Chiến lược scalping trong ngày điên rồ với sự kết hợp hai chỉ báo

Tổng quan

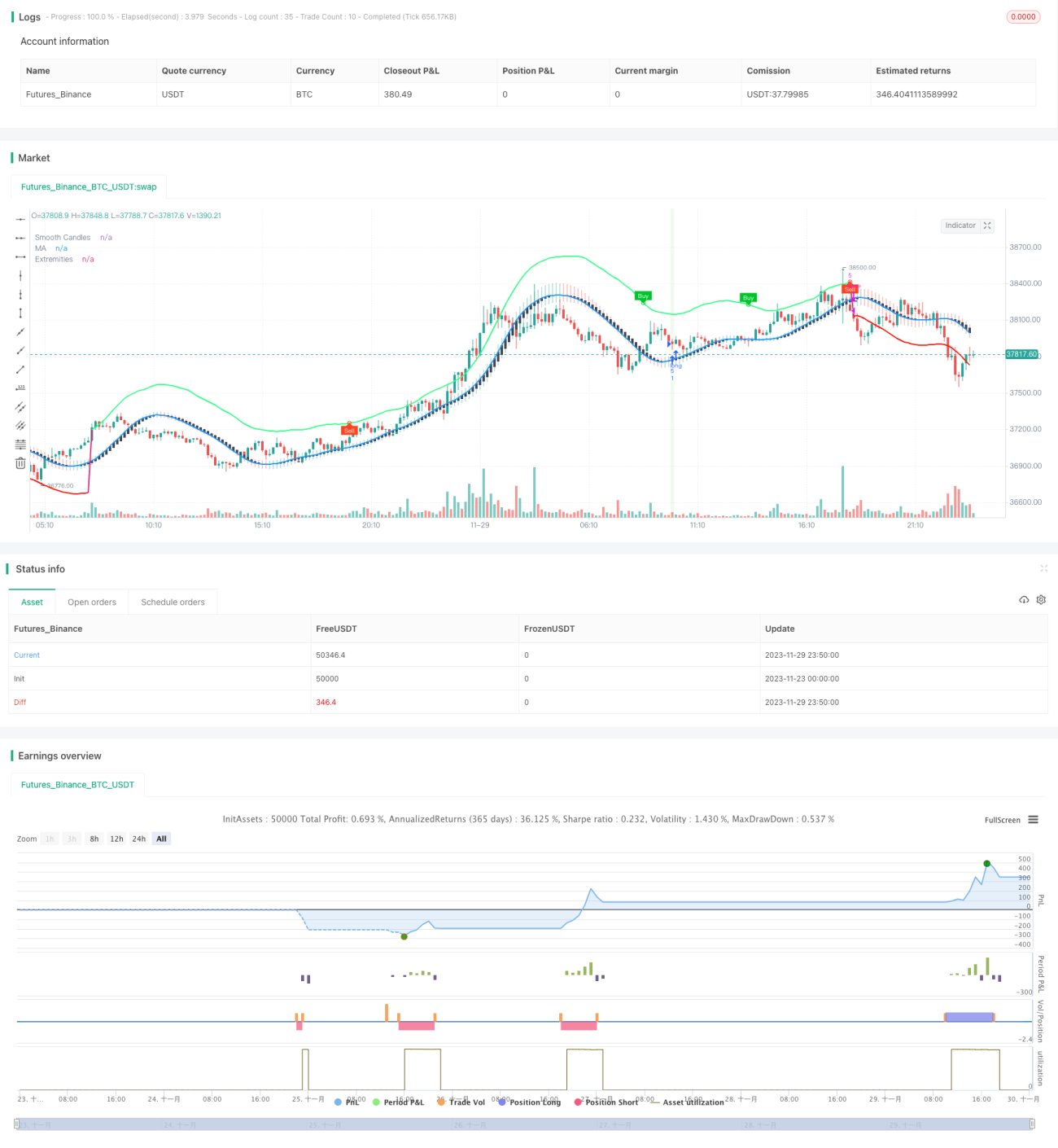

Chiến lược này kết hợp các tín hiệu mua bán của hai chỉ báo TMO và AMA do LuxAlgo phát triển, nhằm nắm bắt cơ hội bắt đầu xu hướng trong giai đoạn dao động. Nó sẽ mua hoặc bán sau khi thỏa mãn nhiều điều kiện như tín hiệu mua bán của chỉ báo TMO, điểm cực trị mua/bán của chỉ báo AMA, và sự gia tăng dần khối lượng thân nến. Phương pháp cắt lỗ sử dụng mức giá cao nhất và thấp nhất của N nến gần nhất.

Nguyên lý chiến lược

Chỉ báo TMO phản ánh động lượng giá. Nó thuộc loại chỉ báo dao động, có thể đưa ra tín hiệu giao dịch khi giá có sự phân kỳ. Chỉ báo AMA là một chỉ báo đường trung bình động trơn tru. Nó hiển thị một phạm vi biến động giá, khi giá tiến gần đến dải trên hoặc dưới thì cho thấy hiện tượng quá mua hoặc quá bán.

Logic chính mà chiến lược này dựa trên là: Chỉ báo TMO có thể phản ánh sự phân kỳ xu hướng giá để cung cấp tín hiệu giao dịch, chỉ báo AMA có thể hiển thị vùng giá có khả năng đảo chiều, đồng thời kết hợp với sự gia tăng khối lượng thân nến để xác nhận khởi động xu hướng. Do đó, sự kết hợp của chúng có thể nâng cao tỷ lệ thành công giao dịch. Cụ thể, chiến lược sẽ mở vị thế mua hoặc bán trong các trường hợp sau:

- Chỉ báo TMO xuất hiện tín hiệu mua, tức là giá phân kỳ hướng lên VÀ chỉ báo AMA xuất hiện giá trị cực đại mua.

- Chỉ báo TMO xuất hiện tín hiệu bán, tức là giá phân kỳ hướng xuống VÀ chỉ báo AMA xuất hiện giá trị cực tiểu bán.

- Đồng thời yêu cầu khối lượng thân nến của 3 nến gần nhất ngày càng lớn.

Như vậy, nó giải quyết vấn đề tín hiệu giả do một chỉ báo đơn lẻ gây ra. Phương pháp cắt lỗ chọn mức giá cao nhất và thấp nhất trong N nến gần nhất, có thể kiểm soát rủi ro khá tốt.

Ưu điểm của chiến lược

Chiến lược này có những ưu điểm sau:

-

Kết hợp chỉ báo, nâng cao độ chính xác của tín hiệu. Chỉ báo TMO và AMA xác nhận lẫn nhau, giảm tín hiệu giả, từ đó nâng cao độ chính xác của tín hiệu.

-

Kết hợp nhiều điều kiện, nắm bắt thời điểm bắt đầu xu hướng. Các điều kiện như tín hiệu chỉ báo TMO, điểm cực trị của AMA và sự gia tăng khối lượng thân nến giúp nắm bắt hiệu quả thời điểm bắt đầu xu hướng, đây là mục tiêu mà chiến lược Scalping hướng tới.

-

Phương pháp cắt lỗ dựa trên nến giúp kiểm soát rủi ro. Sử dụng mức giá cao nhất và thấp nhất gần đây của nến làm điểm cắt lỗ có thể kiểm soát tốt rủi ro cho mỗi lệnh, đồng thời tránh được rủi ro đảo chiều do độ trễ khi chỉ báo tính toán lại.

-

Logic giao dịch đơn giản và hiệu quả. Chiến lược này chỉ sử dụng hai chỉ báo để thực hiện một chiến lược Scalping khá hoàn chỉnh, không quá phức tạp, logic rõ ràng. Và từ kết quả ví dụ, chiến lược đã đạt được lợi nhuận tốt.

Rủi ro của chiến lược

Chiến lược này chủ yếu tồn tại các rủi ro sau:

-

Rủi ro vào lệnh và thoát lệnh thường xuyên. Là chiến lược Scalping, thời gian nắm giữ không dài, nếu chi phí giao dịch cao sẽ ảnh hưởng nhất định đến lợi nhuận.

-

Rủi ro cắt lỗ quá mạnh. Sử dụng mức giá cao nhất và thấp nhất gần đây làm điểm cắt lỗ có thể khá mạnh tay, không thể lọc nhiễu thị trường hoàn toàn, làm tăng xác suất kích hoạt cắt lỗ.

-

Rủi ro khó tối ưu tham số. Chiến lược liên quan đến nhiều tham số, việc tìm ra bộ tham số tối ưu có thể khá khó khăn.

Hướng tối ưu hóa

Chiến lược này có thể được tối ưu hóa theo các hướng sau:

-

Thêm các chỉ báo lọc bổ sung, như khối lượng giao dịch thị trường, có thể lọc bỏ một số tín hiệu giả, nâng cao chất lượng tín hiệu.

-

Thử thêm điều kiện lọc vào phương pháp cắt lỗ, tránh cắt lỗ quá mạnh. Ví dụ, chờ xác nhận thêm vài nến trước khi kích hoạt cắt lỗ.

-

Tiến hành tối ưu hóa tham số, tìm ra tổ hợp tham số tối ưu cho chỉ báo. Điều này có thể lọc thêm nhiễu, nâng cao tỷ lệ thắng của chiến lược. Cần tối ưu chủ yếu các tham số như độ dài chỉ báo TMO, độ dài chỉ báo AMA và hệ số nhân.

-

Thử nghiệm backtest và giao dịch thực trên các sản phẩm và khung thời gian khác nhau, tìm ra sản phẩm và khung thời gian phù hợp nhất với logic chiến lược này.

Tổng kết

Chiến lược này kết hợp tín hiệu giao dịch của chỉ báo TMO và AMA, tìm kiếm thời điểm bắt đầu xu hướng trong thị trường dao động để thực hiện giao dịch Scalping. Nó có ưu điểm về độ chính xác tín hiệu cao, nắm bắt sớm xu hướng và kiểm soát rủi ro. Sau khi tối ưu hóa thêm về tham số và quy tắc, chiến lược này có thể trở thành chiến lược Scalping trong ngày có giá trị thực tiễn cao.

- 1