Chiến lược giao dịch định lượng MACD đảo ngược hai đường

Tổng quan

Chiến lược này là một chiến lược giao dịch định lượng MACD đảo ngược hai đường ray. Nó tham khảo các chỉ báo kỹ thuật được mô tả bởi William Blau trong cuốn sách "Momentum, Direction and Divergence" và mở rộng dựa trên đó. Chiến lược này cũng có chức năng backtest, có thể thêm các tính năng bổ sung như cảnh báo, bộ lọc, trailing stop, v.v.

Nguyên lý chiến lược

Chỉ báo cốt lõi của chiến lược là MACD. Nó tính toán đường trung bình động nhanh EMA(r) và đường trung bình động chậm EMA(slowMALen), sau đó tính toán chênh lệch xmacd giữa chúng. Ngoài ra, nó tính toán EMA(signalLength) của xmacd để có được xMA_MACD. Khi xmacd cắt lên trên xMA_MACD, mua; khi cắt xuống dưới, bán. Điểm mấu chốt của chiến lược này là tín hiệu giao dịch đảo ngược, tức là mối quan hệ giữa xmacd và xMA_MACD ngược với chỉ báo MACD thông thường, đây cũng là nguồn gốc của tên gọi "MACD đảo ngược".

Ngoài ra, chiến lược này còn giới thiệu bộ lọc xu hướng. Khi tín hiệu mua được đưa ra, nếu đã cấu hình bộ lọc xu hướng tăng, nó sẽ kiểm tra xem giá có đang tăng hay không; tương tự, tín hiệu bán sẽ kiểm tra xu hướng giảm giá. Chỉ báo RSI và MFI cũng có thể được sử dụng để lọc tín hiệu. Cơ chế dừng lỗ được cấu hình để ngăn chặn các khoản lỗ vượt quá ngưỡng.

Phân tích lợi thế

Lợi thế lớn nhất của chiến lược này là chức năng backtest mạnh mẽ. Có thể chọn các loại giao dịch khác nhau, thiết lập phạm vi thời gian backtest và tối ưu hóa chiến lược dựa trên dữ liệu của từng loại cụ thể. So với chiến lược MACD đơn giản, nó thêm các phán đoán về xu hướng, tình trạng quá mua/quá bán, có thể lọc ra một số tín hiệu trùng lặp. MACD đảo ngược hai đường ray khác với MACD truyền thống, có thể nắm bắt một số cơ hội mà MACD truyền thống có thể bỏ lỡ.

Phân tích rủi ro

Rủi ro của chiến lược này chủ yếu đến từ tư duy giao dịch đảo ngược. Mặc dù tín hiệu đảo ngược có thể thu được một số cơ hội, nhưng nó cũng có nghĩa là từ bỏ một số điểm mua/bán của MACD truyền thống, điều này cần được đánh giá cẩn thận. Ngoài ra, bản thân MACD dễ tạo ra vấn đề tín hiệu giả tăng. Nếu gặp thị trường dao động, chiến lược này có thể tạo ra quá nhiều giao dịch, tăng chi phí giao dịch và tổn thất trượt giá.

Để giảm rủi ro, có thể điều chỉnh thông số một cách thích hợp, tối ưu hóa độ dài đường trung bình động; kết hợp bộ lọc xu hướng và chỉ báo để tránh phát sinh tín hiệu trong thị trường dao động; tăng khoảng cách dừng lỗ một cách hợp lý để đảm bảo kiểm soát thua lỗ cho từng giao dịch riêng lẻ.

Hướng tối ưu hóa

Chiến lược này có thể được tối ưu hóa từ các khía cạnh sau:

- Điều chỉnh thông số đường ray nhanh và chậm, tối ưu hóa độ dài đường trung bình động, kiểm tra dữ liệu của từng loại cụ thể để tìm ra tổ hợp thông số tốt nhất.

- Thêm hoặc điều chỉnh bộ lọc xu hướng, dựa trên kết quả backtest để đánh giá xem có cải thiện tỷ suất lợi nhuận của chiến lược hay không.

- Kiểm tra các cơ chế dừng lỗ khác nhau, dừng lỗ cố định hay trailing stop tốt hơn.

- Thử kết hợp các chỉ báo khác như KD, Bollinger Bands, v.v., thiết lập nhiều điều kiện lọc hơn để đảm bảo chất lượng tín hiệu.

Tổng kết

Chiến lược định lượng MACD đảo ngược hai đường ray tham khảo ý tưởng của chỉ báo MACD cổ điển, mở rộng và cải tiến dựa trên đó. Chiến lược này có ưu điểm như cấu hình thông số linh hoạt, lựa chọn cơ chế lọc phong phú và chức năng backtest mạnh mẽ. Điều này cho phép nó được tối ưu hóa cá nhân hóa cho các loại giao dịch khác nhau, là một chiến lược giao dịch định lượng tiềm năng đáng để khám phá.

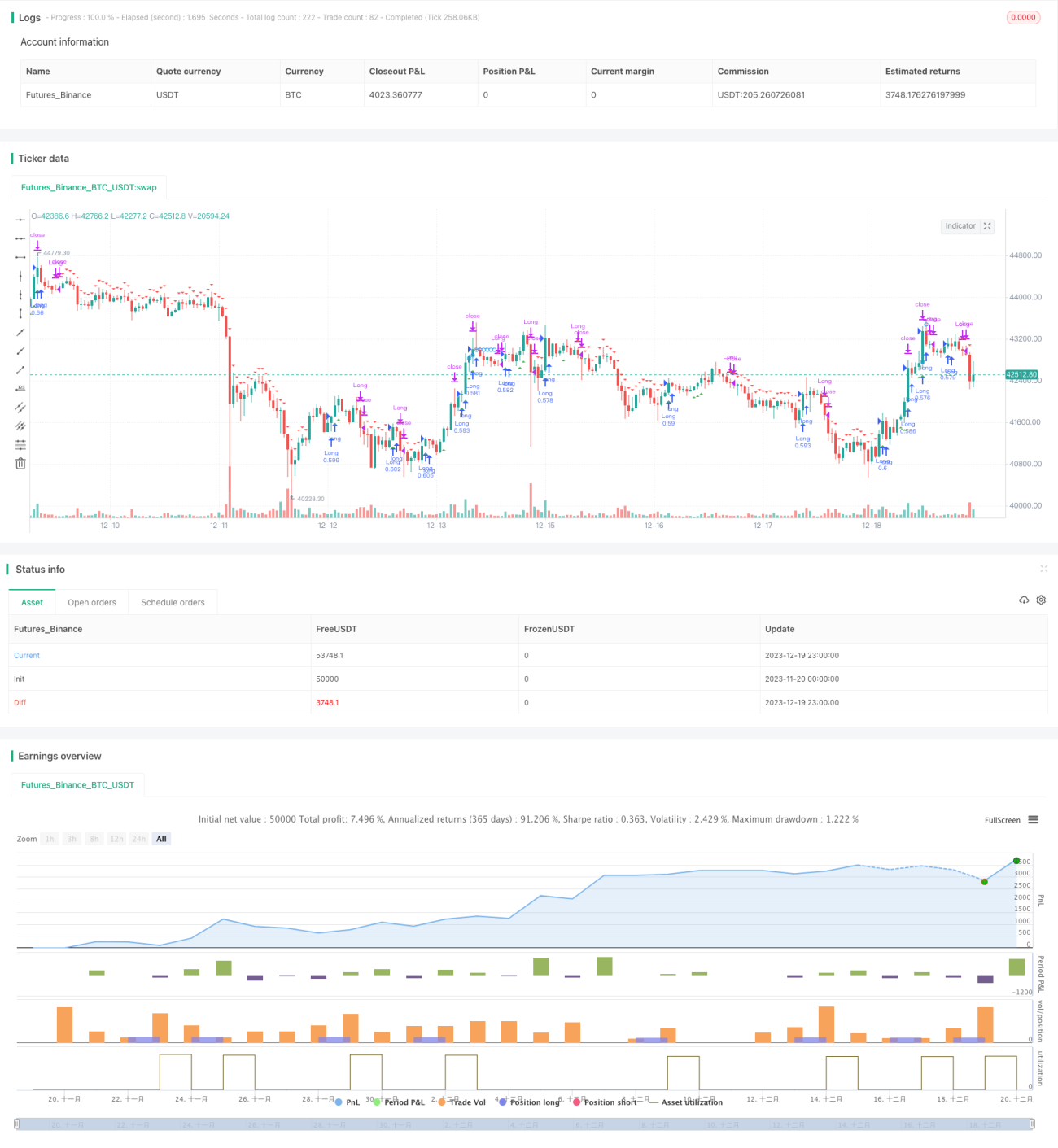

/*backtest

start: 2023-11-20 00:00:00

end: 2023-12-20 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version = 3

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 09/12/2016

// This is one of the techniques described by William Blau in his book- 1