/quá bán, tham khảo bộ lọc đường trung bình động và sử dụng cắt lỗ để bảo vệ vốn. So với chiến lược đột phá dải cố định truyền thống, nó thích ứng tốt hơn với biến động thị trường. Thông qua tối ưu hóa tham số và kiểm soát rủi ro, có thể nâng cao hơn nữa tính ổn định và tỷ suất lợi nhuận của chiến lược. Nhìn chung, chiến lược này tận dụng tính linh hoạt của Bollinger Bands, thu được ưu điểm của chiến lược đột phá, đáng để thử nghiệm thực tế và theo dõi tối ưu hóa lâu dài.

- 1