Chiến lược giao dịch Bitcoin dựa trên chỉ số định lượng

Tổng quan

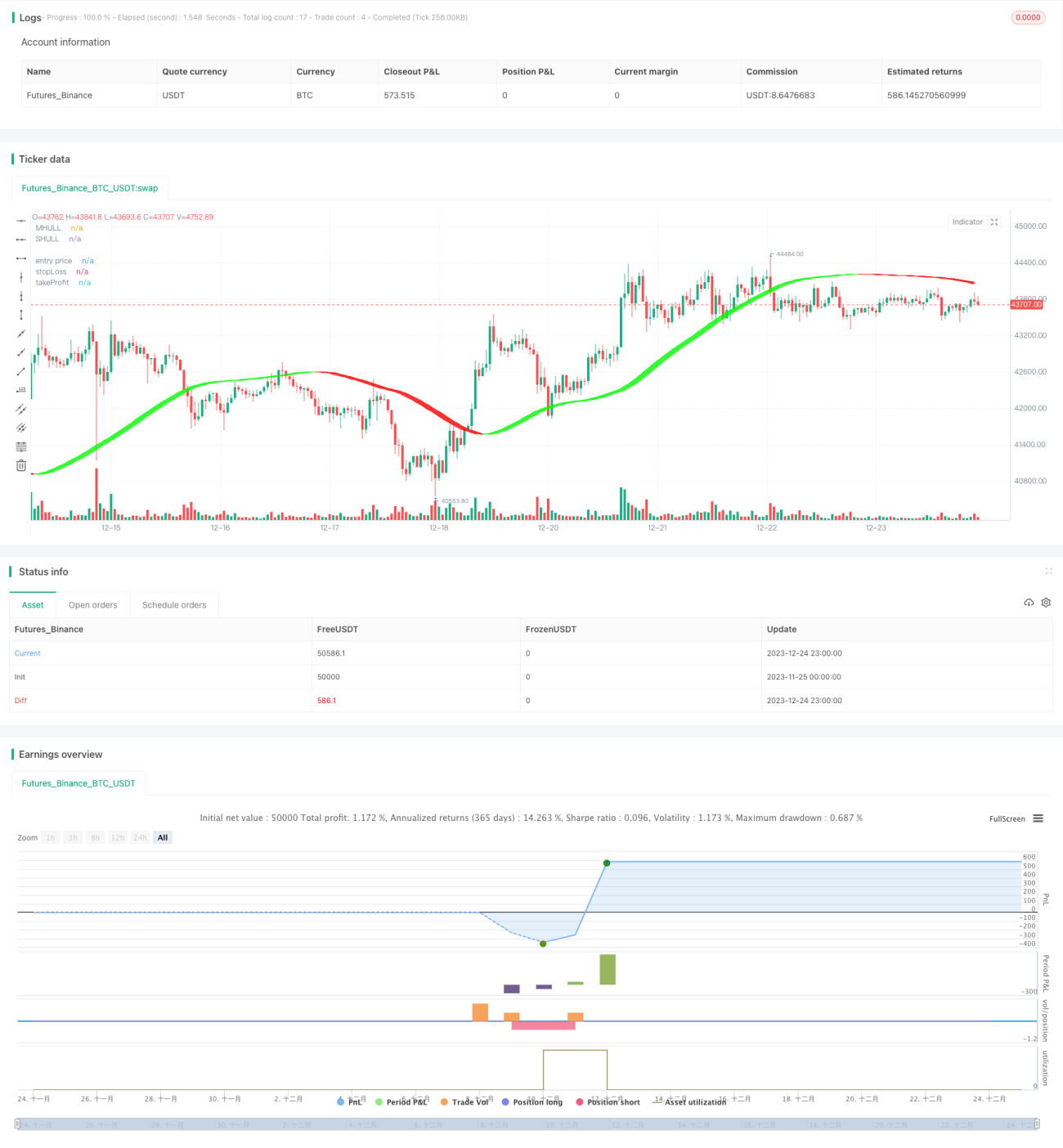

Chiến lược này sử dụng nhiều chỉ báo định lượng để xác định thời điểm mua bán Bitcoin, thực hiện giao dịch tự động. Các chỉ báo chính bao gồm Chỉ báo Hull (Hull), Chỉ số sức mạnh tương đối (RSI), Dải Bollinger (BB) và Bộ dao động khối lượng (VO).

Nguyên lý chiến lược

-

Sử dụng đường trung bình động Hull đã được điều chỉnh để xác định xu hướng chính của thị trường, kết hợp với Dải Bollinger để hỗ trợ xác định điểm mua bán phá vỡ.

-

Chỉ báo RSI kết hợp với phạm vi biến động thích ứng để xác định vùng quá mua/quá bán, phát ra tín hiệu giao dịch. Đồng thời thiết lập hai bộ tham số làm tín hiệu xác nhận Duplicate.

-

Bộ dao động khối lượng xác định lực mua bán, tránh các phá vỡ giả.

-

Theo tỷ lệ tham số giá dừng lỗ/chốt lời, thiết lập trước các mức dừng lỗ và chốt lời để quản lý rủi ro.

Phân tích ưu điểm

-

Đường Hull có thể nắm bắt nhanh hơn sự chuyển đổi xu hướng, Dải Bollinger hỗ trợ giúp giảm tín hiệu nhiễu.

-

Chỉ báo RSI với tham số tối ưu và xác nhận tín hiệu Duplicate có độ tin cậy cao hơn.

-

Bộ dao động khối lượng kết hợp với xu hướng và tín hiệu chỉ báo, tránh giao dịch không chính xác.

-

Phương pháp dừng lỗ/chốt lời được thiết lập trước có thể tự động kiểm soát lãi lỗ từng giao dịch, quản lý hiệu quả rủi ro tổng thể.

Phân tích rủi ro

-

Thiết lập tham số không phù hợp có thể dẫn đến tần suất giao dịch quá cao hoặc hiệu quả tín hiệu kém.

-

Khi xảy ra biến động mạnh do sự kiện bất ngờ, mức dừng lỗ có thể bị phá vỡ, gây ra tổn thất lớn.

-

Khi chuyển sang các đồng tiền khác, cần kiểm tra lại và tối ưu hóa tham số.

-

Khi thiếu dữ liệu khối lượng, bộ dao động khối lượng sẽ không hoạt động.

Hướng tối ưu hóa

-

Thực hiện nhiều bài kiểm tra kết hợp tham số RSI hơn để tìm ra tham số tối ưu nhất.

-

Thử kết hợp các chỉ báo khác như MACD, KD với RSI để nâng cao độ chính xác của tín hiệu.

-

Thêm module dự đoán mô hình, kết hợp học máy để xác định hướng thị trường.

-

Kiểm tra hiệu quả tham số khi chuyển sang các sản phẩm giao dịch khác.

-

Tối ưu hóa thuật toán dừng lỗ/chốt lời để tối đa hóa lợi nhuận.

Tổng kết

Chiến lược này kết hợp nhiều chỉ báo kỹ thuật định lượng để xác định thời điểm mua bán. Thông qua tối ưu hóa tham số, kiểm soát rủi ro và các phương pháp khác, đã thực hiện giao dịch tự động Bitcoin. Hiệu quả khá tốt, nhưng vẫn cần tiếp tục kiểm tra và tối ưu hóa để thích ứng với biến động thị trường. Có thể cung cấp tham khảo cho nhà đầu tư, hỗ trợ quyết định giao dịch.

- 1