Chiến lược giao nhau hai đường trung bình động trọng số động lượng

1

Follow

1802

Followers

Tổng quan

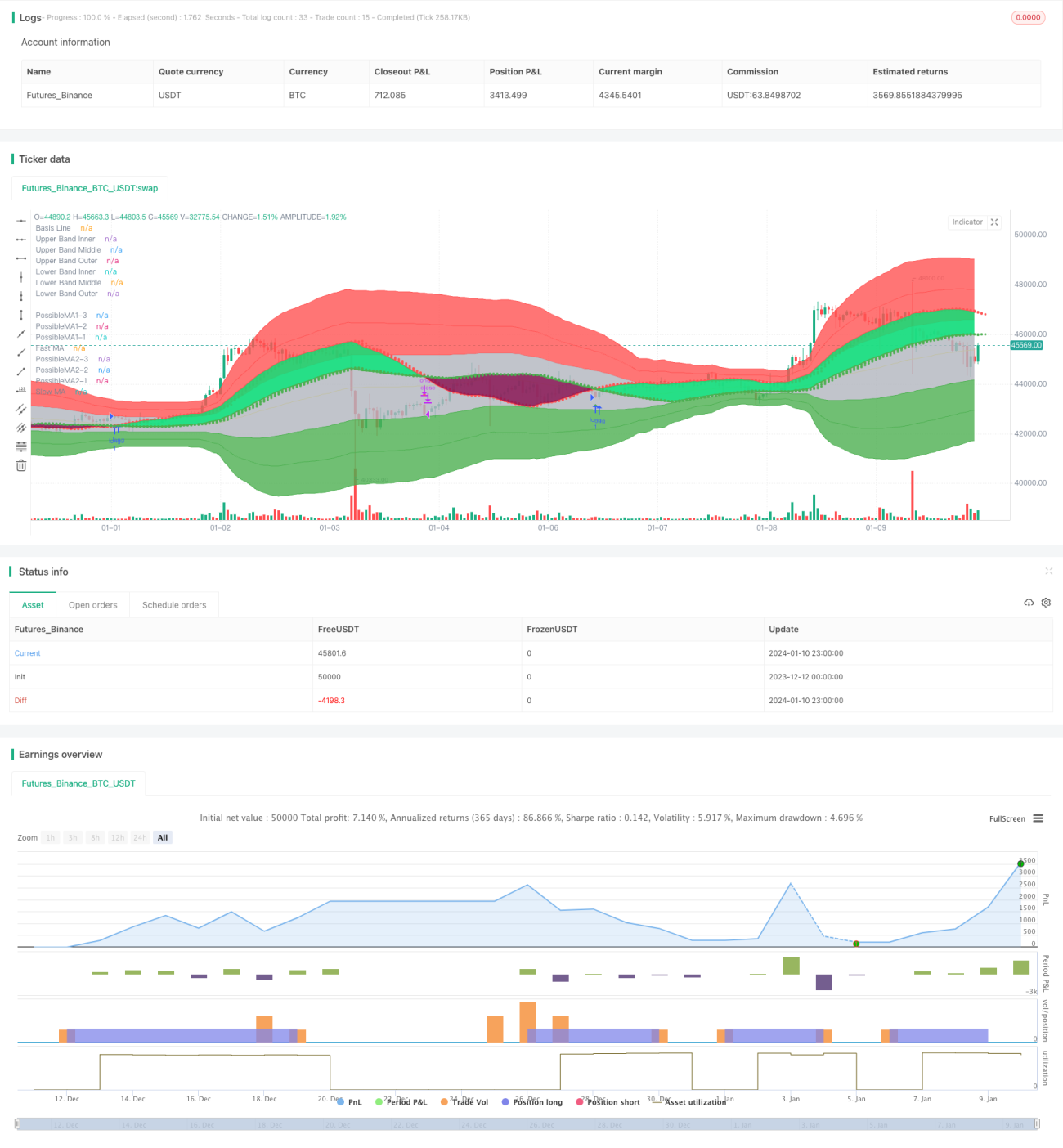

Chiến lược này tính toán hai đường trung bình động có trọng số động lượng (MAEMA) với chu kỳ khác nhau, và tạo ra tín hiệu mua/bán khi chúng giao nhau. Trong đó, đường ngắn hạn dùng để đánh giá xu hướng thị trường và tín hiệu đảo chiều ngắn hạn, trong khi đường dài hạn xác định hướng xu hướng chính.

Nguyên lý

- Tính MAEMA của đường nhanh (chu kỳ 80) và đường chậm (chu kỳ 144).

- Đường nhanh phản ánh xu hướng ngắn hạn và điểm đảo chiều. Đường chậm phản ánh hướng xu hướng chính.

- Khi đường nhanh cắt lên trên đường chậm, xuất hiện tín hiệu mua. Khi đường nhanh cắt xuống dưới đường chậm, xuất hiện tín hiệu bán.

- Chiến lược cũng vẽ 3 điểm dự báo, biểu thị giá trị có thể có của chu kỳ tiếp theo, từ đó đánh giá xu hướng giao nhau trong tương lai.

- Chiến lược tận dụng tối đa tính chất động lượng và chức năng dự báo của chỉ báo MAEMA.

Phân tích ưu điểm

- Bản thân MAEMA đã tích hợp yếu tố động lượng, có thể nắm bắt sự thay đổi xu hướng nhanh hơn.

- Chiến lược hai đường trung bình, đánh giá hướng xu hướng trong các khung thời gian khác nhau.

- Kết hợp giao nhau của đường nhanh/chậm và điểm dự báo của chính MAEMA, làm cho tín hiệu mua/bán đáng tin cậy hơn.

- Đồ thị được vẽ tự động đầy đủ, phản ánh trực quan biến động thị trường.

Phân tích rủi ro

- Khi thị trường biến động bất thường, độ nhạy của chỉ báo MAEMA có thể quá cao, dẫn đến tín hiệu sai. Có thể nới lỏng điểm dừng lỗ hợp lý.

- Hệ thống đường trung bình dễ tạo ra tín hiệu giả trong thị trường đi ngang. Có thể thêm các bộ lọc khác.

- Cần xác định tham số tối ưu cho chu kỳ đường nhanh và đường chậm tùy theo từng loại tài sản.

Hướng tối ưu hóa

- Tối ưu hóa tham số chu kỳ của MAEMA đường nhanh và đường chậm để tìm ra tổ hợp tham số tốt nhất.

- Thêm điều kiện lọc để tránh mở vị thế trong thị trường dao động. Ví dụ đưa vào DMI, MACD để đánh giá tính xu hướng.

- Dựa trên kết quả backtest điều chỉnh hệ số ATR, điểm dừng lỗ động để giảm false positive và kiểm soát rủi ro.

Tổng kết

Chiến lược này sử dụng giao nhau của hai đường trung bình động có trọng số động lượng để đánh giá sự thay đổi xu hướng thị trường, nguyên lý cơ bản rõ ràng và đơn giản. Kết hợp với tính động lượng và chức năng dự báo của chính MAEMA, hiệu quả nhận diện tín hiệu đảo chiều khá tốt. Cần chú ý tối ưu hóa tham số và tăng cường điều kiện lọc để nâng cao độ ổn định.

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1