Chiến lược dừng lỗ theo xu hướng dựa trên TFO và ATR

Tổng quan

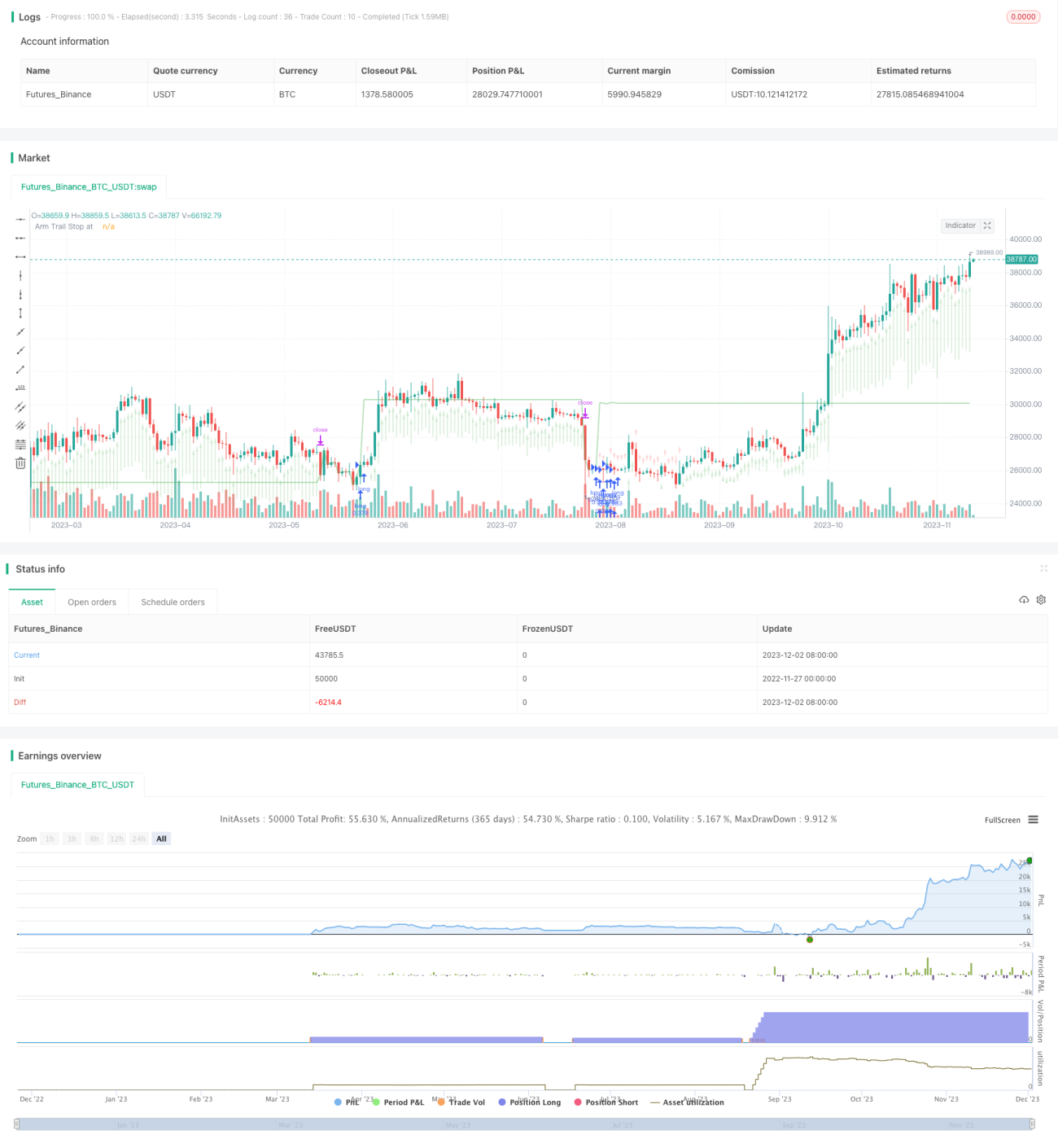

Chiến lược này được thiết kế dựa trên chỉ báo Trend Flex Oscillator (TFO) của Tiến sĩ John Ehlers và chỉ báo Average True Range (ATR), tạo thành một chiến lược trailing stop theo xu hướng. Nó phù hợp với thị trường tăng giá, mở vị thế mua khi giá đảo chiều sau trạng thái quá bán. Thông thường, vị thế sẽ được đóng trong vòng vài ngày, trừ khi bị thị trường gấu bắt giữ, khi đó nó sẽ giữ vững vị thế. Chiến lược này điều chỉnh các tham số có thể cấu hình thông qua backtest đơn giản, nhưng không nên hoàn toàn tin tưởng vào kết quả backtest.

Nguyên lý chiến lược

Chiến lược kết hợp hai chỉ báo TFO và ATR, mở vị thế mua khi điều kiện mua được thỏa mãn, và đóng vị thế khi điều kiện bán được thỏa mãn.

Điều kiện mua: Khi TFO dưới một ngưỡng nhất định (cho thấy quá bán), và giá trị TFO của nến trước đó thấp hơn nến hiện tại (cho thấy TFO đảo chiều tăng), đồng thời ATR cao hơn ngưỡng biến động đã thiết lập (cho thấy thị trường biến động gia tăng), thỏa mãn cả ba điều kiện thì mở vị thế mua.

Điều kiện bán: Khi TFO cao hơn một ngưỡng nhất định (cho thấy quá mua), đồng thời ATR cao hơn ngưỡng đã thiết lập, thỏa mãn điều kiện thì đóng tất cả các vị thế mua. Ngoài ra, chiến lược còn thiết lập trailing stop: khi giá phá vỡ mức trailing stop đã đặt, tất cả các vị thế mua cũng sẽ bị đóng. Người dùng có thể chọn để chiến lược đóng vị thế dựa trên tín hiệu chỉ báo hoặc chỉ đóng theo mức stop.

Chiến lược này có thể mở tối đa 15 vị thế mua cùng lúc. Các tham số có thể điều chỉnh, phù hợp với nhiều khung thời gian khác nhau.

Ưu điểm của chiến lược

-

Kết hợp xu hướng và biến động để đánh giá hướng thị trường, khá ổn định. TFO có thể nắm bắt tín hiệu sớm của sự bứt phá xu hướng, ATR nắm bắt thời điểm biến động thị trường gia tăng.

-

Thiết lập các tham số mua bán và stop có thể điều chỉnh, linh hoạt trong thao tác. Người dùng có thể điều chỉnh tham số theo thị trường để tối ưu hóa.

-

Tích hợp chức năng stop, có thể giảm thiểu tổn thất trong các đợt biến động cực đoan. Stop loss là một phần rất quan trọng trong giao dịch định lượng.

-

Hỗ trợ mở thêm vị thế và đóng một phần, có thể khuếch đại lợi nhuận bằng cách tăng quy mô vị thế. Phù hợp với thị trường tăng giá.

Rủi ro của chiến lược

-

Chiến lược chỉ mua, không bán khống, không thể kiếm lợi nhuận trong thị trường giảm. Nếu gặp thị trường gấu thảm khốc, có thể gây tổn thất lớn.

-

Thiết lập tham số không phù hợp có thể dẫn đến giao dịch quá mức hoặc bỏ lỡ mua/bán. Cần kiểm tra nhiều lần để tìm bộ tham số tối ưu.

-

Trong các điều kiện thị trường cực đoan, stop loss có thể không hiệu quả, không ngăn chặn được tổn thất lớn. Đây là vấn đề mà tất cả các chiến lược stop đều có thể gặp phải.

-

Backtest không thể phản ánh hoàn toàn tình hình giao dịch thực tế, kết quả thực tế sẽ có độ lệch nhất định.

Tối ưu hóa chiến lược

-

Có thể cân nhắc thêm đường trailing stop vào điều kiện bán, giúp chiến lược kịp thời cắt lỗ, kiểm soát hiệu quả rủi ro giảm.

-

Có thể mở rộng cơ chế bán khống, mở vị thế bán khi TFO đảo chiều giảm và ATR đủ lớn, giúp chiến lược thích ứng với thị trường giảm.

-

Có thể thêm nhiều bộ lọc hơn, ví dụ như thay đổi khối lượng giao dịch, giảm tác động của các phiên giao dịch bất thường lên chiến lược.

-

Có thể kiểm tra các thiết lập tham số và kết quả backtest trên các khung thời gian khác nhau, tìm ra khung thời gian và tổ hợp tham số tối ưu.

Tổng kết

Chiến lược này kết hợp ưu điểm của phân tích xu hướng và đo lường biến động, xác định hướng thị trường thông qua tổ hợp chỉ báo TFO và ATR; thiết lập các cơ chế như mở thêm vị thế, đóng một phần, trailing stop, có thể khuếch đại lợi nhuận và kiểm soát rủi ro, phù hợp với thị trường tăng giá; còn có không gian tối ưu hóa có thể mở rộng, thông qua việc thêm nhiều bộ lọc chỉ báo và tinh chỉnh tham số có thể cải thiện thêm hiệu suất của chiến lược. Về cơ bản, nó đáp ứng các yêu cầu chức năng cơ bản của một chiến lược định lượng, đáng để nghiên cứu và ứng dụng sâu hơn.

/*backtest

start: 2022-11-27 00:00:00

end: 2023-12-03 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Chart0bserver

//

// Open Source attributions:- 1