Chiến lược lợi nhuận ngắn hạn dựa trên mô hình chữ V của RSI

Tổng quan

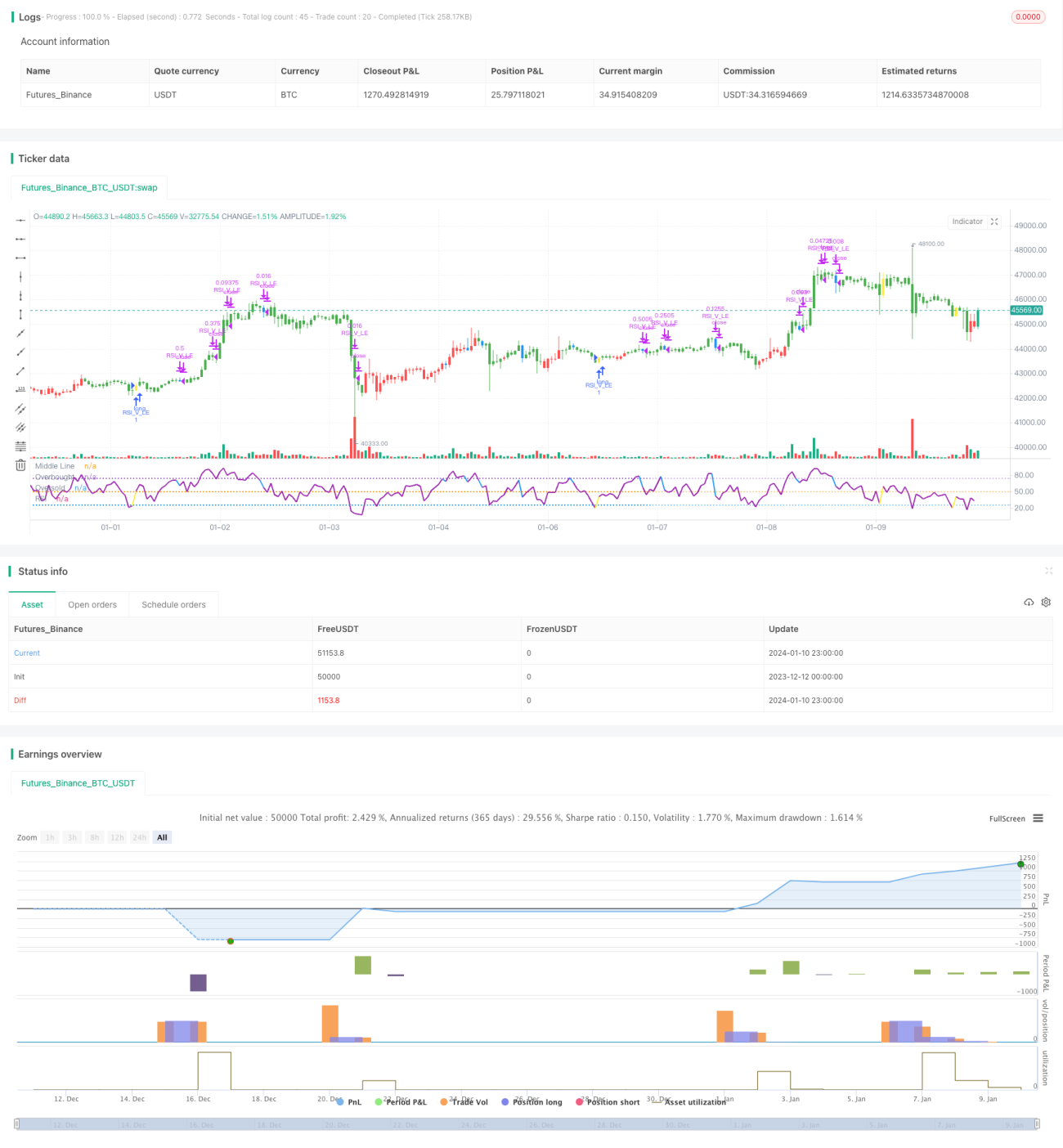

Chiến lược này dựa trên hình thái chữ V của chỉ báo RSI, kết hợp với bộ lọc đường trung bình EMA, tạo thành một chiến lược lợi nhuận ngắn hạn tương đối đáng tin cậy. Nó có thể nắm bắt các cơ hội hình thành từ sự bật lên của giá trong vùng quá bán, thông qua tín hiệu hình thái chữ V của RSI để mua chính xác, từ đó đạt được mục tiêu kiếm lợi nhuận trong ngắn hạn.

Nguyên lý chiến lược

- Sử dụng đường 20 ngày nằm trên đường 50 ngày làm điều kiện xu hướng dài hạn tăng.

- RSI hình thành hình thái chữ V, biểu thị cơ hội bật lên từ vùng quá bán.

- Đáy của nến trước thấp hơn đáy của hai nến trước đó.

- RSI của nến hiện tại cao hơn RSI của hai nến trước đó.

- RSI vượt lên trên 30 làm tín hiệu hoàn thành hình thái chữ V, mua lên.

- Cắt lỗ đặt dưới giá vào lệnh 8%.

- Khi RSI vượt qua 70, bắt đầu di chuyển điểm dừng lỗ lên giá vào lệnh.

- Khi RSI vượt qua 90, bắt đầu chốt 3/4 vị thế.

- Khi RSI cắt xuống dưới 10 hoặc kích hoạt cắt lỗ, đóng toàn bộ vị thế.

Phân tích ưu điểm

- Sử dụng đường trung bình EMA để đánh giá xu hướng chính, tránh giao dịch ngược chiều.

- Hình thái chữ V của RSI xác định cơ hội bật lên từ vùng quá bán, bắt kịp xu hướng đảo chiều.

- Nhiều cơ chế cắt lỗ giúp kiểm soát rủi ro.

Phân tích rủi ro

- Trong trường hợp thị trường giảm mạnh, có thể không kịp cắt lỗ, dẫn đến thua lỗ lớn.

- Tín hiệu hình thái chữ V của RSI có thể có sai sót, dẫn đến thua lỗ không đáng có.

Hướng tối ưu

- Tối ưu tham số RSI, tìm kiếm hình thái chữ V RSI đáng tin cậy hơn.

- Kết hợp với các chỉ báo khác để đánh giá độ tin cậy của tín hiệu đảo chiều.

- Tối ưu chiến lược cắt lỗ, vừa tránh quá mạo hiểm vừa kịp thời cắt lỗ.

Tổng kết

Chiến lược này tích hợp bộ lọc đường trung bình EMA và đánh giá hình thái chữ V của RSI, tạo thành một bộ chiến lược giao dịch ngắn hạn tương đối đáng tin cậy. Nó có thể nắm bắt hiệu quả các cơ hội bật lên từ vùng quá bán, tạo ra lợi nhuận trong ngắn hạn. Thông qua việc liên tục tối ưu tham số và mô hình, hoàn thiện cơ chế cắt lỗ, chiến lược này có thể tăng cường thêm tính ổn định và khả năng sinh lời. Nó mở ra một cánh cửa khác để các nhà giao dịch định lượng kiếm lợi nhuận ngắn hạn.

- 1