Chiến lược kênh giá Bollinger Bands đột phá và đảo chiều thông minh

Tổng quan

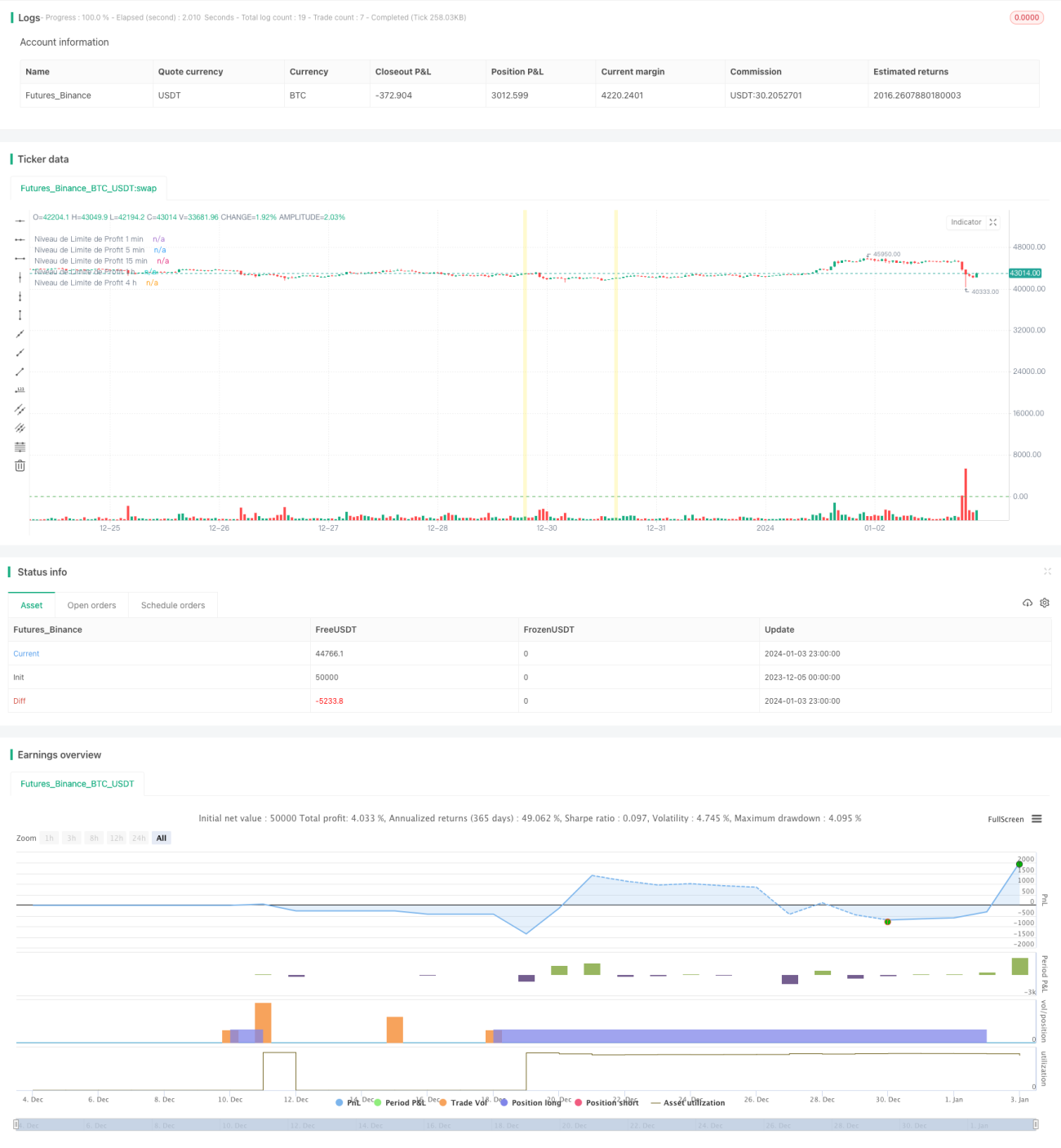

Chiến lược này là một chiến lược đột phá kết hợp nhiều khung thời gian (1 phút, 5 phút, 15 phút, 1 giờ và 4 giờ), nó phát hiện các vùng hỗ trợ và kháng cự trên biểu đồ.

Nguyên lý chiến lược

Chiến lược này sử dụng Bollinger Bands và kênh giá để xác định các vùng hỗ trợ và kháng cự. Đầu tiên, nó tính toán đường trung bình động đơn giản (SMA) và độ lệch chuẩn (STDEV) dựa trên giá đóng cửa của mỗi khung thời gian, từ đó xác định dải trên và dải dưới. Sau đó, nó phát hiện "khối đột phá", được xác định dựa trên tình trạng giá phá vỡ khỏi mức hỗ trợ hoặc kháng cự cùng với khối lượng giao dịch. Khi giá phá vỡ mức hỗ trợ hoặc kháng cự với khối lượng giao dịch cao, một khối đột phá được hình thành.

Khi phát hiện khối đột phá, nếu giá phá vỡ dải dưới thì tạo ra tín hiệu mua; nếu phá vỡ dải trên thì tạo ra tín hiệu bán. Chiến lược này cũng vẽ kênh giá cho mỗi khung thời gian, biểu thị các mức hỗ trợ và kháng cự.

Ngoài ra, chiến lược này thiết lập mức chốt lời cho mỗi khung thời gian. Điều này có nghĩa là các mức giá được chỉ định cho vị thế nên được đóng lệnh có lợi nhuận. Đồng thời cũng thiết lập mức cắt lỗ để hạn chế thua lỗ.

Phân tích ưu điểm

- Sử dụng phân tích đa khung thời gian, đánh giá xu hướng thị trường toàn diện hơn

- Kết hợp khối đột phá, dải Bollinger và khối lượng giao dịch, làm cho tín hiệu đáng tin cậy hơn

- Thiết lập chốt lời cắt lỗ, hỗ trợ kiểm soát rủi ro

Phân tích rủi ro

- Thiết lập tham số Bollinger Bands không phù hợp có thể dẫn đến tín hiệu giả

- Đột phá có thể là nhiễu thị trường ngắn hạn, từ đó phát sinh rủi ro kẹt lệnh

- Đánh giá nhiều khung thời gian làm tăng độ phức tạp của chiến lược

Có thể tránh rủi ro hơn nữa bằng cách tối ưu tham số Bollinger Bands, tăng thời gian nắm giữ hoặc thiết lập cắt lỗ.

Hướng tối ưu

Chiến lược này có thể được tối ưu theo các hướng sau:

- Tối ưu tham số Bollinger Bands để dải trên và dải dưới phản ánh tốt hơn hỗ trợ và kháng cự thực tế

- Thêm thuật toán học máy để đánh giá hướng và sức mạnh đột phá

- Thêm chỉ báo biến động giá để xác định thời điểm mua bán tốt nhất

- Kết hợp thêm nhiều chỉ báo như MACD, KD… để đánh giá xu hướng và năng lượng

Tổng kết

Chiến lược này tích hợp phân tích chỉ báo kỹ thuật đa khung thời gian, thông qua giao dịch đột phá, quản lý rủi ro bằng chốt lời cắt lỗ, là một chiến lược giao dịch hệ thống đột phá linh hoạt và đáng tin cậy. Tuy nhiên, việc thiết lập tham số và kiểm soát rủi ro vẫn cần được kiểm tra và tối ưu liên tục dựa trên thị trường thực tế.

- 1