Chiến lược đột phá giao cắt vàng hai đường EMA

Tổng quan

Chiến lược này là một chiến lược giao dịch theo xu hướng dựa trên tín hiệu Golden Cross và Death Cross của đường trung bình động hàm mũ (EMA) 5 phút và 34 phút. Khi đường nhanh cắt lên trên đường chậm, chiến lược sẽ mở vị thế mua; khi đường nhanh cắt xuống dưới đường chậm, chiến lược sẽ mở vị thế bán. Đồng thời, chiến lược thiết lập các mức chốt lời và cắt lỗ để kiểm soát rủi ro.

Nguyên lý chiến lược

- Đường nhanh EMA5 và đường chậm EMA34 tạo thành tín hiệu giao dịch. EMA5 phản ánh sự thay đổi giá gần đây nhất, EMA34 phản ánh sự thay đổi giá trong trung hạn.

- Khi đường nhanh cắt lên trên đường chậm, đó là tín hiệu Golden Cross, cho thấy xu hướng ngắn hạn tốt hơn xu hướng trung hạn, chiến lược sẽ nắm giữ vị thế mua.

- Khi đường nhanh cắt xuống dưới đường chậm, đó là tín hiệu Death Cross, cho thấy xu hướng ngắn hạn kém hơn xu hướng trung hạn, chiến lược sẽ nắm giữ vị thế bán.

- Thiết lập các mức chốt lời và cắt lỗ để khóa lợi nhuận và kiểm soát rủi ro.

Phân tích ưu điểm

- Sử dụng hai đường EMA để lọc các tín hiệu phá vỡ giả, tránh bị mắc kẹt.

- Theo dõi xu hướng trung hạn, tăng cường cơ hội sinh lời.

- Thiết lập các mức chốt lời và cắt lỗ giúp kiểm soát rủi ro hiệu quả.

Phân tích rủi ro

- Hai đường EMA có độ trễ nhất định, có thể bỏ lỡ các cơ hội giao dịch ngắn hạn.

- Nếu điểm cắt lỗ được đặt quá rộng, rủi ro thua lỗ có thể gia tăng.

- Nếu điểm chốt lời được đặt quá hẹp, có thể không tối đa hóa được cơ hội lợi nhuận.

Hướng tối ưu hóa

- Tối ưu hóa các tham số EMA để tìm ra bộ tham số tốt nhất.

- Tối ưu hóa các điểm chốt lời và cắt lỗ để khóa lợi nhuận lớn hơn.

- Bổ sung thêm các chỉ báo lọc khác như MACD, KDJ,... để nâng cao độ chính xác của tín hiệu.

Tổng kết

Chiến lược này tạo ra tín hiệu giao dịch dựa trên tín hiệu Golden Cross và Death Cross của hai đường trung bình động hàm mũ (EMA), đồng thời thiết lập các mức chốt lời và cắt lỗ để kiểm soát rủi ro. Đây là một chiến lược theo dõi xu hướng trung hạn đơn giản nhưng hiệu quả. Việc tối ưu hóa các tham số chốt lời, cắt lỗ và đưa thêm các chỉ báo khác để lọc tín hiệu có thể giúp tăng cường hơn nữa khả năng sinh lời ổn định của chiến lược.

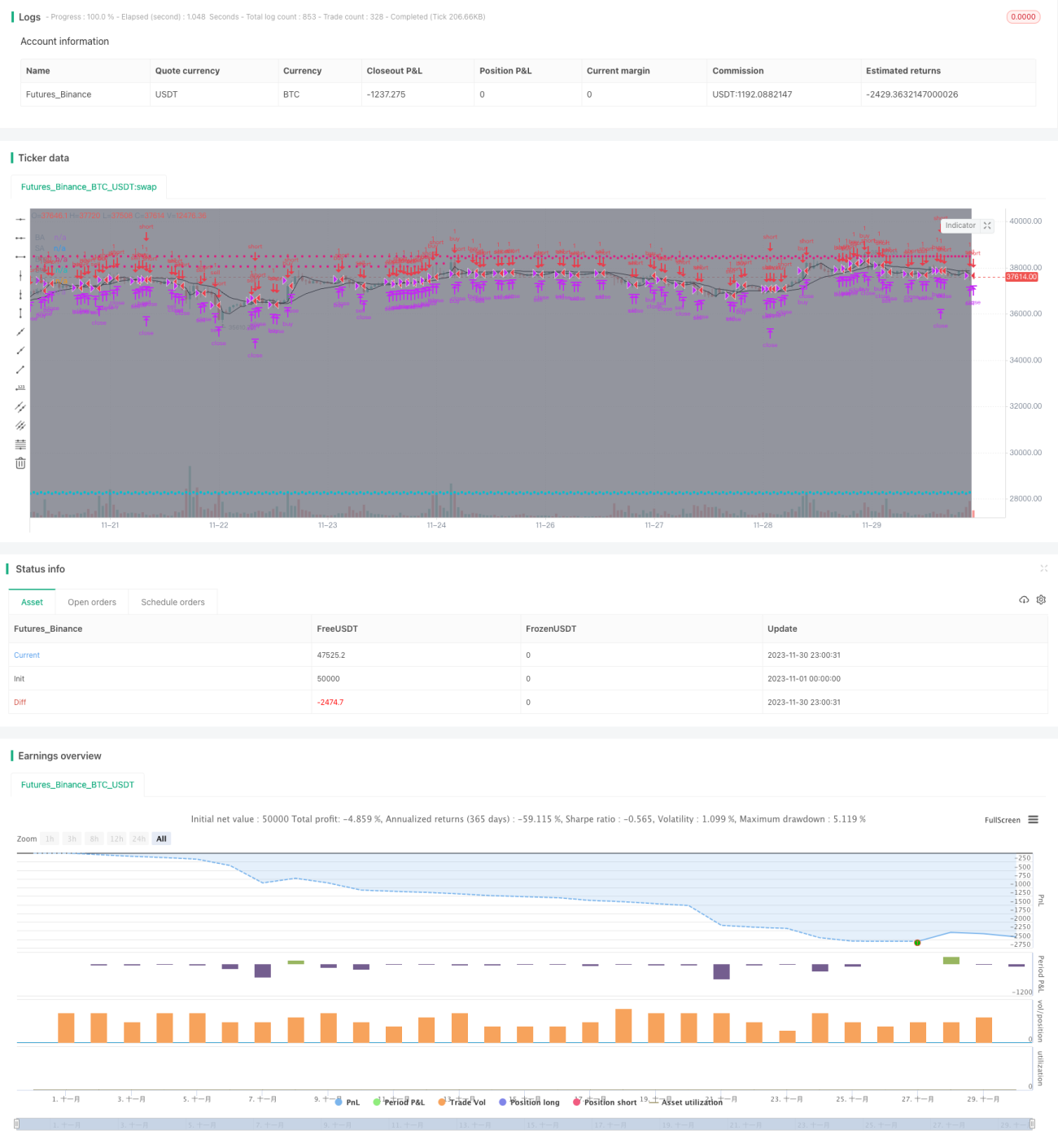

/*backtest

start: 2023-11-01 00:00:00

end: 2023-11-30 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy(title='[STRATEGY][RS]MicuRobert EMA cross V2', shorttitle='S', overlay=true, pyramiding=0, initial_capital=100000)

USE_TRADESESSION = input(title='Use Trading Session?', type=bool, defval=true)

USE_TRAILINGSTOP = input(title='Use Trailing Stop?', type=bool, defval=true)- 1