Chiến lược định lượng dựa trên tỷ lệ thay đổi giá và đường trung bình động

Tổng quan

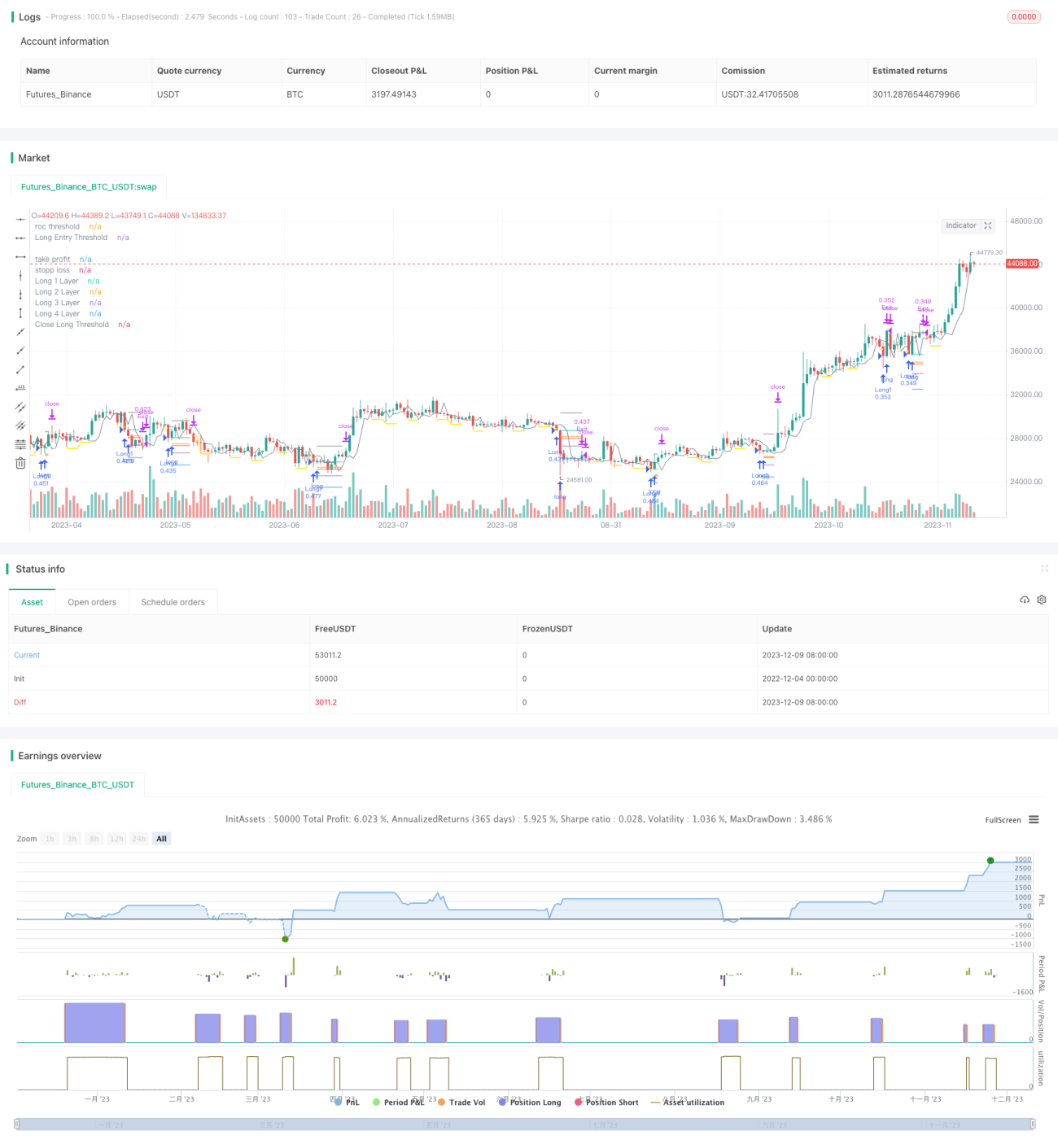

Chiến lược này kết hợp các chỉ báo kỹ thuật về tốc độ thay đổi giá (ROC) và đường trung bình động để xác định chính xác điểm mua và điểm bán. Khi giá giảm rõ rệt, thiết lập ngưỡng mua, và khi giảm sâu hơn thì mở vị thế long; khi giá tăng, thiết lập ngưỡng bán, và khi tăng tiếp thì đóng vị thế. Đồng thời, chiến lược còn áp dụng phương pháp tăng vốn, mua nhiều lần để giảm chi phí.

Nguyên lý chiến lược

Logic mua

- Tính toán tốc độ thay đổi giá (ROC) và thiết lập đường ngưỡng mua.

- Khi giá phá vỡ đường ngưỡng mua, ghi nhận điểm đó và kích hoạt đường giới hạn mua.

- Đường giới hạn mua được thiết lập thời gian tồn tại dựa trên tham số đầu vào, hết hạn thì đóng.

- Khi giá tiếp tục giảm và phá vỡ đường giới hạn mua, mở vị thế long đầu tiên.

Logic bán

- Tính toán tốc độ thay đổi giá (ROC) và thiết lập đường ngưỡng bán.

- Khi giá vượt lên trên đường ngưỡng bán, ghi nhận điểm đó và kích hoạt đường giới hạn bán.

- Đường giới hạn bán được thiết lập thời gian tồn tại dựa trên tham số đầu vào, hết hạn thì đóng.

- Khi giá tiếp tục tăng và vượt lên trên đường giới hạn bán, đóng toàn bộ vị thế long.

Kiểm soát rủi ro

Chiến lược tích hợp chức năng cắt lỗ và chốt lời, có thể tùy chỉnh tham số để kiểm soát rủi ro của vị thế hiện tại theo thời gian thực.

Phương pháp tăng vốn

Mỗi khi mở một vị thế giao dịch, giá mua tiếp theo được thiết lập theo một tỷ lệ nhất định dựa trên tham số đầu vào, nhằm đạt hiệu quả mua nhiều đợt và tăng vốn.

Phân tích ưu điểm

- Sử dụng chỉ báo tốc độ thay đổi giá ROC để tìm điểm mua bán; ROC rất nhạy cảm với biến động giá, xác định điểm mua bán chính xác.

- Sử dụng phương pháp đường giới hạn để xác nhận thêm thời điểm mua bán, tránh phá vỡ giả.

- Phương pháp tăng vốn có thể theo dõi giá trị thị trường dựa trên cơ sở kiểm soát rủi ro.

- Tích hợp chức năng cắt lỗ chốt lời để kiểm soát chặt chẽ rủi ro từng vị thế.

Rủi ro và giải pháp

- Khi thị trường biến động mạnh, chiến lược có thể mở quá nhiều vị thế. Giải pháp: đặt tham số tăng vốn hợp lý, kiểm soát tổng số vị thế.

- Khi xu hướng giá dao động không rõ ràng, giá cắt lỗ hoặc chốt lời có thể bị kích hoạt thường xuyên. Có thể nới lỏng biên độ cắt lỗ/chốt lời hoặc tắt chức năng này.

Đề xuất tối ưu

- Kết hợp các chỉ báo khác để lọc thời điểm vào lệnh. Ví dụ: kết hợp với đường trung bình động, chỉ chấp nhận tín hiệu ROC khi giá phá vỡ đường trung bình động.

- Tối ưu hóa logic tăng vốn, chỉ kích hoạt tăng vốn khi thỏa mãn điều kiện nhất định. Ví dụ: chỉ tiếp tục tăng vốn khi giá giảm thêm vượt quá một mức nhất định.

- Cài đặt tham số cho các sản phẩm khác nhau có sự khác biệt lớn, cần backtest đầy đủ và mô phỏng thực tế để có được bộ tham số tối ưu.

- Có thể thiết lập cắt lỗ/chốt lời thích ứng, điều chỉnh biên độ cắt lỗ khác nhau dựa trên mức độ biến động thị trường.

Tổng kết

Chiến lược này sử dụng tổng hợp chỉ báo ROC để xác định chính xác điểm mua bán, phương pháp đường giới hạn lọc tín hiệu, tích hợp cắt lỗ chốt lời để phòng ngừa rủi ro, và mở rộng lợi nhuận thông qua tăng vốn. Với cài đặt tham số hợp lý, có thể đạt được lợi nhuận vượt trội trong khi đảm bảo rủi ro trong tầm kiểm soát. Trong tương lai, có thể tối ưu hóa thêm cơ chế lọc tín hiệu và kiểm soát rủi ro để chiến lược thích ứng với nhiều môi trường thị trường hơn.

- 1