Chiến lược giao dịch hai chiều dựa trên khe hở nhiều đường trung bình động

Tổng quan

Chiến lược này sử dụng chỉ báo Williams High/Low để nhận diện tín hiệu đảo chiều đa xu hướng, kết hợp với nhiều đường trung bình động để giao dịch khoảng cách (gap trading), đồng thời hỗ trợ thêm chỉ báo RSI để lọc tín hiệu nhiễu, nhằm thực hiện giao dịch hai chiều hiệu quả.

Nguyên lý chiến lược

-

Chỉ báo Williams High/Low dựa vào giá cao nhất và giá thấp nhất trong một chu kỳ nhất định để xác định điểm ngoặt, phát ra tín hiệu mua và bán.

-

Các đường trung bình động 20, 50 và 100 ngày tạo thành nhiều đường trung bình, khi giá phá vỡ hai trong số các đường này, tín hiệu giao dịch được phát ra.

-

Chỉ báo RSI xác định vùng quá mua/quá bán, dùng để lọc các tín hiệu không chắc chắn.

-

Chiến lược xác định tín hiệu mua/bán ổn định bằng cách đánh giá giá phá vỡ hai đường trung bình nào, kết hợp với tín hiệu từ chỉ báo Williams và bộ lọc RSI.

-

Xác định điểm vào lệnh: Khi đường trung bình ngắn hạn cắt lên trên đường trung bình trung và dài hạn, đồng thời xuất hiện tín hiệu Williams thấp mới và RSI ở vùng thấp, thì vào lệnh mua (long); Khi đường trung bình ngắn hạn cắt xuống dưới đường trung bình trung và dài hạn, đồng thời xuất hiện tín hiệu Williams cao mới và RSI ở vùng cao, thì vào lệnh bán (short).

-

Cắt lỗ và chốt lời: Đặt mức cắt lỗ và chốt lời theo tỷ lệ cố định.

Lợi thế của chiến lược

-

Chỉ báo Williams xác định chính xác các mức hỗ trợ/kháng cự quan trọng, nhận diện tín hiệu đảo chiều.

-

Việc phá vỡ nhiều đường trung bình giúp tránh tín hiệu sai do dao động của một đường trung bình đơn lẻ.

-

Chỉ báo RSI hỗ trợ lọc tín hiệu nhiễu, giúp thời điểm vào lệnh chính xác và đáng tin cậy hơn.

-

Hệ thống cắt lỗ/chốt lời cố định kiểm soát rủi ro, giúp lợi nhuận và thua lỗ rõ ràng hơn.

-

Kết hợp chỉ báo đảo chiều và chỉ báo xu hướng để xác nhận kép, giúp tín hiệu giao dịch chính xác và đáng tin cậy hơn.

Rủi ro của chiến lược

-

Lựa chọn công cụ giao dịch không phù hợp, cần điều chỉnh tham số cho từng loại.

-

Lựa chọn chu kỳ không hợp lý, cần điều chỉnh tham số phù hợp với từng khung thời gian.

-

Cắt lỗ/chốt lời cố định không thể điều chỉnh theo biến động thị trường, có thể dẫn đến cắt lỗ sớm hoặc chốt lời chưa đủ.

-

Dễ phát sinh tín hiệu sai khi các đường trung bình dao động.

-

Tín hiệu bị trễ khi các chỉ báo phân kỳ.

Hướng tối ưu hóa chiến lược

-

Tối ưu hóa tham số động theo từng công cụ giao dịch.

-

Thêm hệ thống tự động điều chỉnh cắt lỗ/chốt lời, giúp lợi nhuận và thua lỗ hợp lý hơn.

-

Bổ sung thêm nhiều chỉ báo lọc như MACD, Stochastic, ... để giảm tín hiệu sai.

-

Thêm thuật toán học máy để tự động nhận diện thời điểm giao dịch tốt nhất.

-

Kết hợp thêm các chỉ báo xác định xu hướng để nhận diện thị trường có xu hướng.

Tổng kết

Chiến lược này kết hợp nhiều công cụ phân tích kỹ thuật như chỉ báo Williams, đường trung bình động và RSI, thông qua xác nhận kép để giảm tín hiệu sai, có thể nắm bắt hiệu quả các cơ hội đảo chiều, đồng thời kết hợp cắt lỗ/chốt lời cố định để kiểm soát rủi ro. Nhìn chung, đây là một chiến lược giao dịch hai chiều đáng tin cậy và thực tế. Bước tiếp theo có thể tăng cường hiệu quả chiến lược thông qua tối ưu hóa tham số, tối ưu hóa cắt lỗ/chốt lời và kết hợp mô hình.

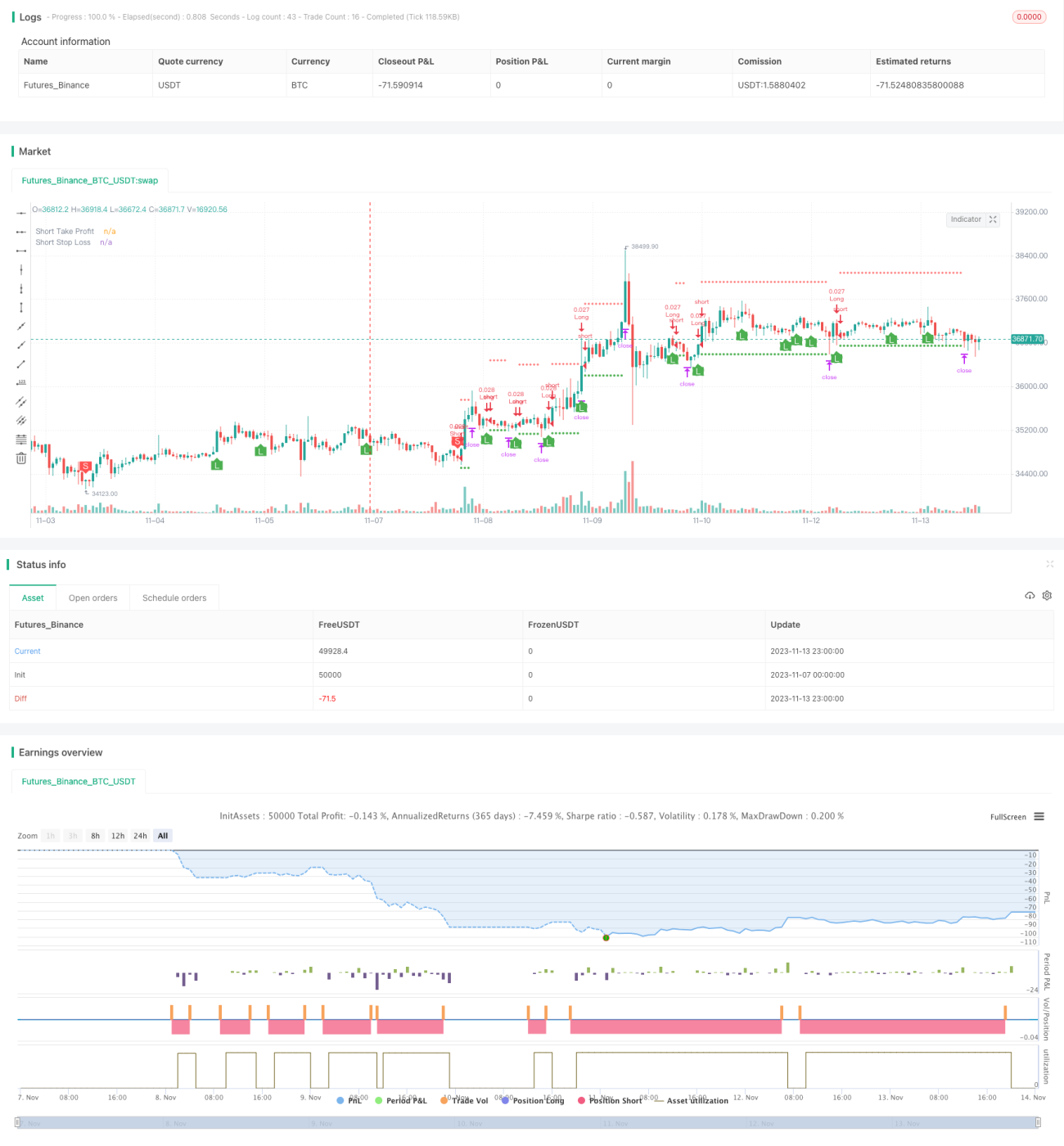

/*backtest

start: 2023-11-07 00:00:00

end: 2023-11-14 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © B_L_A_C_K_S_C_O_R_P_I_O_N

// v 1.1

- 1