Chiến lược định lượng kết hợp đường trung bình động ba lần và MACD

Tổng quan

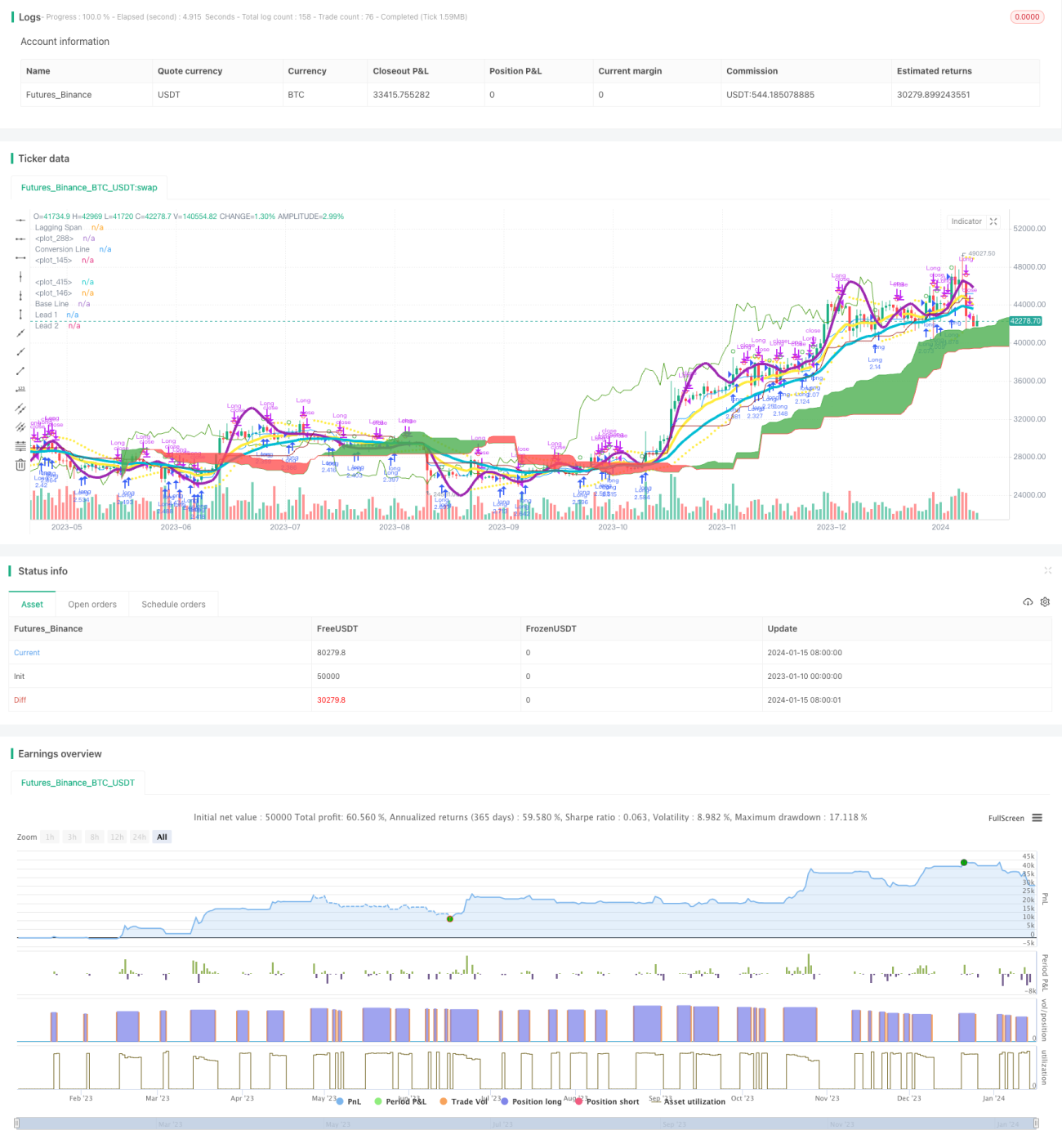

Chiến lược này kết hợp sử dụng chỉ báo đường trung bình động ba lớp và chỉ báo MACD để phát triển một chiến lược giao dịch định lượng khá ổn định và đáng tin cậy. Chiến lược này nhằm mục đích bắt kịp các xu hướng có thể xuất hiện trong tương lai, đặc biệt phù hợp cho các vị thế nắm giữ trung và dài hạn.

Nguyên lý chiến lược

Chiến lược này chủ yếu dựa trên sự kết hợp giữa đường trung bình động ba lớp và chỉ báo MACD.

Đầu tiên, chiến lược sử dụng ba đường trung bình động hàm mũ có độ dài lần lượt là 3, 7 và 2. Ba đường trung bình động này tạo thành một hệ thống trung bình động từ nhanh đến chậm, dùng để xác định hướng xu hướng trong tương lai. Khi đường trung bình động ngắn hạn cắt lên trên đường trung bình động dài hạn, đó là tín hiệu mua (long); khi đường trung bình động ngắn hạn cắt xuống dưới đường trung bình động dài hạn, đó là tín hiệu bán (short).

Thứ hai, chiến lược cũng đồng thời sử dụng chỉ báo MACD với các tham số 3 và 7. Khi đường chính MACD cắt lên trên đường tín hiệu, đó là tín hiệu mua; khi cắt xuống dưới, đó là tín hiệu bán.

Bằng cách kết hợp sử dụng hai chỉ báo, có thể tránh được nhiều tín hiệu sai do một chỉ báo đơn lẻ gây ra, từ đó nâng cao độ ổn định của chiến lược.

Ưu điểm của chiến lược

- Sử dụng hai chỉ báo để lọc, nâng cao chất lượng tín hiệu

- Tham số đã được tối ưu hóa qua nhiều lần kiểm tra, ổn định và đáng tin cậy

- Áp dụng hệ thống trung bình động ba lớp, có thể lọc hiệu quả nhiễu thị trường và xác định xu hướng tương lai

- Tham số MACD được thiết lập nhanh, có thể nhanh chóng bắt kịp các cơ hội ngắn hạn

Rủi ro của chiến lược

- Tồn tại rủi ro drawdown và thua lỗ liên tiếp

- Khi thị trường không có xu hướng rõ ràng, chiến lược này sẽ phát sinh nhiều giao dịch sai

- Chỉ báo MACD dễ tạo ra tín hiệu sai, cần kết hợp với chỉ báo đường trung bình động

Giải pháp:

- Áp dụng chiến lược cắt lỗ phù hợp để kiểm soát drawdown tối đa

- Khi trạng thái thị trường rõ ràng là không có xu hướng, giảm tần suất giao dịch

- Tối ưu hóa tham số MACD và kết hợp với các chỉ báo khác

Hướng tối ưu hóa chiến lược

- Kiểm tra và tối ưu hóa các tham số của đường trung bình động và MACD để tìm ra tổ hợp tốt nhất

- Thêm các chỉ báo phụ trợ như KDJ, VRSI để tránh tín hiệu sai

- Đưa vào mô hình học máy để đánh giá trạng thái thị trường, thực hiện điều chỉnh linh hoạt

- Kết hợp chiến lược cắt lỗ, thiết lập điểm cắt lỗ tối ưu

Tổng kết

Chiến lược này thông qua sự kết hợp giữa đường trung bình động và MACD đã đạt được khả năng bắt xu hướng ổn định. Ưu điểm của chiến lược nằm ở việc kết hợp các chỉ báo, giúp giảm thiểu hiệu quả các tín hiệu sai, từ đó đạt được hiệu quả chiến lược tốt hơn. Bước tiếp theo, thông qua tối ưu hóa tham số, đưa vào chiến lược cắt lỗ, điều chỉnh linh hoạt và các biện pháp khác để hoàn thiện chiến lược này hơn nữa, biến nó thành một công cụ hiệu quả để tìm kiếm cơ hội trung và dài hạn.

/*backtest

start: 2023-01-10 00:00:00

end: 2024-01-16 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

strategy("Matt's MACD Algo v1", shorttitle="Matt's MACD Algo v1", overlay=true, pyramiding = 0, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital=7000, calc_on_order_fills = true, commission_type=strategy.commission.percent, commission_value=0, currency = currency.USD)

//study("MFI Fresh", shorttitle="MFI Fresh", overlay=true)

- 1