Chiến lược định lượng đường quấn phân tâm hàng ngày

Tổng quan

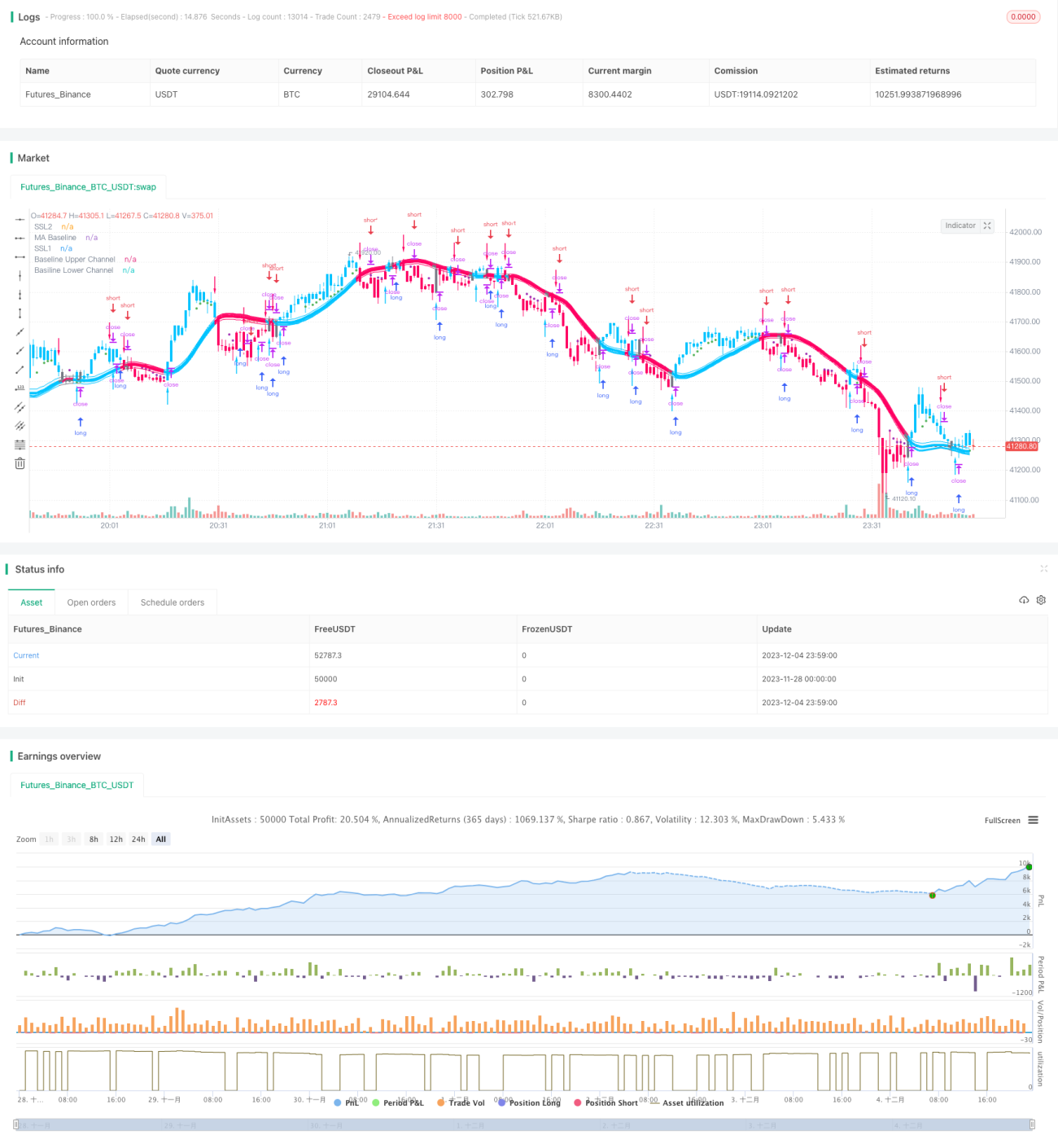

Chiến lược giao dịch định lượng Đường phân tâm quấn quanh hàng ngày là một chiến lược giao dịch ngắn hạn dựa trên đường trung bình động và chỉ số giá cao nhất/thấp nhất. Nó sử dụng mũi tên EXIT của chỉ số hỗn hợp SSL để xác định điểm mua/bán, kết hợp với chỉ số QQE để lọc tín hiệu, và dùng chỉ số ATR để tính toán mức dừng lỗ cũng như các mức thêm vị thế theo đợt. Chiến lược này phù hợp với các nhà đầu tư nhạy cảm với biến động thị trường và yêu cầu kiểm soát rủi ro chặt chẽ.

Nguyên lý chiến lược

Chiến lược sử dụng mũi tên EXIT của chỉ số hỗn hợp SSL để xác định điểm vào lệnh mua/bán. Phía trên mũi tên EXIT là điểm cao EXIT, phía dưới là điểm thấp EXIT. Khi giá đóng cửa cắt xuống từ điểm cao EXIT sẽ phát sinh tín hiệu bán, khi giá đóng cửa cắt lên từ điểm thấp EXIT sẽ phát sinh tín hiệu mua.

Để tăng độ tin cậy của tín hiệu, chiến lược đưa vào chỉ số QQE như một điều kiện lọc phụ trợ. Tín hiệu từ mũi tên EXIT chỉ được thực hiện khi chỉ số QQE cùng hướng.

Để kiểm soát rủi ro, chiến lược sử dụng chỉ số ATR theo bội số để tính mức dừng lỗ và các mức thêm vị thế theo đợt. Dừng lỗ vị thế bán là giá đóng cửa + ATR × 1,8; dừng lỗ vị thế mua là giá đóng cửa – ATR × 1,8. Thêm vị thế làm ba đợt, mỗi đợt có số tiền thêm bằng 10% số tiền ban đầu. Các mức thêm vị thế lần lượt là giá đóng cửa – ATR × 0,1; giá đóng cửa – ATR × 0,3 và giá đóng cửa – ATR × 0,7.

Mỗi đợt thêm vị thế có mức dừng lỗ riêng. 20% khối lượng vị thế của đợt đầu tiên sẽ bị dừng lỗ khi chạm mức dừng, phần còn lại tiếp tục nắm giữ.

Ưu điểm của chiến lược

- Tận dụng mũi tên EXIT để chốt lời, dừng lỗ kịp thời, kiểm soát rủi ro hiệu quả.

- Bộ lọc chỉ số QQE giúp tăng độ chính xác của tín hiệu.

- Sử dụng chỉ số ATR để tính toán mức dừng lỗ và thêm vị thế dựa trên biến động thị trường, kiểm soát rủi ro chính xác hơn.

- Thêm vị thế theo đợt, tận dụng xu hướng để thu lợi nhuận.

Rủi ro của chiến lược

- Vị thế có lãi bị dừng lỗ một phần có thể khiến phần vị thế còn lại đối mặt với rủi ro tiếp tục bị dừng lỗ. Có thể xem xét chốt lời tổng thể hoặc chốt lời dựa trên các chỉ số cơ bản của bản thân cổ phiếu.

- Mức độ nhạy cảm với biến động thị trường của mũi tên EXIT và chỉ số QQE khác nhau, có thể phát sinh tín hiệu mâu thuẫn, cần điều chỉnh tham số để giảm xung đột tín hiệu.

- Thêm vị thế quá mức có thể dẫn đến mua đỉnh bán đáy. Cần đánh giá tình hình, giảm mức đòn bẩy.

Hướng tối ưu

- Kết hợp các chỉ số cơ bản của bản thân cổ phiếu để chốt lời, ví dụ đặt mức chốt lời hợp lý dựa trên tỷ lệ giá trị sổ sách, tỷ lệ P/E, tỷ suất cổ tức, v.v.

- Điều chỉnh tham số của chỉ số QQE để đồng nhất với tín hiệu từ mũi tên EXIT.

- Giảm tỷ lệ thêm vị thế theo mức độ nóng của thị trường, giảm thêm vị thế trong giai đoạn thị trường dao động.

- Kiểm tra tổ hợp tham số tối ưu dựa trên các chỉ số như mức sụt giảm tối đa, tỷ lệ lợi nhuận/rủi ro.

Tổng kết

Chiến lược này lấy mũi tên EXIT của chỉ số hỗn hợp SSL làm tín hiệu cốt lõi, sử dụng chỉ số QQE và ATR để lọc và dừng lỗ. Thông qua việc thêm vị thế theo đợt giúp khuếch đại lợi nhuận. Đây là chiến lược giao dịch ngắn hạn định lượng, phù hợp để theo dõi xu hướng ngắn hạn của thị trường. Chiến lược có khả năng kiểm soát sụt giảm và rủi ro, nhưng cũng cần chú ý phòng tránh các rủi ro như xung đột tín hiệu, mua đỉnh bán đáy. Nếu có thể kết hợp phương pháp chốt lời dựa trên các yếu tố cơ bản của cổ phiếu, đồng thời thận trọng hơn trong việc đánh giá dao động thị trường và điều chỉnh tỷ lệ thêm vị thế, thì không gian lợi nhuận của chiến lược sẽ lớn hơn.

- 1