Chiến lược xu hướng BB KC tiệm tiến

Tổng quan

Chiến lược này sử dụng kết hợp tín hiệu từ Dải Bollinger và Đường Keltner để nhận diện xu hướng thị trường. Dải Bollinger là công cụ phân tích kỹ thuật xác định kênh giá dựa trên phạm vi biến động giá; Đường Keltner là chỉ báo kỹ thuật kết hợp biến động giá và xu hướng để xác định vùng hỗ trợ hoặc kháng cự. Chiến lược tận dụng ưu điểm của cả hai chỉ báo, thông qua việc xác định xem Dải Bollinger và Đường Keltner có xảy ra giao cắt vàng (Golden Cross) hay không để tìm cơ hội mua/bán, đồng thời kết hợp khối lượng giao dịch để xác nhận tín hiệu. Điều này giúp nhận diện hiệu quả điểm bắt đầu của xu hướng và giảm thiểu tín hiệu nhiễu.

Nguyên lý chiến lược

- Tính đường trung bình, dải trên và dải dưới của Bollinger Bands chu kỳ 20, độ rộng dải được xác định bằng 2 lần độ lệch chuẩn.

- Tính đường trung bình, dải trên và dải dưới của Keltner Channels chu kỳ 20, độ rộng dải được xác định bằng 2.2 lần khoảng dao động thực (True Range).

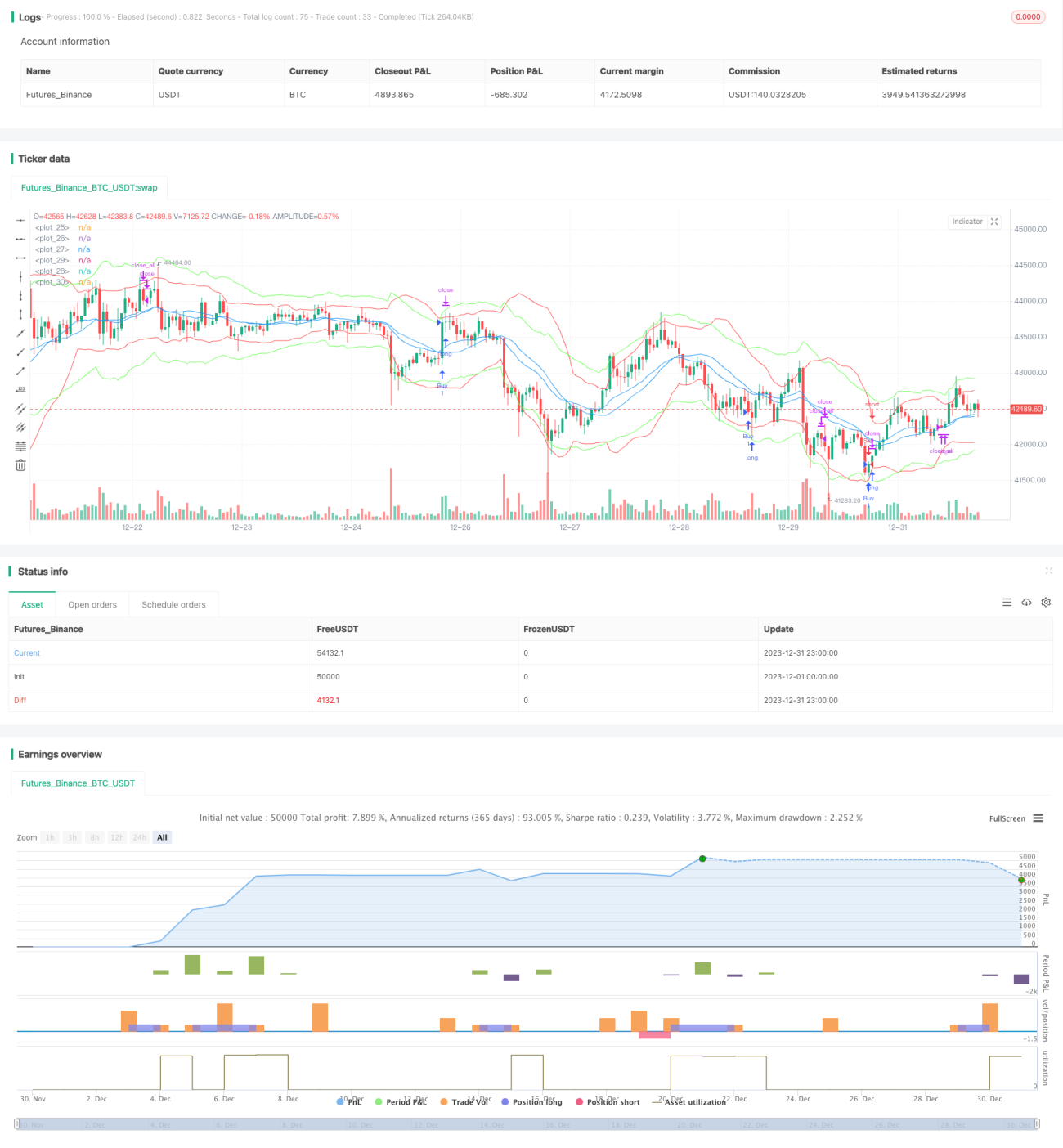

- Khi dải trên của Keltner cắt lên trên dải trên của Bollinger, và khối lượng giao dịch lớn hơn khối lượng trung bình 10 kỳ, thì mua (Long).

- Khi dải dưới của Keltner cắt xuống dưới dải dưới của Bollinger, và khối lượng giao dịch lớn hơn khối lượng trung bình 10 kỳ, thì bán (Short).

- Sau khi mở lệnh, nếu sau 20 nến không thoát, thì cưỡng chế chốt lời/cắt lỗ và thoát.

- Sau khi mua, đặt stop loss 1.5%; sau khi bán, đặt stop loss -1.5%; sau khi mua, đặt trailing stop 2%; sau khi bán, đặt trailing stop -2%.

Chiến lược này chủ yếu dựa vào Bollinger Bands để đánh giá phạm vi và cường độ biến động, sử dụng Keltner Channels để xác nhận. Sự kết hợp giữa hai chỉ báo có tham số khác nhau nhưng bản chất tương tự giúp tăng độ chính xác của tín hiệu. Việc bổ sung khối lượng giao dịch cũng giảm hiệu quả các tín hiệu nhiễu.

Phân tích ưu điểm

- Kết hợp ưu điểm của cả Bollinger Bands và Keltner Channels, nâng cao độ chính xác của tín hiệu giao dịch.

- Kết hợp chỉ báo khối lượng, giảm hiệu quả các tín hiệu nhiễu do giá chạm dải liên tục.

- Thiết lập cơ chế stop loss và trailing stop, kiểm soát rủi ro hiệu quả.

- Cơ chế cưỡng chế chốt lời/cắt lỗ sau tín hiệu nhiễu giúp nhanh chóng dừng lỗ/chốt lời.

Phân tích rủi ro

- Cả Bollinger Bands và Keltner Channels đều dựa trên đường trung bình động kết hợp với biến động, dễ phát sinh tín hiệu sai trong thị trường đi ngang.

- Không có cơ chế lãi kép, bị kẹt nhiều lần có thể dẫn đến thua lỗ lớn.

- Tín hiệu đảo chiều khá phổ biến, khi điều chỉnh tham số dễ bỏ lỡ cơ hội xu hướng.

Có thể nới rộng mức stop loss hoặc thêm các chỉ báo phụ trợ như MACD để lọc tín hiệu, nhằm giảm rủi ro từ tín hiệu sai.

Hướng tối ưu

- Có thể thử nghiệm ảnh hưởng của các tham số khác nhau lên lợi nhuận chiến lược, như điều chỉnh độ dài đường trung bình, bội số độ lệch chuẩn, v.v.

- Có thể thêm các chỉ báo khác để xác định tín hiệu, như hỗ trợ từ chỉ báo KDJ hoặc MACD.

- Có thể sử dụng phương pháp học máy để tự động tối ưu hóa tham số.

Tổng kết

Chiến lược này kết hợp sử dụng Bollinger Bands và Keltner Channels để nhận diện xu hướng thị trường, đồng thời bổ sung chỉ báo khối lượng để xác nhận tín hiệu. Bằng cách tối ưu tham số, thêm các chỉ báo kỹ thuật khác, có thể tăng cường chiến lược này để thích ứng với nhiều điều kiện thị trường hơn. Nhìn chung, chiến lược có tính khả thi cao, thuộc dạng dễ nắm bắt và điều chỉnh trong giao dịch định lượng.

- 1