Chiến lược giao dịch hỗn hợp

Tổng quan

Chiến lược giao dịch theo mùa vụ kết hợp S&P500 là một chiến lược định lượng sử dụng quy luật theo mùa để giao dịch cổ phiếu. Chiến lược này kết hợp hệ thống mua giữ cải tiến, điều kiện chỉ báo kỹ thuật và chỉ báo dòng tiền, thực hiện xoay vòng giữa các tháng giao dịch tốt và kém trong năm.

Nguyên lý chiến lược

Tín hiệu và quy tắc giao dịch của chiến lược như sau:

- Vào lệnh mua tại thời điểm mở cửa phiên giao dịch đầu tiên của tháng 10 hàng năm.

- Khi VIX cao hơn 60% hoặc ATR 15 ngày cao hơn 90%, tạm hoãn giao dịch theo mùa vụ, chờ thị trường ổn định trở lại mới vào lệnh.

- Đóng vị thế tại thời điểm mở cửa phiên giao dịch đầu tiên của tháng 8 hàng năm.

- Khi VIX vượt quá 120% hoặc chỉ báo dòng tiền VFI phá vỡ dưới -20 và đường trung bình 10 ngày đi xuống, cũng phát tín hiệu đóng vị thế.

- Có thể tùy chọn thêm giao dịch bán khống.

Chiến lược này tận dụng quy luật thị trường cổ phiếu có hiệu suất không đồng đều trong năm, mua vào trong các tháng 10-4 có lịch sử hiệu suất tốt, chốt lời hoặc bán khống trong các tháng 5-9 có lịch sử hiệu suất kém, thực hiện giao dịch ngược. Đồng thời, chiến lược bổ sung một số điều kiện chỉ báo kỹ thuật, tạm hoãn giao dịch khi thị trường biến động mạnh, giúp phòng tránh rủi ro.

Phân tích ưu điểm

Chiến lược giao dịch theo mùa vụ kết hợp S&P500 có những ưu điểm sau:

- Tận dụng quy luật theo mùa ổn định và đã được kiểm chứng. Chiến lược dựa trên thực tế chỉ số S&P500 có các tháng hiệu suất khác biệt rõ rệt trong năm.

- Kết hợp nhiều bộ lọc. Chiến lược bổ sung nhiều điều kiện như VIX, ATR, VFI, có thể lọc nhiễu hiệu quả và đưa ra tín hiệu giao dịch đáng tin cậy hơn.

- Quy tắc giao dịch có thể cấu hình. Chiến lược có thể tùy chọn thêm mua hoặc bán, các tháng giao dịch cũng có thể điều chỉnh theo nhu cầu, dễ dàng kiểm tra và tối ưu.

- Cơ chế phòng tránh rủi ro tích hợp. Ví dụ phát hiện biến động qua VIX và ATR, có thể hiệu quả tránh tác động của biến động thị trường mạnh.

- Chỉ báo dòng tiền hỗ trợ đánh giá. VFI có thể phản ánh dòng tiền của người tham gia thị trường, cung cấp cơ sở bổ sung cho quyết định chiến lược.

Phân tích rủi ro

Chiến lược giao dịch theo mùa vụ kết hợp S&P500 cũng tồn tại một số rủi ro tiềm ẩn:

- Rủi ro quy luật lịch sử mất hiệu lực. Thị trường cổ phiếu có tính bất định cao, quy luật lịch sử không nhất thiết luôn đúng.

- Rủi ro chỉ báo kỹ thuật phát tín hiệu sai. Các chỉ báo VIX, ATR và VFI cũng có thể đánh giá sai.

- Rủi ro tối ưu tham số chưa hoàn thiện. Tham số chiến lược có thể được kiểm tra và tối ưu thêm, tham số hiện tại có thể chưa phải tối ưu.

- Rủi ro bổ sung từ bán khống. Giao dịch bán khống tùy chọn mang lại rủi ro thua lỗ vô hạn.

Có thể tăng cường chiến lược thông qua quản lý rủi ro, kết hợp chỉ báo, điều chỉnh tham số, áp dụng học máy, v.v., để giải quyết các rủi ro trên.

Hướng tối ưu

Chiến lược giao dịch theo mùa vụ kết hợp S&P500 có thể tối ưu hóa thêm từ các khía cạnh sau:

- Kiểm tra với dữ liệu lịch sử dài hơn. Có thể sử dụng nhiều dữ liệu lịch sử hơn để kiểm tra lại và tối ưu tham số chiến lược.

- Thêm cơ chế cắt lỗ. Có thể thiết lập cắt lỗ thả nổi hoặc cắt lỗ theo thời gian, kiểm soát hiệu quả thua lỗ từng lệnh.

- Tối ưu tham số chỉ báo kỹ thuật. Có thể điều chỉnh tham số VIX, ATR và VFI, tìm tổ hợp tham số tối ưu.

- Áp dụng mô hình học máy. Sử dụng mạng nơ-ron hoặc cây quyết định để tối ưu tham số thích ứng.

- Kết hợp chiến lược. Có thể kiểm tra kết hợp với các chiến lược khác, tận dụng tính không tương quan để giảm rủi ro hệ thống thị trường.

Tổng kết

Chiến lược giao dịch theo mùa vụ kết hợp S&P500 vận dụng tổng hợp quy luật theo mùa đã được kiểm chứng, điều kiện chỉ báo kỹ thuật và chỉ báo dòng tiền. Chiến lược này tránh được những tháng thị trường cổ phiếu hoạt động kém nhất, phân bổ vốn vào các tháng giao dịch tốt trong năm, đồng thời tích hợp cơ chế lọc biến động thị trường hiệu quả, có thể tạo ra lợi nhuận vượt trội ổn định. Đồng thời, chiến lược dễ dàng kiểm tra, tối ưu và điều chỉnh, cung cấp một khuôn khổ tham khảo và phát triển thứ hai cho các nhà giao dịch định lượng. Bằng cách đưa vào thêm dữ liệu, biện pháp cắt lỗ, điều chỉnh tham số và kết hợp, có thể nâng cao hơn nữa hiệu quả của chiến lược.

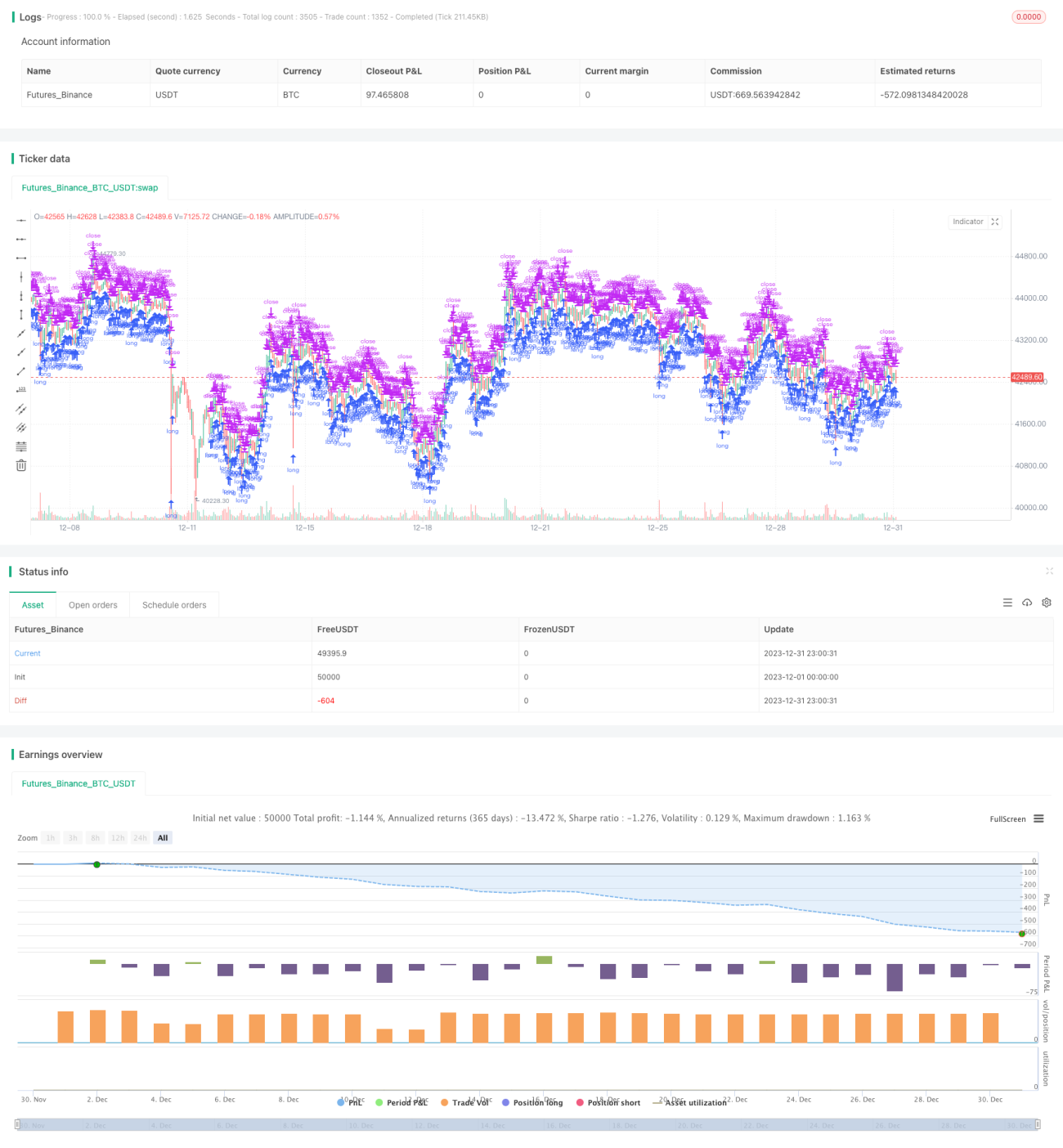

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// TASC Issue: April 2022 - Vol. 40, Issue 4

// Article: Sell In May? Stock Market Seasonality

// Article By: Markos Katsanos

// Language: TradingView's Pine Script v5- 1