Chiến lược theo xu hướng đảo ngược kép

Tổng quan

Đây là một chiến lược theo dõi xu hướng kết hợp với tín hiệu đảo ngược kép. Nó tích hợp 123 chiến lược đảo ngược và chiến lược chỉ số hiệu suất để theo dõi các điểm đảo ngược giá, cho phép đánh giá xu hướng đáng tin cậy hơn.

Nguyên tắc chiến lược

Chiến lược này bao gồm hai chiến lược con:

-

123 Chiến lược đảo ngược

Sử dụng đường K 14 ngày để đánh giá tín hiệu đảo ngược. Các quy tắc cụ thể là:

- Tín hiệu đa đầu: Giá đóng cửa hai ngày trước giảm, giá đóng cửa đường K hiện tại cao hơn giá đóng cửa ngày trước, Stochastic Slow ngày 9 thấp hơn 50

- Tín hiệu không đầu: Giá đóng cửa 2 ngày trước tăng, giá đóng cửa K hiện tại thấp hơn giá đóng cửa ngày trước, Stochastic Fast 9 ngày cao hơn 50

-

Chiến lược chỉ số hiệu suất

Tính toán các đợt tăng/tăng trong 14 ngày qua như là một chỉ số. Quy tắc là:

- Chỉ số hiệu suất> ((0)), tạo ra tín hiệu đa đầu

- Chỉ số hiệu suất <(0), tạo ra tín hiệu không đầu

Tín hiệu cuối cùng là sự kết hợp của hai loại tín hiệu. Đó là tín hiệu đa không gian đồng hướng cần thiết để tạo ra hoạt động mua và bán thực tế.

Điều này có thể lọc một số tiếng ồn và làm cho tín hiệu trở nên đáng tin cậy hơn.

Lợi thế chiến lược

Hệ thống này có những ưu điểm sau:

- Kết hợp hai yếu tố đánh giá, tín hiệu đáng tin cậy hơn

- Có thể lọc hiệu quả tiếng ồn thị trường, tránh các tín hiệu sai

- 123 hình thức cổ điển và thực tế, dễ dàng đánh giá và tái tạo

- Chỉ số hiệu suất có thể đánh giá xu hướng trong tương lai

- Gói tham số linh hoạt, có thể được tối ưu hóa hơn nữa

Rủi ro chiến lược

Chiến lược này cũng có một số rủi ro:

- Có thể bỏ lỡ sự thay đổi đột ngột, không thể nắm bắt được xu hướng

- Sự kết hợp của hai điều kiện dẫn đến tín hiệu kém hơn, có thể ảnh hưởng đến lợi nhuận

- Cần có sự phán đoán đồng hành, dễ bị ảnh hưởng bởi biến động đặc biệt của cổ phiếu

- Các vấn đề về thiết lập tham số có thể gây ra sự lệch tín hiệu

Có thể xem xét tối ưu hóa các khía cạnh sau:

- Điều chỉnh các tham số, chẳng hạn như chiều dài K, chu kỳ Stochastic

- Tối ưu hóa logic phán đoán của tín hiệu kép

- Kết hợp nhiều yếu tố như số lượng giao dịch.

- Tăng hệ thống chống thiệt hại

Tóm tắt

Chiến lược này tích hợp phán đoán đảo ngược kép, có thể phát hiện hiệu quả các điểm biến giá. Mặc dù tín hiệu xảy ra với xác suất thấp hơn, nhưng độ tin cậy cao, phù hợp để bắt được xu hướng đường dài trung bình. Có thể tăng cường hiệu quả chiến lược hơn nữa bằng cách điều chỉnh tham số và tối ưu hóa đa yếu tố.

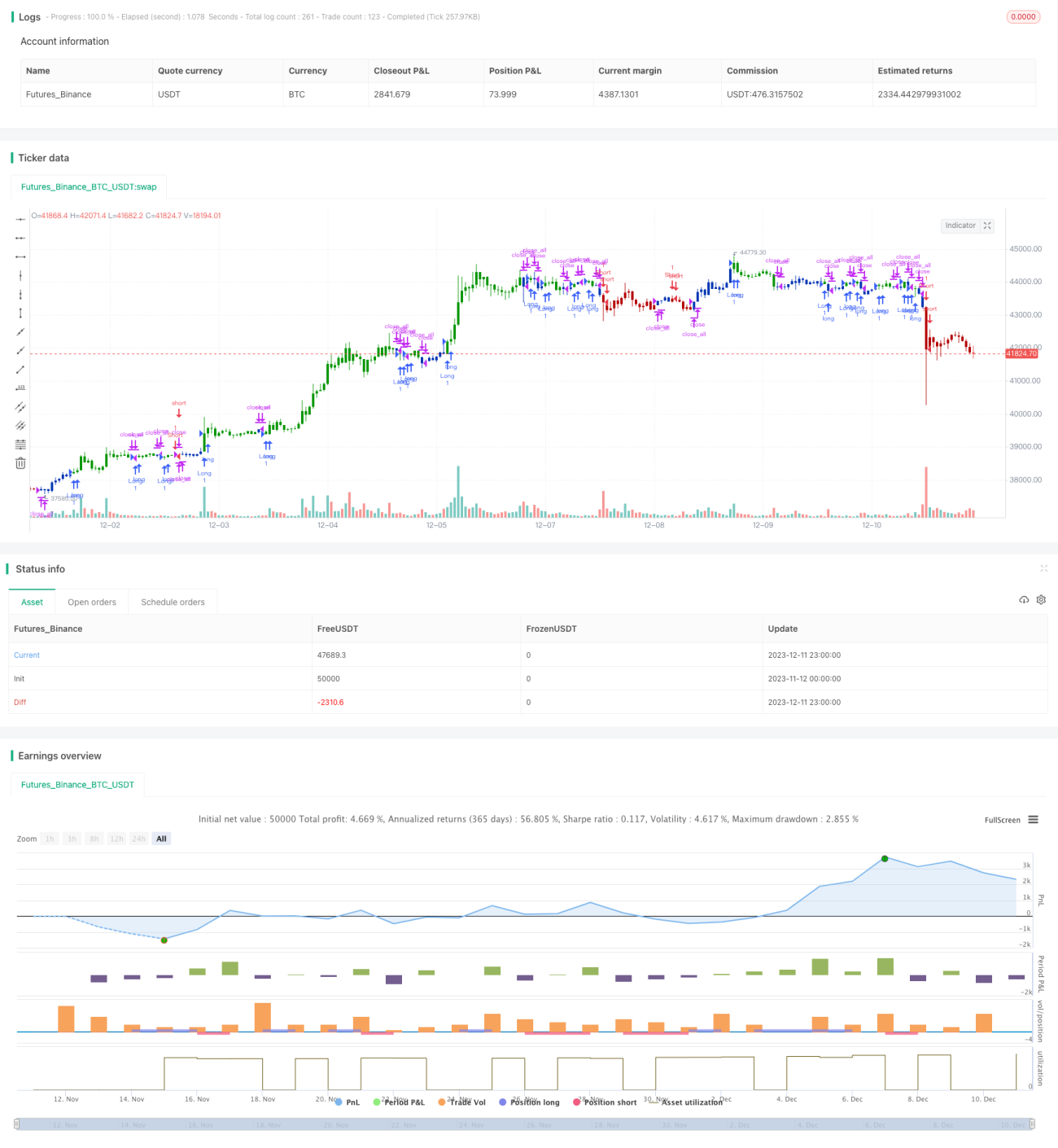

/*backtest

start: 2023-11-12 00:00:00

end: 2023-12-12 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 15/04/2021

// This is combo strategies for get a cumulative signal. - 1