Chiến lược tích lũy đột phá dựa trên bộ lọc nến có ý nghĩa

Tổng quan

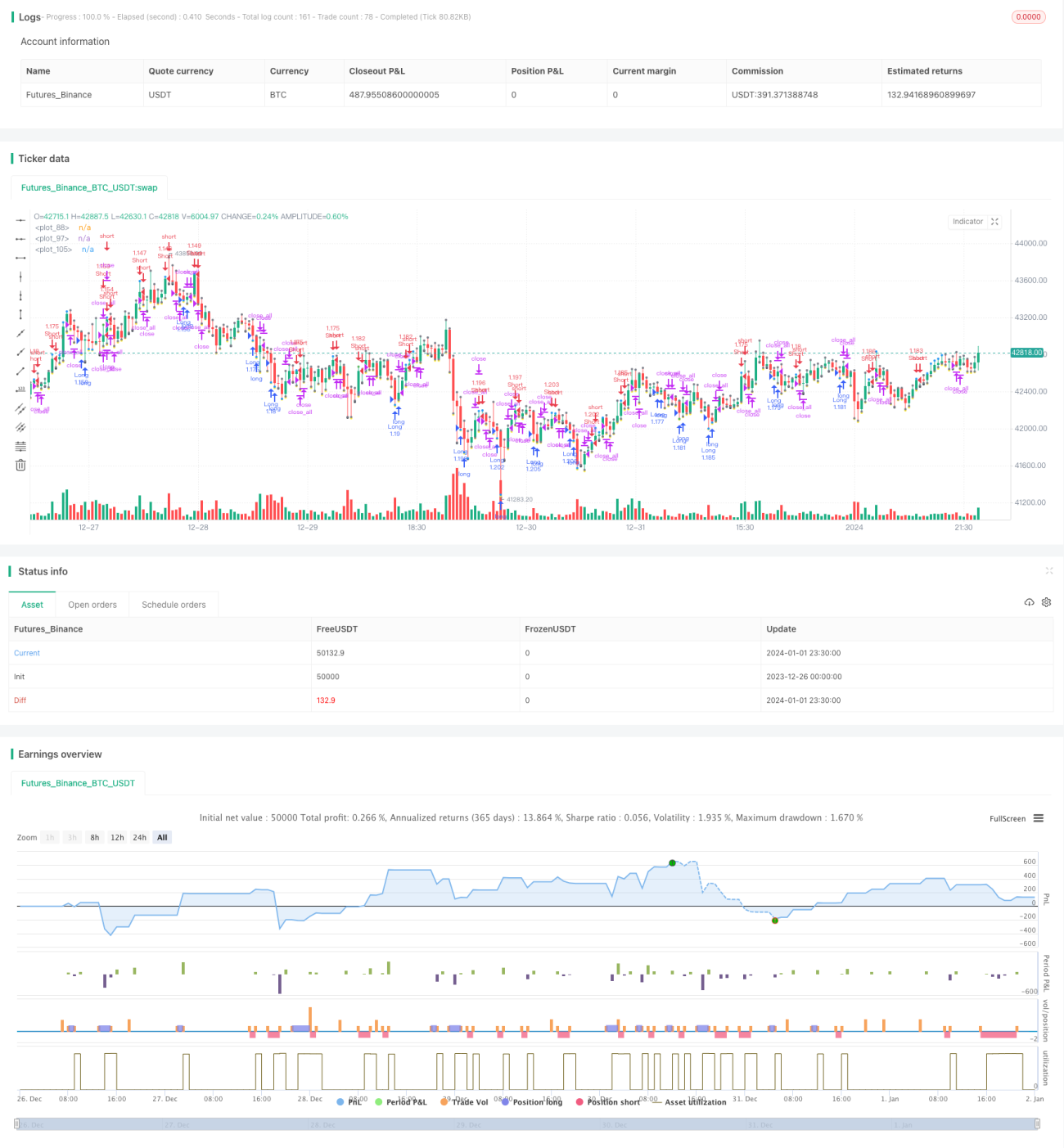

Chiến lược này dự đoán xu hướng bằng cách xác định "nến ý nghĩa" của cây nến, kết hợp với tín hiệu đột phá để phát ra tín hiệu giao dịch. Chiến lược sẽ lọc bỏ những cây nến quá nhỏ, chỉ phân tích các "nến ý nghĩa", giúp tránh bị nhiễu bởi các biến động nhỏ quá thường xuyên, làm cho tín hiệu ổn định và đáng tin cậy hơn.

Nguyên lý chiến lược

-

Xác định độ dài thân nến hiện tại

body, nếu lớn hơn 3 lần giá trị trung bình củabodycủa 6 cây nến trước đó, thì coi đó là "nến ý nghĩa". -

Nếu 3 cây "nến ý nghĩa" liên tiếp đều là nến xanh, thì xác định là tín hiệu tăng; nếu 3 cây "nến ý nghĩa" liên tiếp đều là nến đỏ, thì xác định là tín hiệu giảm.

-

Đồng thời với việc xác định tín hiệu, nếu giá phá vỡ đỉnh hoặc đáy trước đó, cũng sẽ phát sinh tín hiệu giao dịch bổ sung.

-

Sử dụng đường trung bình SMA làm bộ lọc, chỉ mở vị thế khi giá phá vỡ SMA.

-

Sau khi nắm giữ vị thế, nếu giá lại phá vỡ điểm vào lệnh hoặc đường SMA, thì đóng vị thế.

Phân tích ưu điểm

-

Sử dụng "nến ý nghĩa" để xác định xu hướng, có thể lọc bỏ quá nhiều nhiễu không cần thiết, làm cho tín hiệu rõ ràng hơn.

-

Kết hợp tín hiệu xu hướng và tín hiệu đột phá, có thể nâng cao chất lượng tín hiệu, giảm tín hiệu giả.

-

Bộ lọc đường SMA giúp tránh mua đuổi bán đỉnh. Mua khi giá dưới SMA, bán khi giá trên SMA, tăng độ tin cậy của tín hiệu.

-

Thiết lập điều kiện chốt lời cắt lỗ, có thể kịp thời cắt lỗ và chốt lời, có lợi cho việc bảo toàn vốn.

Phân tích rủi ro

-

Chiến lược này khá mạo hiểm, sử dụng 3 cây nến để xác định tín hiệu, có thể nhầm lẫn dao động ngắn hạn là đảo chiều xu hướng.

-

Dữ liệu kiểm thử không đầy đủ, hiệu quả có thể khác nhau đối với các sản phẩm và khung thời gian khác nhau.

-

Không có kiểm soát vị thế qua đêm phiên giao dịch đêm, tồn tại rủi ro vị thế qua đêm.

Hướng tối ưu

-

Có thể tối ưu hóa thêm các tham số của "nến ý nghĩa", như số lượng nến để xác định, định nghĩa về "ý nghĩa", v.v.

-

Có thể kiểm tra ảnh hưởng của các tham số khung thời gian khác nhau đến hiệu quả, tìm ra khung thời gian tối ưu.

-

Có thể thêm ATR stop loss để kiểm soát rủi ro.

-

Có thể cân nhắc thêm logic kiểm soát vị thế qua đêm.

Tổng kết

Chiến lược này sử dụng bộ lọc "nến ý nghĩa" và xác định xu hướng, kết hợp với đột phá để tạo thành tín hiệu giao dịch, có thể lọc hiệu quả các biến động nhỏ không cần thiết, tín hiệu rõ ràng và đáng tin cậy hơn. Tuy nhiên, do chu kỳ xác định ngắn, có thể có rủi ro nhận định sai nhất định. Có thể hoàn thiện thêm thông qua tối ưu tham số và biện pháp quản lý rủi ro.

- 1