Chiến lược đảo chiều RSI đa nhân tố

Tổng quan

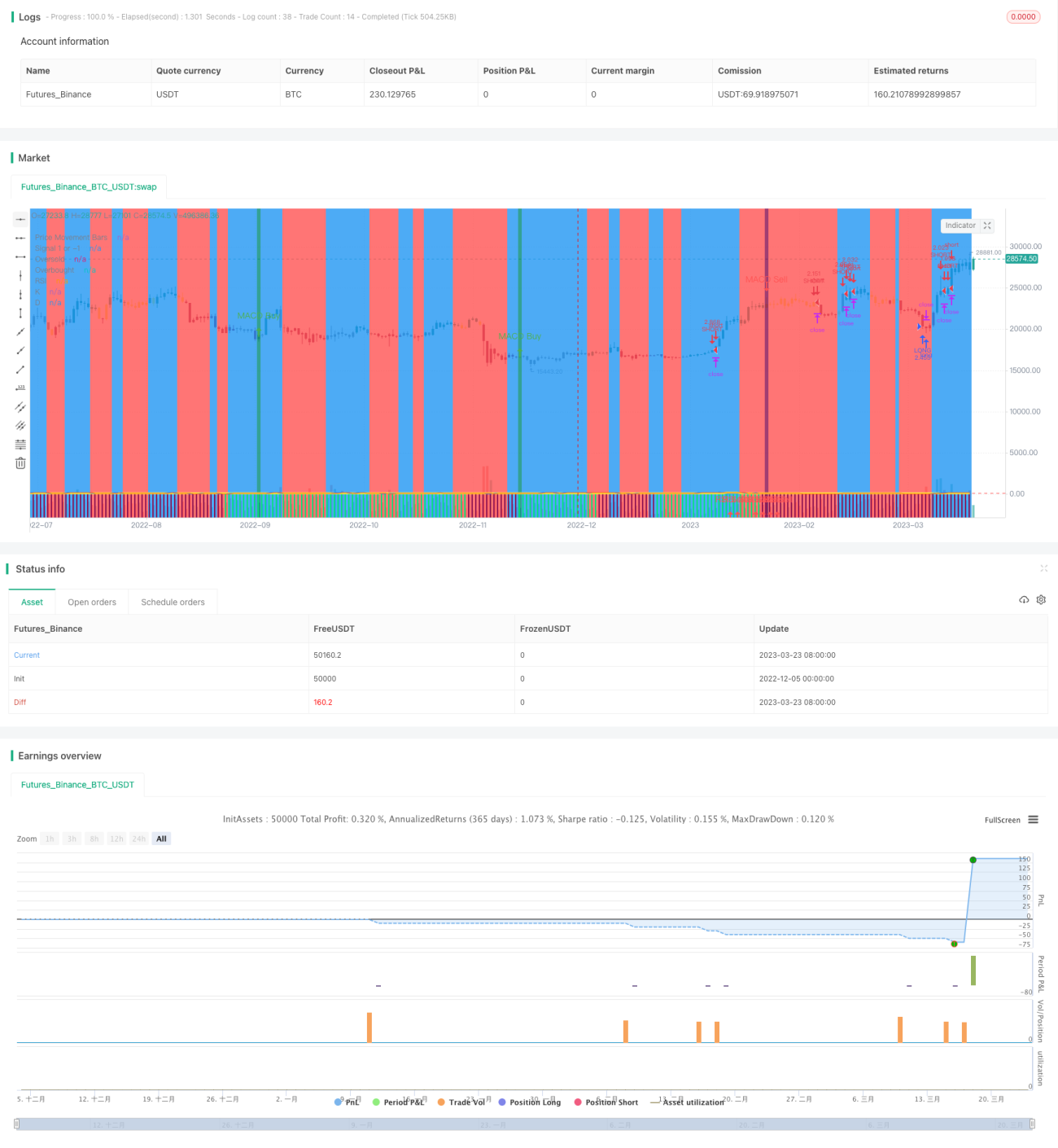

Chiến lược này sử dụng chỉ báo RSI để nhận diện tình trạng quá mua/quá bán, kết hợp với nhiều yếu tố phụ trợ như MACD, Stochastic để vào lệnh. Chiến lược nhằm mục đích nắm bắt các cơ hội đảo chiều ngắn hạn, thuộc loại chiến lược đảo chiều.

Nguyên lý chiến lược

Chiến lược này chủ yếu sử dụng chỉ báo RSI để xác định thị trường đang ở trạng thái quá mua hay quá bán. Khi chỉ báo RSI vượt qua đường quá mua đã thiết lập, cho thấy thị trường có thể đang ở trạng thái quá mua, lúc này chiến lược chọn bán khống; khi chỉ báo RSI xuống dưới đường quá bán đã thiết lập, cho thấy thị trường có khả năng đang ở trạng thái quá bán, chiến lược lúc này chọn mua vào. Bằng cách này, chiến lược kiếm lợi nhuận từ các cơ hội giao dịch ngắn hạn phát sinh trong quá trình đảo chiều khi thị trường chuyển từ trạng thái cực đoan này sang trạng thái cực đoan khác.

Ngoài ra, chiến lược còn đưa vào nhiều yếu tố phụ trợ như MACD, Stochastic. Vai trò của các yếu tố phụ trợ này là lọc bỏ một số tín hiệu giao dịch sai lệch có thể xảy ra. Chỉ khi chỉ báo RSI phát tín hiệu và các yếu tố phụ trợ cũng ủng hộ tín hiệu đó, chiến lược mới thực hiện hành động giao dịch thực sự. Phương thức kết hợp đa yếu tố này có thể nâng cao độ tin cậy của tín hiệu chiến lược, từ đó cũng tăng tính ổn định của chiến lược.

Phân tích ưu điểm

Ưu điểm lớn nhất của chiến lược này là hiệu quả nắm bắt cao, thực hiện xác thực đa yếu tố để cải thiện chất lượng tín hiệu. Cụ thể thể hiện ở các khía cạnh sau:

- Bản thân chỉ báo RSI có khả năng nhận diện chế độ thị trường mạnh mẽ, có thể nhận diện hiệu quả hiện tượng quá mua/quá bán.

- Nhờ sự trợ giúp của nhiều công cụ phụ trợ để xác thực đa yếu tố, nâng cao chất lượng tín hiệu, lọc bỏ nhiều tín hiệu sai lệch.

- Chiến lược không nhạy cảm với tham số, dễ tối ưu hóa.

Rủi ro và giải pháp

Chiến lược này cũng đối mặt với một số rủi ro nhất định, tập trung ở hai khía cạnh:

- Rủi ro đảo chiều thất bại. Bản thân tín hiệu đảo chiều dựa trên cơ hội chênh lệch thống kê, không loại trừ khả năng thất bại của một số đảo chiều. Có thể kiểm soát rủi ro bằng cách giảm vị thế hoặc đặt lệnh dừng lỗ.

- Rủi ro thua lỗ trong xu hướng tăng. Nhìn chung, chiến lược vẫn thiên về giao dịch ngược xu hướng, trong xu hướng tăng khó tránh khỏi thua lỗ nhất định. Điều này đòi hỏi chúng ta phải đánh giá chính xác xu hướng lớn, khi cần thiết có thể can thiệp thủ công để bỏ qua các điều kiện thị trường bất lợi.

Hướng tối ưu hóa

Chiến lược này cần được tối ưu hóa từ các khía cạnh sau:

- Thử nghiệm trên các sản phẩm khác nhau để tìm bộ tham số tối ưu. Chiến lược không nhạy cảm với tham số, nhưng vẫn khuyến nghị tìm tham số tối ưu cho từng sản phẩm.

- Thêm cơ chế thoát lệnh thích ứng. Có thể thử nghiệm thêm dừng lỗ động, thoát lệnh theo thời gian, v.v., để chiến lược thích nghi hơn với sự thay đổi của thị trường.

- Đưa thuật toán học máy vào. Có thể thử nghiệm để mô hình học cách đánh giá xác suất đảo chiều thành công, từ đó nâng cao tỷ lệ thắng của chiến lược.

Tổng kết

Nhìn chung, chiến lược này là một chiến lược đảo chiều ngắn hạn. Sử dụng khả năng nhận diện quá mua/quá bán của chỉ báo RSI, đồng thời nhờ sự trợ giúp của nhiều công cụ phụ trợ để xác thực đa yếu tố, từ đó nâng cao chất lượng tín hiệu. Chiến lược này có hiệu quả nắm bắt cao, tính ổn định cũng khá tốt. Đáng để thử nghiệm và tối ưu hóa thêm, cuối cùng đạt được lợi nhuận.

/*backtest

start: 2022-12-05 00:00:00

end: 2023-03-24 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=4

strategy(shorttitle='Ain1',title='All in One Strategy', overlay=true, initial_capital = 1000, process_orders_on_close=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, commission_type=strategy.commission.percent, commission_value=0.18, calc_on_every_tick=true)- 1