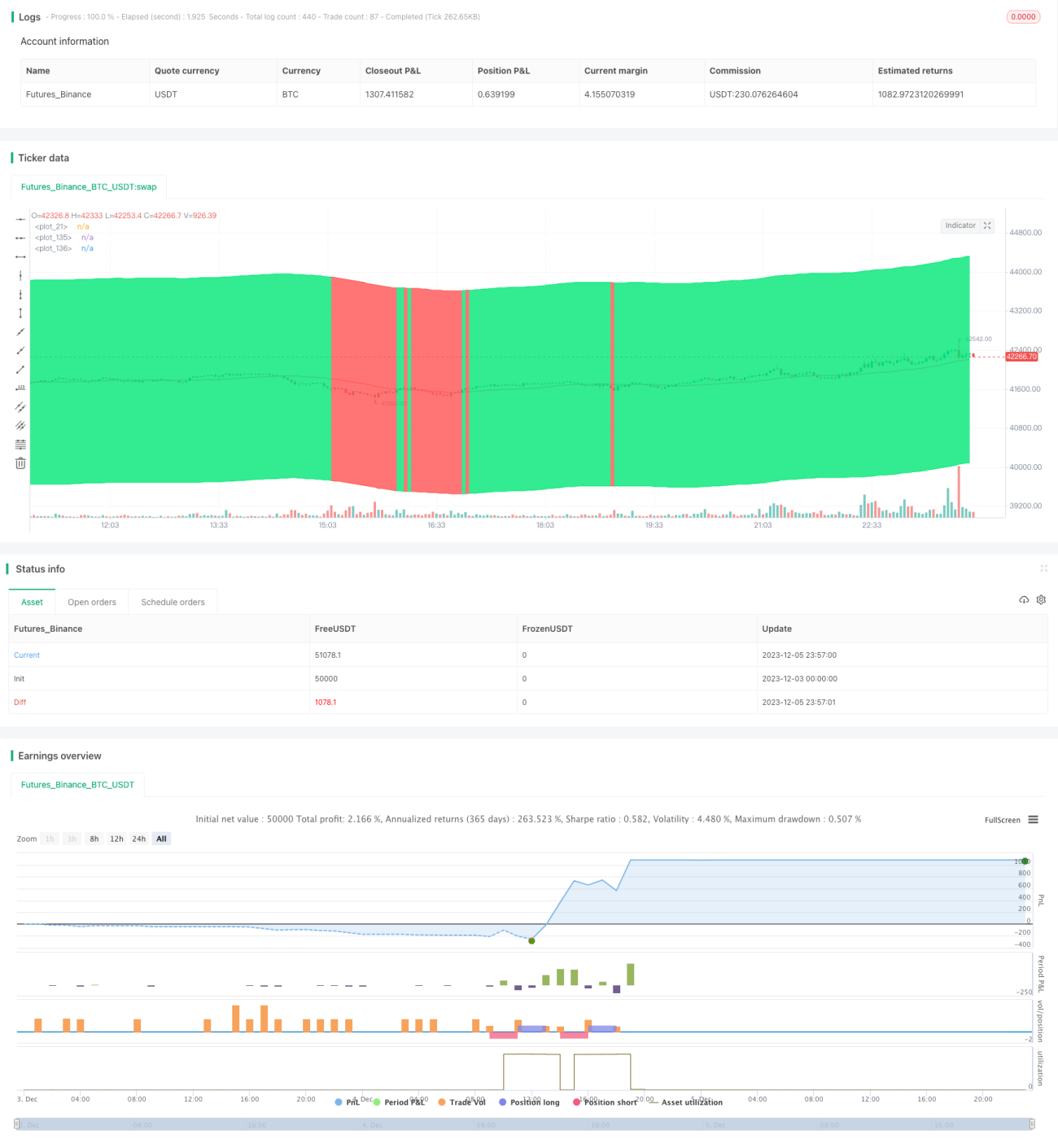

Chiến lược theo dõi xu hướng động

Tổng quan

Ý tưởng chính của chiến lược này là theo dõi động xu hướng thị trường, mua khi xu hướng tăng và bán khi xu hướng giảm. Nó xác định hướng xu hướng bằng cách tính toán kết hợp nhiều chỉ báo, chẳng hạn như hồi quy tuyến tính, đường trung bình động Hull đã sửa đổi, v.v.

Nguyên lý chiến lược

Chiến lược này sử dụng nhiều chỉ báo kỹ thuật để xác định hướng xu hướng. Đầu tiên, nó tính toán một kênh phạm vi, ranh giới trên và dưới được tính dựa trên đường trung bình động đơn giản của close và một tham số đầu vào. Sau đó, nó tính toán đường trung bình động Hull đã sửa đổi, chỉ báo này được cho là có khả năng mô tả xu hướng chính xác hơn. Ngoài ra, nó còn tính toán chỉ báo hồi quy tuyến tính. Khi đường trung bình động Hull đã sửa đổi cắt lên trên đường hồi quy tuyến tính, nó tạo ra tín hiệu mua; khi cắt xuống dưới, nó tạo ra tín hiệu bán. Bằng cách này, có thể theo dõi động sự thay đổi của xu hướng.

Để giảm tín hiệu sai, chiến lược này còn thiết kế nhiều bộ lọc. Ví dụ, sử dụng EMA để xác định xem có đang ở xu hướng giảm hay không, và sử dụng một chỉ báo cửa sổ để theo dõi sự thay đổi của RSI. Các bộ lọc này có thể tránh phát sinh tín hiệu giao dịch trong thị trường dao động.

Về điểm vào lệnh và cắt lỗ, chiến lược này ghi nhận giá mở cửa cuối cùng và đặt tỷ lệ chốt lời và cắt lỗ. Ví dụ, nếu giá mua cuối cùng là 100 đô la, thì đặt mục tiêu chốt lời là 102 đô la và giá cắt lỗ là 95 đô la. Điều này cho phép theo dõi động.

Phân tích ưu điểm

Chiến lược này có những ưu điểm sau:

- Theo dõi động sự thay đổi xu hướng, có thể nắm bắt tốt hướng đi dài hạn;

- Sử dụng nhiều bộ lọc, giúp giảm nhiễu, tránh giao dịch thường xuyên trong thị trường dao động;

- Tự động điều chỉnh vị trí chốt lời và cắt lỗ, thực hiện theo dõi xu hướng;

- Có thể tự động tìm ra bộ tham số tối ưu thông qua tối ưu hóa tham số.

Phân tích rủi ro

Chiến lược này cũng tồn tại một số rủi ro:

- Vẫn không thể hoàn toàn tránh được rủi ro bị mắc kẹt trong thị trường. Khi xu hướng đảo chiều, có thể đối mặt với lỗ thả nổi lớn.

- Cài đặt tham số không phù hợp có thể khiến chiến lược hoạt động kém. Cần tìm ra bộ tham số tối ưu thông qua tối ưu hóa.

- Thời gian xử lý dữ liệu quá lâu có thể dẫn đến tín hiệu bị trễ. Cần tối ưu hóa tính toán chỉ báo để càng gần thời gian thực càng tốt.

Để kiểm soát rủi ro, có thể đặt cắt lỗ, trailing stop hoặc sử dụng quyền chọn để khóa lợi nhuận. Ngoài ra, phải kiểm tra lặp đi lặp lại các bộ tham số, tìm ra phạm vi tham số đáng tin cậy. Cuối cùng, cũng cần chú ý đến thời gian tính toán chỉ báo, luôn hướng tới tính thời gian thực của tín hiệu.

Hướng tối ưu hóa

Chiến lược này có thể được tối ưu hóa từ các khía cạnh sau:

- Thử nghiệm kết hợp nhiều chỉ báo hơn, tìm ra cách xác định xu hướng đáng tin cậy hơn;

- Điều chỉnh phạm vi tham số, tìm ra tham số tối ưu;

- Tối ưu hóa bộ lọc tín hiệu, tìm ra điểm cân bằng giữa việc loại bỏ nhiễu và độ trễ;

- Thử nghiệm các phương pháp như học máy để tự động sinh ra các quy tắc giao dịch.

Trong quá trình tối ưu hóa, cần sử dụng đầy đủ backtest và giao dịch mô phỏng để đánh giá chất lượng tín hiệu và độ ổn định của chiến lược. Chỉ những phương án tối ưu hóa đã được kiểm chứng kỹ lưỡng mới có thể áp dụng vào giao dịch thực tế.

Tổng kết

Nhìn chung, chiến lược này là một chiến lược theo xu hướng khá tốt. Nó sử dụng nhiều chỉ báo để xác định xu hướng, thiết lập bộ lọc để giảm tín hiệu sai, và có thể tự động điều chỉnh chốt lời và cắt lỗ để theo dõi xu hướng. Nếu tham số được thiết lập phù hợp, nó có thể nắm bắt tốt xu hướng trung và dài hạn. Công việc tiếp theo là tìm ra tham số tối ưu và tiếp tục kiểm tra cũng như tối ưu hóa chiến lược.

- 1