Chiến lược dừng lỗ bám theo đảo chiều xu hướng

Tổng quan

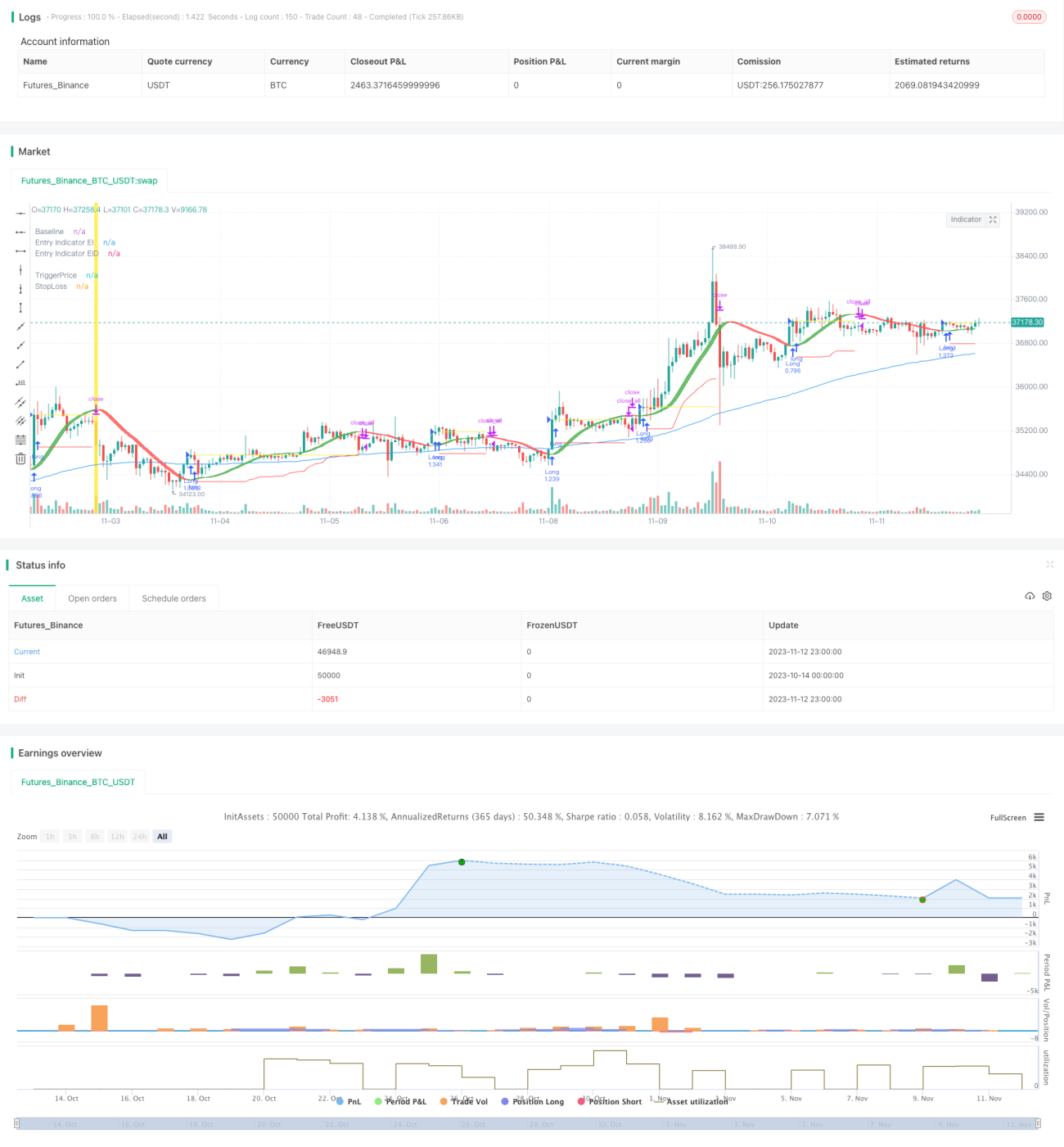

Chiến lược này dựa trên chỉ báo đảo chiều xu hướng, kết hợp cơ chế trailing stop theo xu hướng, nhằm theo dõi xu hướng trong thị trường có xu hướng và giảm thiểu thua lỗ trong thị trường đi ngang.

Nguyên lý chiến lược

Chiến lược sử dụng đường trung bình động Hull (Hull Moving Average) làm chỉ báo xu hướng chính. Khi giá cắt lên trên đường Hull, mua lên; khi giá cắt xuống dưới đường Hull, bán xuống. Đồng thời, kết hợp đường trung bình McGinley để xác nhận xu hướng.

Sau khi mở vị thế, nếu giá đảo chiều, tức là khi xảy ra giao cắt ngược của đường Hull, sẽ thực thi logic thay đổi xu hướng và đóng vị thế hiện tại.

Chiến lược này cũng áp dụng cơ chế trailing stop theo xu hướng. Sau khi mở vị thế, mức stop động sẽ được tính toán dựa trên ATR. Khi giá biến động, đường stop cũng được điều chỉnh linh hoạt, giúp trailing stop lợi nhuận.

Ưu điểm của chiến lược

- Sử dụng đường trung bình Hull để xác định điểm đảo chiều xu hướng, đường Hull có độ nhạy cao với các tín hiệu đột phá.

- Kết hợp đường trung bình McGinley để xác nhận xu hướng, giúp lọc bỏ một phần các đột phá giả.

- Áp dụng cơ chế trailing stop động, có thể điều chỉnh mức stop dựa trên biến động thị trường, kiểm soát thua lỗ hiệu quả.

- Khi đường Hull xác nhận đảo chiều, phản ứng kịp thời để tránh thua lỗ lan rộng.

- Dễ dàng chuyển đổi các bộ tham số khác nhau để thử nghiệm, tìm ra tham số tối ưu.

Rủi ro và giải pháp

-

Có thể xảy ra trường hợp stop bị kích hoạt trong thị trường đi ngang.

- Có thể mở rộng mức stop phù hợp, thêm vùng đệm stop.

-

Trong thị trường biến động mạnh, trailing stop có thể không theo kịp biến động giá.

- Có thể rút ngắn chu kỳ làm mịn để stop bắt kịp giá nhanh hơn.

-

Đột phá giả có thể dẫn đến thua lỗ không đáng có.

- Thêm các chỉ báo khác để xác nhận, tránh đột phá giả.

-

Tham số không phù hợp có thể khiến chiến lược hoạt động kém hiệu quả.

- Có thể backtest qua các chu kỳ thị trường khác nhau để tìm ra tham số tối ưu.

Hướng tối ưu hóa

- Thêm các chỉ báo khác để xác nhận, như mô hình nến, Bollinger Bands, RSI,... nhằm nâng cao chất lượng tín hiệu.

- Tối ưu hóa tham số cho từng sản phẩm, khung thời gian khác nhau để tìm bộ tham số tốt nhất.

- Có thể thử nghiệm các phương pháp học máy để tự động tối ưu hóa tham số.

- Tối ưu hóa thuật toán stop, đảm bảo dừng lỗ nhưng giảm thiểu các stop không cần thiết.

- Kết hợp quản lý vốn để tối ưu hóa chiến lược quản lý vị thế.

- Cân nhắc thêm cơ chế chốt lời tự động.

Tổng kết

Nhìn chung, đây là một chiến lược theo xu hướng khá ổn định. So với stop cố định, chiến lược này sử dụng cơ chế stop động, có thể điều chỉnh mức stop dựa trên biến động thị trường, giúp giảm xác suất stop bị kẹt. Đồng thời, việc đưa vào đường trung bình Hull và logic thay đổi xu hướng cho phép phản ứng nhanh với sự đảo chiều xu hướng. Tuy nhiên, chiến lược này cũng có những rủi ro nhất định, như rủi ro stop trong thị trường đi ngang, rủi ro đột phá giả,... Thông qua việc tối ưu hóa thêm tham số chỉ báo, thuật toán stop, quản lý vị thế, v.v., có thể giúp chiến lược đạt được hiệu suất ổn định hơn ở các thị trường khác nhau.

/*backtest

start: 2023-10-14 00:00:00

end: 2023-11-13 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// © Milleman

//@version=4

strategy("MilleMachine", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital=10000, commission_type=strategy.commission.percent, commission_value=0.06)

- 1