Chiến lược giao dịch biến động tự thích nghi dựa trên sự phá vỡ giá

1

Follow

1802

Followers

Tổng quan

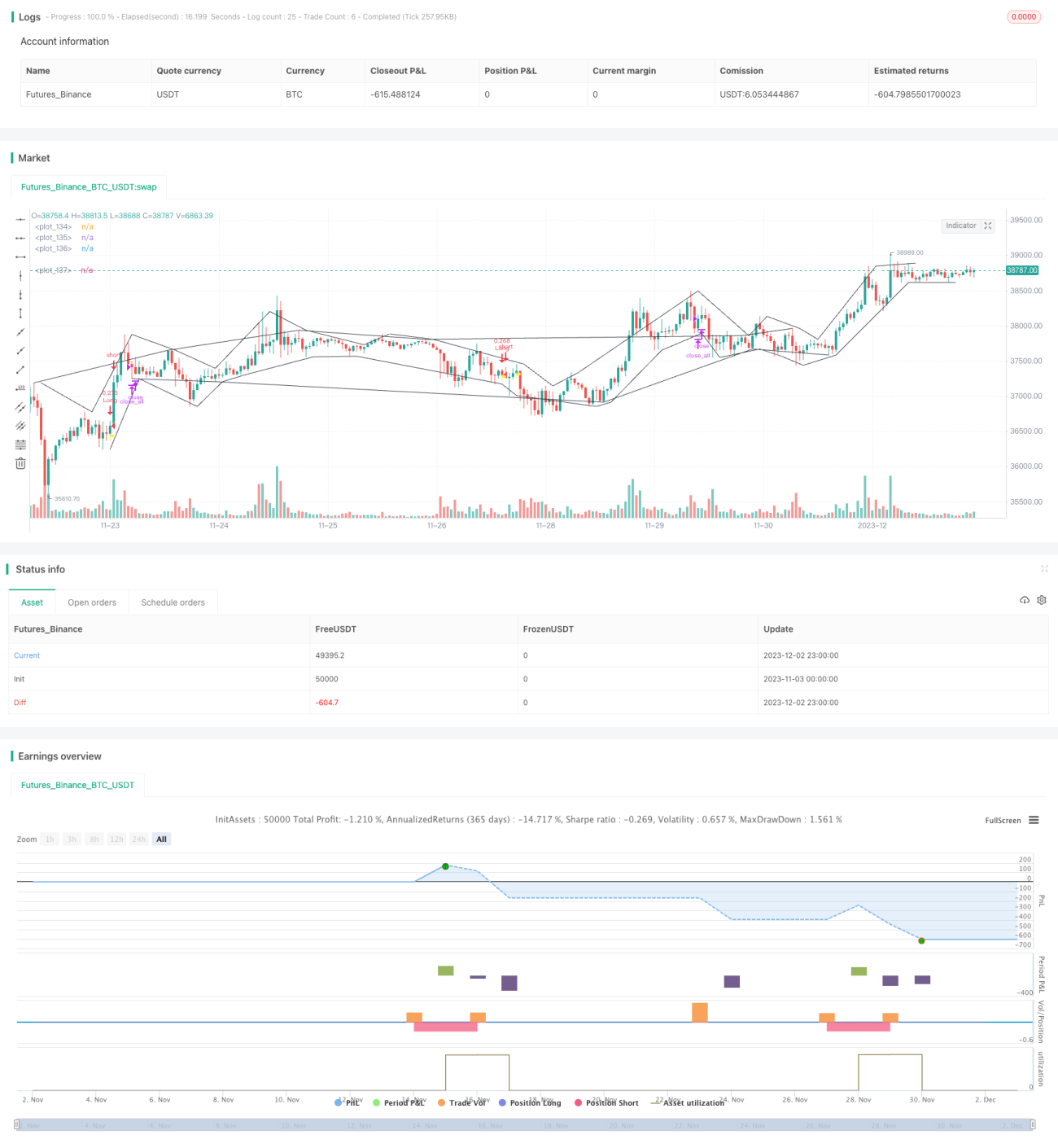

Chiến lược này dựa trên các điểm phá vỡ giá để nhận diện xu hướng thị trường, kết hợp với chỉ báo thích ứng để đánh giá xu hướng lớn, nhằm nắm bắt các cơ hội đảo chiều giá ngắn hạn. Khi giá phá vỡ khỏi kênh đột phá từ đường cơ sở, tín hiệu mua/bán được tạo ra. Chiến lược này phù hợp với giao dịch tiền điện tử có biến động cao.

Nguyên lý chiến lược

- Xác định các điểm cực trị của giá làm ranh giới kênh. Khi giá tạo đỉnh mới hoặc đáy mới, điểm đó được coi là ranh giới kênh.

- Tính chỉ báo biến động thích ứng MA để xác định hướng xu hướng tổng thể. Giá trị MA càng lớn cho thấy thị trường đang ở giai đoạn dao động.

- Khi giá phá vỡ lên phía trên đường trên của kênh, tín hiệu mua được tạo ra; khi giá phá vỡ xuống phía dưới đường dưới của kênh, tín hiệu bán được tạo ra.

- Đặt điểm dừng lỗ. Điểm dừng lỗ cho vị thế long được đặt ở mức 1% giá vào lệnh.

Phân tích ưu điểm

- Kênh giá có tính thích ứng, có thể xác định chính xác các điểm đảo chiều xu hướng.

- Chỉ báo biến động đánh giá xu hướng lớn, tránh bỏ lỡ hướng đi chính trong xu hướng dao động.

- Chiến lược đảo chiều, phù hợp để nắm bắt các đợt bật lại giá ngắn hạn.

Phân tích rủi ro

- Trong các đợt giảm mạnh liên tục, dễ kích hoạt nhiều điểm dừng lỗ, gây thua lỗ lớn.

- Trong giai đoạn dao động đi ngang, việc mua bán thường xuyên làm tăng chi phí giao dịch.

- Cần xác định thời điểm vào lệnh thủ công, giao dịch tự động hoàn toàn có rủi ro quá khớp.

Hướng tối ưu

- Tối ưu tham số của MA để đánh giá xu hướng tổng thể tốt hơn.

- Thêm chỉ báo khối lượng để tránh các tín hiệu đảo chiều khi khối lượng suy yếu.

- Thêm mô hình học máy để tối ưu động các tham số.

Tổng kết

Chiến lược này có tư duy tổng thể rõ ràng, mang giá trị thực tiễn nhất định. Tuy nhiên, vẫn cần chú ý kiểm soát rủi ro giao dịch, tránh gây thua lỗ lớn trong các điều kiện thị trường đặc biệt. Bước tiếp theo có thể tối ưu từ nhiều khía cạnh như khung tổng thể, tham số chỉ báo, kiểm soát rủi ro, giúp các tham số chiến lược và tín hiệu giao dịch trở nên đáng tin cậy hơn.

Source

Pine

/*backtest

start: 2023-11-03 00:00:00

end: 2023-12-03 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// @version = 4

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © TradingGroundhog

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1